Voice Assistant Application Market Growth to Soar at 24.1% CAGR by 2031 – Trends & Insights

Other |

2026-02-19 11:15:27

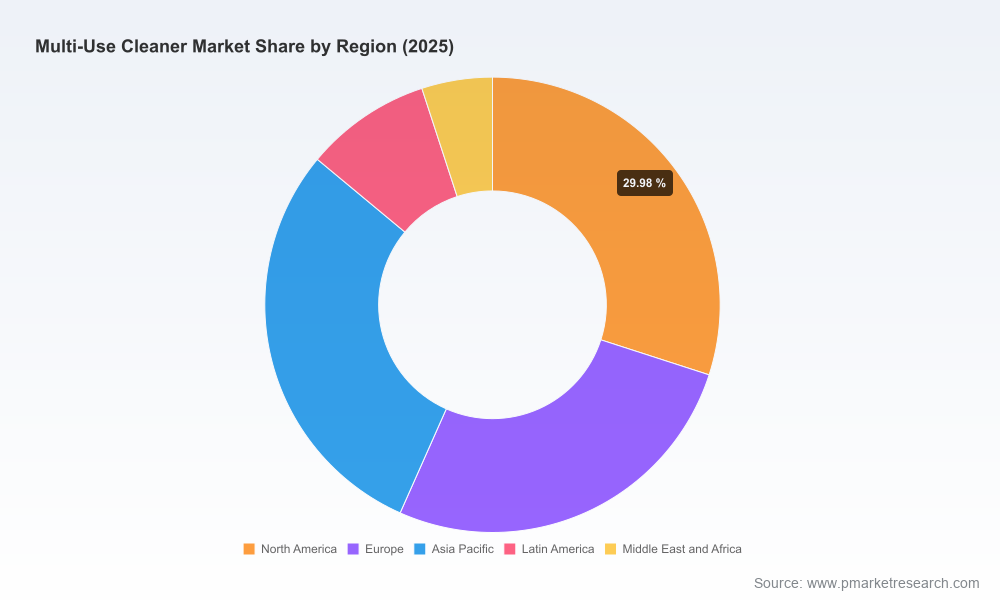

As organizations set strategy for 2026, the Multi Use Cleaner market presents a mix of steady expansion, margin pressure from raw material volatility, and attractive consolidation opportunities for market leaders and challengers alike. PW Consulting’s latest market research, grounded in a 2025 base-year assessment and a 2026–2032 forecast, models a market that grows at a mid-single-digit compound annual growth rate (CAGR of 4.61%), expanding materially from its 2025 valuation and approaching a significantly larger market size by 2032. This briefing outlines the core strategic implications for corporate decision-makers while reserving the detailed segment- and country-level tables for the full report.

Multi Use Cleaner Market

Reliable macro sizing to guide capital allocation — The report establishes an updated market baseline (2025) and presents a transparent forecast through 2032, enabling CFOs and strategy leads to stress-test growth assumptions in product launches, capex, and M&A models against an industry growth trajectory of roughly 4.6% annually.

Multi Use Cleaner Market

Raw material and margin sensitivity — Our scenario modeling incorporates recent feedstock dynamics (notably Linear Alkyl Benzene price movements observed across major markets), demonstrating how input-cost fluctuations materially affect gross margins for different product formats and pack sizes.

Multi Use Cleaner Market

Regulatory and sustainability inflection points — Certification programs (for example, the U.S. EPA Safer Choice) and evolving green-claims scrutiny are increasingly determinative of shelf placement and institutional procurement. The report translates regulations into commercial levers for product positioning and compliance-ready roadmaps.

Competitive structure and consolidation pathways — The market’s concentration profile shows a mid-level consolidation (the top three and top five firms account for a meaningful share of demand), which shapes playbooks for incumbents and entrants around pricing discipline, distribution control, and M&A prioritization.

Validated market sizing and transparent forecasting methodology (base year 2025; forecast 2026–2032) with sensitivity testing across raw material and demand scenarios.

Scenario playbooks mapping pricing, formulation, and channel moves to P&L outcomes—ideal for commercial planning and investor diligence.

Competitive intelligence dossiers on leading players, including capability maps (brand, formulations, channel strength, professional vs. consumer focus) and likely strategic moves.

Supply-chain risk matrix and procurement levers, with practical guidance on hedging, supplier diversification, and concentrate versus ready-to-use SKU economics.

Regulatory impact assessment with a compliance checklist and marketing dos/don’ts for environmental claims.

Go-to-market templates and retailer/professional channel negotiation tactics for accelerating share gains.

M&A screening framework and candidate shortlist methodology to identify bolt-on targets that deliver scale, route-to-market, or formulation IP.

