What Is Driving the Tattoo Ink Market Toward USD 972 M by 2032 at 7.5% CAGR?

Other |

2026-06-20 08:38:40

PW Consulting’s latest HER2-Positive Breast Cancer Market study (base year 2025, historical 2020–2025, forecast 2026–2032) delivers an actionable, decision-grade view for life sciences and healthcare stakeholders preparing strategy for 2026 and beyond. The market has evolved from a large, innovation-driven specialty segment into a dual-speed landscape where high-value biologics and antibody-drug conjugates (ADCs) coexist with rapidly expanding biosimilar competition. Our analysis shows the global market reached approximately USD 20.2 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 9.05% through the 2026–2032 forecast window — driven by new indications, ADC adoption, and expanding access in emerging markets.

HER2-Positive Breast Cancer Market

Timing decisions on launches, label expansions, or lifecycle management must now account for a market growing at ~9% annually, where novel entrants can scale rapidly but face entrenched incumbents and biosimilar pressure.

HER2-Positive Breast Cancer Market

Commercial, clinical development, and market access leaders need integrated scenarios showing how regulatory milestones (e.g., expanded ADC approvals) and payer dynamics (including biosimilar reimbursement) will influence revenue realism and channel strategy over the next 6–8 years.

HER2-Positive Breast Cancer Market

Our study synthesizes market growth mechanics with granular risk matrices — essential for M&A screening, partnership prioritization, and real-world evidence (RWE) investments in 2026.

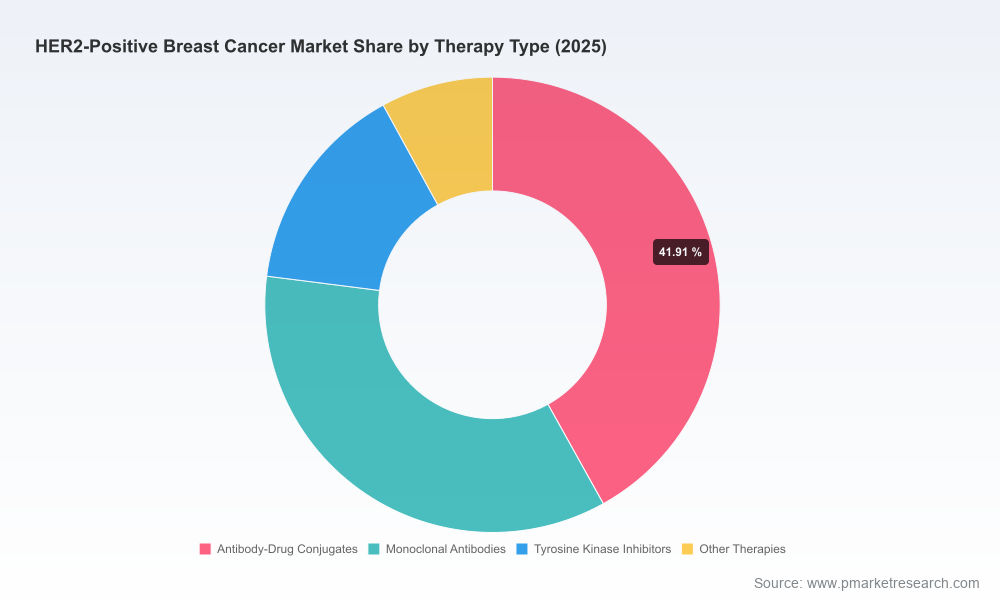

In raw terms, the HER2-positive breast cancer market has expanded materially over the last half-decade and enters the 2026 planning window from a position of strength. The USD 20.2 billion base in 2025 is a function of multiple forces: expanded indications for ADCs in earlier-stage disease, incremental combination regimens in metastatic settings, growing adoption of targeted TKIs in niche populations, and the scaled penetration of trastuzumab biosimilars following originator patent expiries. Our forecast anticipates that cumulative momentum will push the market toward the mid-to-late 2030s with a near-term CAGR of 9.05% (2026–2032), although the distribution of that growth is heterogeneous across therapy classes and channels — a level of granularity we reserve for the full report to preserve competitive sensitivity.

Regulatory expansion of ADC indications: Recent approvals have shifted ADCs from late-line niche assets to frontline and adjuvant settings in selected patient cohorts. That therapeutic reclassification materially increases addressable populations — and thus demand — for ADCs, but also intensifies scrutiny on safety, long-term outcomes, and comparative-effectiveness evidence required by payers.

Biosimilars as a structural cost lever: Trastuzumab patent expirations enabled multiple biosimilars to capture significant share by 2023. This structural shift compresses originator pricing power, accelerates substitution in institutional channels, and necessitates differentiated value propositions from innovators (e.g., convenience formulations, companion diagnostics, or superior label breadth).

Payer behavior and reimbursement mechanics: U.S. ASP-based reimbursement has materially lowered per-unit costs for biosimilars versus originators, changing hospital procurement dynamics. Simultaneously, list prices for complex biologics and ADCs remain elevated due to manufacturing complexity, which raises the commercial bar for demonstrating cost-effectiveness in national health systems.

Supply chain and access volatility: Periodic supply disruptions — particularly around trastuzumab during biosimilar scale-up and surges in demand — underscore the need for resilient manufacturing strategies, regional inventory plays, and diversified supplier networks in 2026 planning.

