Drone Data Link System Market Share: Competitive Dynamics and Global Trends

Other |

2026-04-08 12:56:45

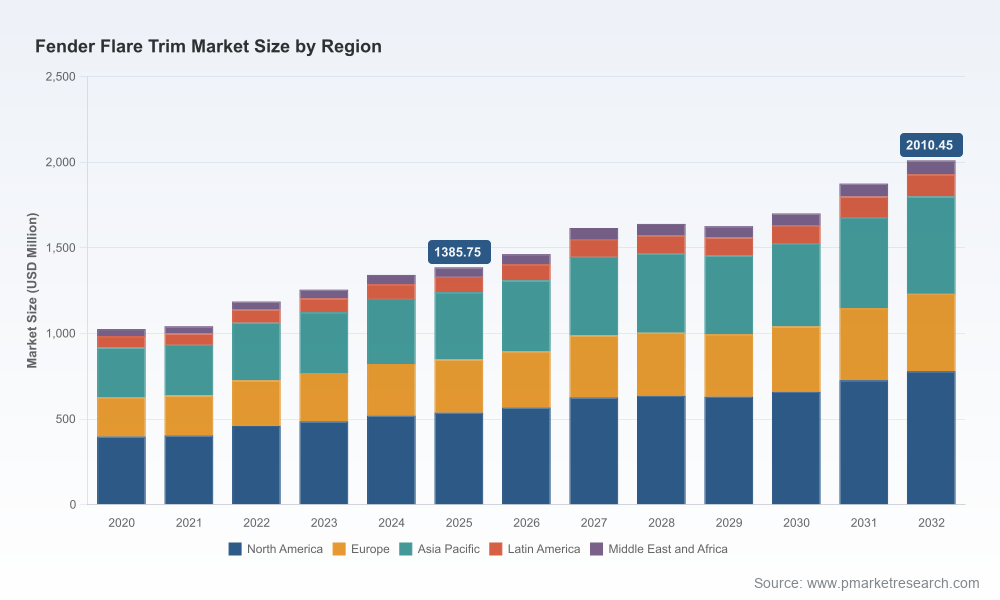

PW Consulting’s latest market brief on the Fender Flare Trim market—anchored on a 2025 base year and forecasting through 2032—translates rigorous quantitative modelling into boardroom-ready strategic guidance. The study quantifies a multi-year recovery and expansion path for the market (2020–2025 historical series, 2026–2032 forecast), and identifies the commercial vectors that will matter most as OEMs, tier suppliers, aftermarket specialists and private equity prepare 2026 playbooks. At a macro level, the segment is on a steady upward trajectory with a mid-single-digit compounded annual growth rate (CAGR) over the forecast window—evidence of durable demand underpinned by vehicle refresh cycles, accessory-driven personalization trends, and the ongoing migration of light vehicles toward modular accessory ecosystems.

Fender Flare Trim Market

Timing: 2026 is the inflection year for many firms that have been repositioning after the supply shocks of early-decade disruptions. Our analysis projects visible revenue expansion across the forecast horizon, making this an opportune moment to convert operational resilience into market share gains.

Fender Flare Trim Market

Portfolio optimization: Margins and win-rates for fender flare trims are increasingly determined by material choices, attachment systems (peel-and-stick, foam tapes, mechanical clips), and the ability to serve both OEM accessory programs and the vibrant aftermarket customization segment. Product mix decisions made in 2026 will influence manufacturing footprints and channel strategies for the next five to seven years.

Fender Flare Trim Market

Capital allocation: With market concentration moderate (top-3 and top-5 shares indicating neither extreme consolidation nor fragmentation), targeted M&A and strategic partnerships can tilt competitive dynamics—especially where firms can acquire scale in adhesive systems, EPDM supply integration, or channel access to OEM accessory catalogs.

Demand drivers: Personalization and utility remain the twin drivers. Consumers continue to treat pickup trucks and SUVs as platforms for aftermarket expression, while fleet and light commercial segments demand functional protection. The net effect is persistent volume demand for trims that balance appearance, sealing performance and ease of installation.

Material evolution: EPDM-based rubber trims retain a central role because of durability, ozone resistance and compatibility with automotive adhesives. Broader growth in synthetic rubber markets—projected to increase materially through the forecast period—reinforces raw material availability and cost stability. For 2026 buyers, this translates into predictable input sourcing if procurement strategies are proactive.

Attachment systems: The market is bifurcating between adhesive-led peel-and-stick solutions (favoured for fast aftermarket installs and OEM accessory kits) and mechanically-clipped edge trims used where reusability or higher environmental tolerance is required. Product teams must prioritize modular designs that can be adapted to either attachment philosophy without a complete retool.

Regulatory and OEM quality bar: Automotive-grade flammability and safety standards remain non-negotiable; components like EPDM trims typically comply with established standards (e.g., FMVSS 302 in relevant markets). Compliance and traceability will therefore be prerequisites for OEM channel entry in 2026—an important gating factor for suppliers contemplating rapid expansion.

