How Can Google Local Services Ad Management Service Boost Local Leads?

Technology |

2026-04-22 07:52:12

PW Consulting today publishes a forward-looking briefing derived from our comprehensive Fused Silica Tubing Market study, with direct relevance to procurement leaders, manufacturing strategists, investors, and R&D heads preparing decisions through 2026 and beyond. Our model shows the market expanding from USD 635.4 Million in 2020 to USD 845.0 Million in 2025, and continuing to grow through the 2026–2032 forecast window — reaching an estimated USD 1,280.66 Million by 2032 at a compound annual growth rate (CAGR) of 6.12% for the forecast period. This release highlights the practical, decision-ready insights contained in the full report while intentionally withholding segment-level tables and exact regional/application breakdowns to preserve the report’s proprietary value.

Fused Silica Tubing Market

Precision capital allocation: The market trajectory and scenario modelling in our study translate into concrete capex timing recommendations for capacity expansion, retrofit, and automation investments that protect margins under raw-material price volatility.

Fused Silica Tubing Market

Supply-chain resilience: We map the HPQ (high-purity quartz) supply chain and associated geopolitical exposures so procurement teams can prioritize dual-sourcing and strategic stock initiatives before 2026 contract renewals.

Fused Silica Tubing Market

Product and process roadmapping: Technology cadence for large-diameter, low-fluorescence, and UV-stable tubing is correlated with end-market adoption curves, enabling product managers to sequence development and commercialization to capture premium niches.

M&A and partnership screening: Our competitive assessment and consolidation scenarios provide a prioritized list of acquisition and JV archetypes — including capability acquisition versus market-share plays — to accelerate inorganic growth strategies.

Executive dashboard: A concise, action-oriented executive summary with topline market sizing and three investment-ready scenarios (Base, Upside, Stress) mapped to trigger points for 2026 decisions.

Methodology and transparent modelling: Time-series demand model (2020–2025 historical; 2026–2032 forecast) with sensitivity levers for HPQ pricing, semiconductor wafer starts, and fiber-optics capital intensity.

Supplier scorecards: Comparative performance matrices that assess capacity, product breadth (e.g., high-purity vs. synthetic routes), technological differentiators, service levels, and concentration risk.

Raw-material risk map: Geographic concentration analysis of HPQ feedstock, price band scenarios, and regulatory disruption stress tests, plus mitigation playbooks — hedging, toll-fusion contracts, and backward integration options.

Commercial playbooks: Pricing frameworks, contract templates, and inventory KPIs tailored for OEMs, distributors, and test-lab buyers to secure continuity while optimizing total cost of ownership.

Capex and manufacturing guide: Build vs. buy decision matrix for fusion technology (plasma fusion, electric fusion, synthetic routes), yield benchmarks, and automation ROI models calibrated for 2026–2028 horizons.

Regulatory and ESG monitor: Assessment of environmental permitting risk, mining restrictions affecting HPQ supply, and near-term compliance investments required by producers in sensitive jurisdictions.

Raw material intensity and pricing: High-purity quartz (HPQ) is the single largest cost driver for fused silica tubing. Industry pricing bands for HPQ vary markedly by grade, creating margin dispersion between producers that own feedstock and those reliant on merchant markets. Our scenarios model price bands and pass-through effects so buyers and manufacturers can negotiate contracts with embedded conditional price mechanisms.

Feedstock geography and concentration: Supply of the highest-grade feedstock remains geographically concentrated in a handful of jurisdictions. That concentration translates into latent supply fragility in the event of localized regulatory actions, permitting delays, or logistics disruptions — all variables embedded in the PW stress-test scenarios.

