Millimeter Wave Radar for Unmanned Driving: Strategic Imperatives for 2026 — A PW Consulting Market Brief

Executive Summary

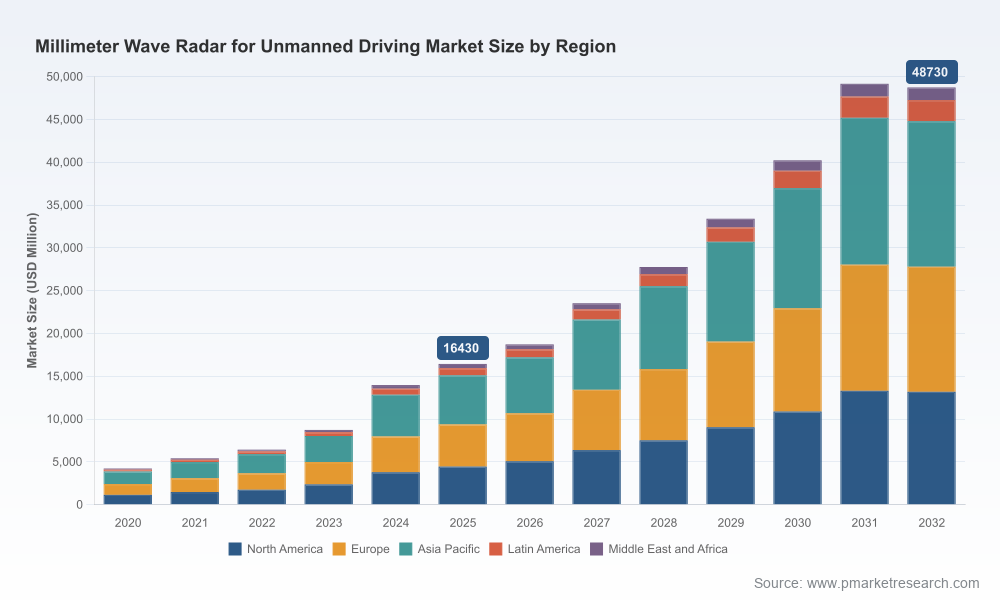

As unmanned driving systems migrate from experimental to commercial deployments, millimeter wave (mmWave) radar has emerged as a core sensor class for robust perception in complex environments. PW Consulting’s latest market model shows the global mmWave radar market for unmanned driving reached approximately USD 16.43 billion in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of 19.7% through the 2026–2032 horizon, peaking near the USD 49 billion range by 2031 before moderating into 2032. Such rapid expansion presents a strategic inflection point for OEMs, Tier‑1 suppliers, semiconductor vendors, and investors. Our new report is designed to convert that macro momentum into actionable decisions for 2026.

Millimeter Wave Radar For Unmanned Driving Market

Why This Matters for 2026 Decision-Makers

- Timing and scale: The market trajectory implies large-scale unit adoption and rising ASPs for next‑generation radars — creating windows for capture strategies that must be executed in 2026 to participate in 2027+ series ramps.

- Concentration dynamics: Market share is meaningfully concentrated — the top three and five players account for a plurality of the market — implying that strategic partnerships and scale economics will determine winners and losers.

- Technology inflection: Advances in 4D imaging, digital beamforming, and integrated mmWave SoCs are reshaping system architectures. Firms that align silicon, sensor modules, and perception software stand to materially outperform.

Report Snapshot — What the PW Consulting Deliverable Contains (Practical, Action‑oriented)

We structured the report to be a decision tool rather than an academic exercise. Key practical elements include:

Millimeter Wave Radar For Unmanned Driving Market

- Executive decision playbooks for OEMs, Tier‑1s, and semiconductor suppliers that translate market scenarios into prioritized actions for procurement, R&D, and commercial agreements.

- Supply‑chain resilience modules: stress‑test scenarios, critical component risk maps, alternative sourcing routes, and negotiating levers for 2026 contract cycles.

- Go‑to‑market templates for radar module commercialization (product roadmaps, tiering strategies, margin waterfall models, and launch readiness checklists).

- Technology roadmaps and integration guides that compare legacy narrow‑band radar approaches with emerging wideband 4D imaging architectures and SoC integration patterns.

- Regulatory and spectrum engagement playbook: a prioritized list of jurisdictions, regulatory milestones, and recommended advocacy positions to influence allocation and certification timelines.

- Investor-facing scenario analyses including base, upside, and stress cases — with sensitivities by adoption pace, semiconductor availability, and regulatory timelines to support valuation decisions.

Note: To preserve the strategic advantage for subscribers and partners, detailed tables containing breakouts by region, frequency band, and application-level market sizing are summarized in the report but are intentionally not disclosed in this press brief.

Millimeter Wave Radar For Unmanned Driving Market

Competitive Landscape — What 2026 Choices Look Like

The competitive map blends legacy automotive systems integrators, semiconductor incumbents, and specialized radar startups. Across the ecosystem, three distinct strategic archetypes are emerging: (1) integrated system leaders that combine sensor hardware, SoCs, and perception software; (2) silicon‑first vendors focused on high‑performance mmWave MMICs and SoCs; and (3) niche imaging specialists pushing 4D radar capabilities.