Market sizing and trend analysis: A detailed historical series (2020–2025) and a granular forecast (2026–2032) presented in USD (Million), including sensitivity scenarios that test key assumptions such as vehicle production swings, material cost shocks and aftermarket spending elasticity.

Demand-driver deep dives: Driver maps for OEM accessory programs, aftermarket personalization, fleet specifications and off-road accessory ecosystems—each linked to actionable levers suppliers and OEMs can pull to capture higher share or margin.

Commercial playbooks: Go-to-market templates for OEM vs aftermarket focus, pricing frameworks for adhesive vs mechanical attachment systems, and product-portfolio blueprints to align R&D and production planning across 2026–2028.

Supply chain and procurement toolkit: Risk matrices and supplier scorecards that reflect raw material dynamics (including EPDM availability), recommended hedging approaches, and nearshoring vs global sourcing trade-offs.

Competitive heatmaps and capability audits: Comparative assessments of manufacturing, adhesive-system knowhow, OEM channel access and aftermarket brand strength to help prioritize inorganic options and partnership targets.

Trim-Lok, Inc. (San Clemente, CA): A diversified player with an expanding catalog and recent product introductions that strengthen its sealing and trim portfolio. Their advances in cataloging and cut-to-length product kits indicate a play for convenience-driven installers and OEM accessory programs alike. For competitors, Trim-Lok’s push signals the importance of fast-ship SKUs and installer-friendly kits; for investors, it highlights an asset-light route to aftermarket scale via distribution and product breadth.

Trimco (USA): Known for flexible plastic trims designed to conform to fender curvature and to adhere with proven acrylic foam tapes. Their product architecture exemplifies the “fit-and-forget” aftermarket preference. Strategic partners should evaluate collaboration on adhesive systems to both lower total cost of ownership for end-users and to lock-in channel relationships.

Johnson Bros. Roll Forming Co. (Berkeley, IL): Custom manufacturers like Johnson play a pivotal role when OEMs demand bespoke profiles and tight dimensional tolerances. 2026 planning should account for lead-time advantages that custom roll formers can provide to captive accessory programs—especially where integration with other body components is required.

Bushwacker (USA) & Air Design (USA): Firms that bridge OEM accessory channels and the accessory-first aftermarket. Bushwacker’s replacement-edge trim options and Air Design’s OE-style fitment approach showcase two viable routes: premium replacement and factory-matching accessories. Suppliers and OEMs should evaluate licensing and co-branding models to scale these channels.

Steel Rubber & Putco (USA): These players highlight divergence in material and positioning—EPDM-focused suppliers emphasizing durability and weather resistance versus premium stainless steel trim specialists targeting style-conscious buyers. Our competitive mapping shows room for niche premium plays alongside high-volume polymer strategies.

Prioritize modular product architectures. Design trims that can be rapidly configured for either adhesive or mechanical attachment, enabling access to both quick-fit aftermarket installs and OE accessory programs without doubling development costs.

Lock in EPDM supply agreements with tiered volume and quality commitments. Given EPDM’s centrality and industry-level demand growth, medium-term supplier agreements and joint development on compound formulations will protect margin and speed to market.

Invest in installer-centric SKUs and distribution velocity. Trim-Lok’s catalog moves demonstrate that rapid fulfillment and fitment simplicity unlock aftermarket share. Consider cut-to-length packs, multilingual design guides, and metric SKU variants for international expansion.

Make channel-specific margin plays. OEM accessory programs value traceability and consistent quality; aftermarket buyers prize price and aesthetics. Tailor cost structures and branding to these distinct economics.

Execute targeted inorganic moves to close capability gaps. With the market’s moderate concentration, bolt-on acquisitions that add adhesive-system expertise, roll-form tooling, or regional distribution can deliver outsized returns versus greenfield buildouts.

Embed regulatory and sustainability credentials into product roadmaps. FMVSS-compliant materials, recyclable polymer options and documentation-ready supply chains will be competitive differentiators in OEM selection processes during 2026 procurement cycles.

The Fender Flare Trim market offers a resilient growth trajectory and a portfolio of strategic entry points for incumbents and new entrants alike. The market’s structure and material dynamics reward those who combine product modularity, supplier integration (particularly around EPDM), and channel-specific commercialization. Importantly, the 2026 planning window is decisive: choices about where to allocate R&D, whom to partner with for adhesives and roll-form capabilities, and whether to pursue scale through M&A will materially shape who captures the next wave of accessory and OEM growth.

PW Consulting’s full Fender Flare Trim Market report contains the comprehensive datasets, scenario models and company-level assessments necessary to operationalize these recommendations. Our analysis presents the complete forecast run, sensitivity tables and a tactical playbook—designed for executives preparing 2026 budgets and three-year strategic plans. For access to the complete figures, segment breakouts and downloadable decision-support tools, please visit the report page on our website.

For detailed analysis of this topic, please visit the official page:Fender Flare Trim Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com