Regulatory nuance on interchangeability: In some jurisdictions, biosimilar interchangeability is not automatically assumed, creating prescriber-level frictions and documentation burdens that affect uptake curves and brand retention strategies.

The HER2-positive segment is consolidated among a group of multinational innovators and biosimilar specialists. Incumbent platform leaders retain strong clinical franchises, while biosimilar and ADC innovators reshape treatment algorithms.

Roche / Genentech — franchise stewardship: The Roche group remains a global anchor with a diverse HER2 franchise spanning originator monoclonals and optimized formulations. Their portfolio strategy centers on preserving clinical leadership through lifecycle extensions and formulation innovations while defending key institutional relationships.

AstraZeneca / Daiichi Sankyo — ADC standard-bearers: The AstraZeneca–Daiichi Sankyo collaboration has rapidly repositioned trastuzumab-based ADCs into earlier indications; regulatory expansions have significant implications for frontline therapy sequencing and adjuvant treatment economics.

Pfizer (including recent acquisitions) — targeted small-molecule plays: Strategic acquisitions and combination trial programs emphasize targeted kinase inhibitors for niche metastatic indications, enabling synergistic combos with existing biologics.

Biosimilar challengers — Amgen, Biocon Biologics, Viatris, Celltrion, Samsung Bioepis: These players operate on scale, pricing flexibility, and channel penetration. Their biosimilars have materially altered procurement negotiations and forced originators to pivot toward differentiated offerings.

Market concentration is high: the top three and five players command a sizable majority of market value, signifying that competitive dynamics will be dominated by strategic moves from incumbents and well-capitalized biosimilar entrants. The full competitive playbook, including SWOTs, channel strategies, and candidate-level forecasts, is covered in the complete report.

Our report is explicitly designed to be operational for 2026 decision cycles. Key deliverables include:

Robust market sizing and validated forecasts (2026–2032) with scenario analysis under alternative regulatory and pricing pathways.

Clinical-pathway overlays showing how recent regulatory events and late-stage data change treatment algorithms and addressable populations.

Segment-level access playbooks: payer engagement templates, HTA dossiers, and value demonstration evidence tailored to Europe, North America, and emerging markets.

Commercial launch and lifecycle strategies: pricing levers, channel segmentation, tender vs. private-market approaches, and distribution risk mitigation tactics.

Supplier and manufacturing risk assessments with mitigation checklists and inventory modeling to prevent revenue leakage from shortages or capacity constraints.

Deal-screening frameworks for M&A, licensing, or co-development with quantified impact on revenue, margin, and time-to-market under multiple scenarios.

Differentiation beyond molecule: For originators, expect the greatest commercial returns from investments in convenience (e.g., subcutaneous formulations), diagnostic linkage, and patient-support services that blunt biosimilar erosion.

Evidence investments: ADC sponsors must prioritize head-to-head and long-term safety trials to secure durable reimbursement, especially where list prices are elevated due to manufacturing complexity.

Biosimilar commercialization: Scale, supply reliability, and channel economics are decisive. Biosimilar entrants should prioritize institutional contracting and create flexible manufacturing footprints to capture tender opportunities.

Regional market access sequencing: Given heterogenous regulatory and reimbursement landscapes, a phased market entry — prioritizing high-value markets with clear HTA pathways — optimizes return on investment in 2026.

The study synthesizes primary interviews with payers, KOLs, and procurement leads; proprietary claims and hospital utilization datasets; and regulatory and clinical-trial pipelines. Forecasts employ scenario-based Monte Carlo modeling to stress-test uptake assumptions under diverse pricing, reimbursement, and supply conditions. While we disclose headline market sizing and trajectory, granular splits by region, therapy subsegment, and channel are intentionally reserved for subscribers to protect competitive sensitivity and to provide the actionable granularity decision-makers require.

Regulatory expansions for ADCs into earlier-stage disease have repositioned these assets from salvage therapy into potentially curative pathways for select patients — a change that demands reorientation of clinical development and commercial evidence plans.

Positive combination trial results for targeted small-molecule agents suggest growing utility for multi-modality regimens; commercial teams must plan for combination pricing dynamics and co-pay implications.

Biosimilar launches and documented pricing differentials in major markets have compressed originator margins and shifted hospital procurement behaviors; secure supply and differentiated services now drive retention.

Documented supply shortages during periods of high biosimilar demand amplify the need for contingency manufacturing and cross-border inventory strategies.

For 2026, stakeholders need more than broad-market optimism: they require prioritized, executable tactics that convert forecast growth into sustainable share and margin. PW Consulting partners with clients to translate this report into bespoke action plans — from launch readiness and HTA dossiers to M&A playbooks and supply-chain continuity planning.

Please note: this press brief intentionally presents a high-level narrative and headline metrics to communicate the strategic shape of the market. Detailed segmentation tables, therapy-by-therapy forecasts, regional allocations, and model workbooks are available through our full report and interactive portal. To access the complete dataset, granular scenario outputs, and bespoke advisory engagements, visit our report landing page or contact PW Consulting’s industry desk to arrange a briefing.

For detailed analysis of this topic, please visit the official page:HER2-Positive Breast Cancer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com