- Robert Bosch GmbH — Leveraging deep automotive systems experience, Bosch’s recent SoC launches accelerate the company’s push to deliver integrated radar stacks for Level 2+ and higher automated features. Expect Bosch to emphasize system validation, safety certification, and supply agreements with OEMs in 2026.

- Continental AG — With significant production scale and new-generation sensor platforms, Continental is positioned to capitalize on high-volume unmanned driving programs. Their manufacturing footprint and series orders make them a natural partner for OEMs seeking rapid industrialization.

- Denso Corporation — Known for long-range detection and multi-sensor fusion, Denso will appeal to vehicle manufacturers prioritizing proven reliability and global supply networks.

- Valeo and HELLA — Both bring module-level expertise and strong integration pathways to the perception stack; expect co-development and joint validation projects with semiconductor partners.

- Aptiv and ZF — Systems integrators that marry active safety platforms to autonomy roadmaps; in 2026 they will be focal points for partnerships between OEMs and sensor innovators.

- Arbe Robotics and Uhnder — Specialists in high-resolution 4D imaging radar, these firms are pushing perceptual gains that enable denser urban autonomy use cases. Their technology demonstrations at recent trade shows highlight readiness for targeted integrations.

- Texas Instruments and Infineon — Silicon incumbents supplying mmWave RFICs and radar MMICs. Their product roadmap and packaging capabilities are key enablers, especially amid semiconductor supply uncertainties.

Recent industry moves—such as product launches, production starts in new geographies, and strategic co‑development agreements—underline two realities for 2026: first, incumbents continue to scale manufacturing; second, innovative entrants are shortening the technology lead time. Both trends raise the bar for partner selection and speed of execution.

Market Dynamics and Headwinds

- Regulatory drivers: Mandatory advanced safety features in multiple jurisdictions are a tailwind for mmWave adoption; simultaneous delays in spectrum allocation in some regions create a patchwork deployment risk that must be actively managed.

- Semiconductor constraints: High‑frequency radar chips remain sensitive to upstream supply disruptions. Companies must institutionalize dual-sourcing, buffer strategies, and long‑lead purchasing to avoid production bottlenecks in 2026 launches.

- Workforce and operational costs: A shortage of RF engineering and precision metrology talent is increasing operational costs for automated production lines; training and process automation investments are therefore non‑negotiable.

- Consolidation pressure: Given observable market concentration, mid‑tier vendors face margin compression and strategic pressure to seek alliances, carve-outs, or M&A to secure scale.

Strategic Actions Recommended for Calendar Year 2026

Based on our modeling and client engagements, PW Consulting recommends a prioritized set of actions for firms looking to lead in mmWave radar for unmanned driving:

- Lock critical silicon capacity now: Secure supply agreements for HF radar SoCs and MMICs with clear delivery milestones and penalty‑based commitments to mitigate semiconductor volatility.

- Pursue modularity in system design: Architect sensor modules that allow field upgrades (software/firmware) and retargeting across frequency bands to maximize reuse across programs and geographies.

- Invest in 4D imaging selectively: For use cases requiring dense urban perception, prioritize pilots with 4D imaging radar partners to validate performance and integration risk before committing to volume buys.

- Form strategic manufacturing partnerships: Consider co‑investing in regional production facilities or entering capacity partnerships to reduce lead times and meet localization requirements.

- Engage in regulatory forums: Proactively shape spectrum allocation and type‑approval pathways through industry coalitions to reduce deployment uncertainty.

- Adopt an M&A playbook: Use 2026 as an opportunistic year to acquire niche innovators (sensor imaging, perception middleware) that complement core competencies and accelerate time to market.

Risk and Sensitivity Considerations

The upside case in our model assumes accelerated regulatory harmonization, rapid semiconductor recovery, and aggressive OEM adoption plans. The downside is dominated by persistent supply chain constraints, delayed spectrum approvals, or slower-than-expected validation cycles for higher autonomy levels. PW Consulting’s full report includes scenario matrices and sensitivity tables that quantify these effects on revenues, deployment timelines, and margin implications for each archetype of market participant.

Conclusion — The 2026 Opportunity Window

2026 is a pivotal year: buyers will lock design wins that influence production starting in 2027 and beyond. Firms that move early to shore up supply, align silicon and system architectures, and secure strategic partnerships will capture disproportionate value. The pace of technological maturation — particularly around 4D imaging and integrated mmWave SoCs — combined with the market’s near‑term growth trajectory, means that commercial choices made in 2026 will determine market positioning for the next half‑decade.

Next Steps — How to Access the Full Intelligence

This press brief is a preview of the full PW Consulting Millimeter Wave Radar for Unmanned Driving Market report. Subscribers receive comprehensive segmentations, market models, supplier scorecards, playbooks, and downloadable spreadsheets designed for boardroom decision-making. For a complete set of data, granular regional and application breakouts, and hands‑on advisory support for 2026 planning, please visit our report page or contact your PW Consulting representative.

For detailed analysis of this topic, please visit the official page:Millimeter Wave Radar For Unmanned Driving Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com