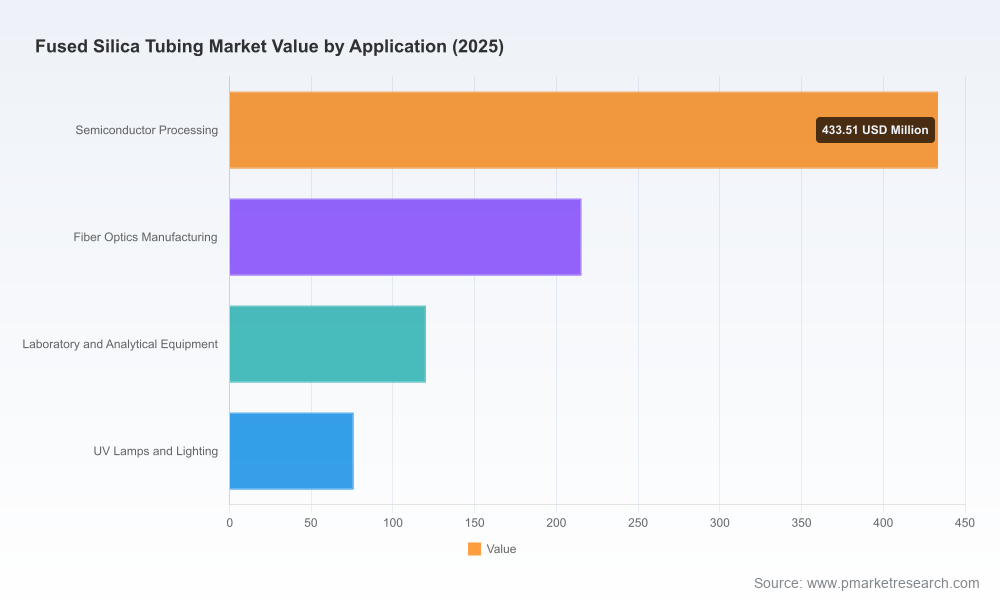

End-market mix shift: Demand drivers include semiconductor processing equipment, fiber optics, laboratory instrumentation, and specialty UV/laser applications. While PV-driven demand eased in the 2024–2025 window, semiconductor capital intensity and advanced photonics continue to exert upward pressure on premium fused silica segments.

Regulatory overlay: Tighter environmental and mining regulations in key HPQ regions — coupled with mid-decade tariff negotiation noise between major economies — increases the likelihood of upstream cost shocks and regional price differentials. Companies that pre-emptively adapt procurement and production footprints will gain a durable cost advantage.

Heraeus Covantics (Hanau, Germany): A market leader in high-purity fused silica and fused quartz tubing, positioned strongly across semiconductor and optics segments. Expect continued emphasis on differentiated product lines and global service networks to protect premium positioning.

Momentive Technologies (Hebron, Ohio): With a center of excellence for quartz fusion and recent capacity investments targeting large-diameter tubing, Momentive is deliberately addressing semiconductor wafer-processing demand. Their 2023 expansion underscores a play for scale in high-tolerance applications.

QSIL GmbH (Germany/Netherlands): A niche technology player leveraging a plasma fusion process to produce very large hollow cylinders and custom OD tubing. QSIL exemplifies the technical-differentiation route — attractive to strategic partners requiring non-standard geometries.

Tosoh and Shin-Etsu (Japan): These incumbents remain critical suppliers to semiconductor-grade markets, combining upstream material control with close customer engineering support in Asia. Their strength lies in integration across material and quartzware offerings.

Saint-Gobain Quartz (France) and WEINERT Industries (Germany): Both emphasize high-temperature and low-fluorescence performance niches, respectively. Their plays center on specialty performance attributes that command premium pricing and higher switching costs.

Polymicro Technologies / Molex and Technical Glass Products (TGP): These firms address precision and lab/analytical markets with coated capillaries and custom catalog offerings. TGP’s December 2025 catalog refresh is illustrative of demand for near-shore, configurable supply options among laboratory and industrial buyers.

China-based integrated producers: A cohort of Chinese manufacturers is scaling capabilities to serve global semiconductor and solar ecosystems. Their trajectory will be shaped by raw-material access, trade policy developments, and technology licensing dynamics.

Capacity moves: Momentive’s mid-decade capacity expansion to increase production of large-diameter tubes signals an expectation of sustained premium demand from wafer-processing and advanced packaging segments. Such moves typically precede measurable pricing stabilization in premium-size bands.

Product breadth: Catalog and product-range updates from regional fabricators reflect rising demand for configurable lead times and tailored sizes — a tactical response to buyers seeking inventory flexibility and reduced supply-chain lead times.

For manufacturers: Prioritize technology investments that raise effective barriers — proprietary fusion processes, coatings that reduce fluorescence, and automation that shortens lead times. Early supplier contracts for HPQ and options on additional feedstock volumes are essential.

For OEMs and fabs: Move from spot buying to multi-year conditional supply contracts with volume, quality, and dual-sourcing clauses. Invest in qualification pools and co-development arrangements with suppliers to secure priority allocation during cyclical tightness.

For investors and M&A teams: Target bolt-on acquisitions that add specialty capability (large OD, low-fluorescence tubing, or capillary coating) rather than commodity capacity. Our scoring system highlights priority targets where technology and customer relationships compound value.

For procurement: Implement HPQ price-curve monitoring and structured options to hedge exposure. Our report provides template contract language and a decision tree for when to lock fixed pricing versus index-linked mechanisms.

The fused silica tubing market is neither purely cyclical nor purely commoditized; it is a technology- and feedstock-intensive ecosystem where product differentiation, feedstock control, and proximity to end markets define winners. The projected mid-single-digit CAGR and the projected increase in absolute market size through 2032 create opportunities for disciplined investors and operationally nimble manufacturers — but they also raise the stakes for anyone with 2026 capital or sourcing decisions on their docket.

PW Consulting’s full Fused Silica Tubing Market report contains the proprietary regional and application splits, detailed supplier scorecards, raw-material price scenarios, and downloadable financial models that underlie the strategic recommendations summarized here. For access to the full data package, bespoke briefings, or a 2026 readiness workshop that translates these insights into an executable roadmap, please visit the PW Consulting report page or contact our market analytics team.

For detailed analysis of this topic, please visit the official page:Fused Silica Tubing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com