Prioritize procurement flexibility: Volatility in surfactant feedstocks is a near-term margin risk. Companies should operationalize dual-sourcing, index-linked contracts, and a small but strategic inventory buffer to flatten cost cycles and avoid reactive price increases that erode share.

Product architecture rebalancing: The economics favor concentrated formats and refill systems where possible—these reduce transport and packaging cost per-use and align with sustainability narratives that matter to both retailers and institutional buyers.

Invest in certification and transparent claims: Certifications validated by recognized programs materially improve win-rates in institutional tenders and assortment decisions in premium retail channels. Prioritize certifications that demonstrably reduce environmental impact without compromising efficacy.

Adopt a segmented channel strategy: Differentiate value propositions for household retail versus professional/institutional channels. Professional customers increasingly prize service, dosing solutions, and bulk packaging; consumer channels remain sensitive to brand, scent, and convenience formats.

R&D to focus on formulation substitution and efficacy: Develop pipelines for lower-VOC, biodegradable surfactants, and multifunctional concentrates that preserve or enhance cleaning efficacy while enabling green claims—this both mitigates regulatory risk and supports premiumization.

Monitor and act on consolidation windows: The market’s concentration suggests attractive bolt-on opportunities for regional players to gain scale; conversely, larger players can target capabilities (supply chain, formulation IP, commercial networks) to accelerate profitable growth.

Embed scenario-driven pricing: Use rolling scenario models tying input-cost simulations to price cadence and promotional strategies to avoid margin erosion while protecting volume.

The Procter & Gamble Company (Cincinnati, Ohio) — Strengths lie in brand equity, consumer insights, and scale marketing. P&G’s optimal play in 2026 is to protect premium household formats while testing concentrated/refill innovations within targeted geographies to validate unit-economics.

The Clorox Company (Oakland, California) — Deep in disinfectant claims and institutional channels; Clorox should leverage its disinfectant credibility to capture higher-margin institutional contracts and expand bundled service offerings.

Reckitt Benckiser (Slough, UK) — With strong multi-surface disinfectant brands, Reckitt is positioned to convert heightened hygiene awareness into sustained premium demand—invest in demonstrable efficacy studies and certification to defend pricing.

Henkel, Unilever, S.C. Johnson — These household-focused players must balance volume-driven assortment at mass retail with a curated set of sustainable SKUs that command incremental margin.

Ecolab, Diversey, Zep, Spartan, Betco — The professional and industrial supply specialists should double down on service-led differentiation: dosing systems, contract cleaning partnerships, and digital monitoring to lock-in institutional clients.

3M, Church & Dwight — Niche formulation or chemistry advantages provide opportunities to license IP or pursue selective co-branding to access adjacent channels without swelling fixed costs.

Feedstock price shocks: Sudden spikes in surfactant raw materials can compress gross margins and force suboptimal pricing decisions. Monitor quarterly benchmark pricing and have trigger-based commercial responses.

Regulatory tightening and green-claims scrutiny: Non-compliant or ambiguous environmental claims can lead to penalties and reputation damage. Keep certification and testing programs current and visible.

Accelerated private-label competition: Retailers are increasingly deploying own-label multipurpose cleaners at aggressive price points. Defend through value-added formats, branded sustainability, and retailer collaboration models.

Supply-chain concentration: Overdependence on single-region suppliers for key surfactants invites disruption risk—diversify and consider nearshoring where feasible.

Input-cost exposure (% of COGS tied to surfactant indexes) and contract hedging coverage.

Pack-level margin per SKU and per-use cost analysis (concentrate vs. ready-to-use).

Certification conversion rate (share of SKUs with third-party validation) and tender win-rate in institutional channels.

Net new-store distribution vs. lost-shelf occurrences (retail assortment changes).

M&A pipeline scorecard (strategic fit, expected synergies, execution risk).

For 2026 strategy cycles, the priority for executives is to convert foresight into defensible action: secure procurement flexibility, accelerate formulation and packaging innovations that meet both sustainability and efficacy tests, and recalibrate commercial models by channel. The full PW Consulting Multi Use Cleaner Market report contains the exhaustive segmentations, country-level dashboards, SKU-level economics, company benchmarking matrices and deal-readiness playbooks that underpin the strategic highlights summarized here.

To preserve the integrity of actionable insights, we have deliberately withheld granular segment tables and detailed regional/applications values from this briefing. Access to the complete dataset and executable playbooks is available through PW Consulting’s report page and enables teams to run bespoke scenario simulations tuned to their portfolio and market exposure.

PW Consulting remains available to support 2026 strategic planning workshops, procurement stress-tests, and M&A diligence grounded in this research. Armed with precise inputs and the recommended monitoring framework, decision-makers can convert the market’s steady growth and structural challenges into a durable competitive advantage.

For detailed analysis of this topic, please visit the official page:Multi Use Cleaner Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com