Anti Fog Polycarbonate Film and Sheet Market — Strategic Outlook for 2026: A PW Consulting Preview

Executive synopsis

PW Consulting’s latest market study on Anti Fog Polycarbonate Film and Sheet provides an actionable intelligence package tailored for executive teams planning capital allocation, product roadmaps, and global supply-chain decisions in 2026. The study synthesizes five years of historical performance (2020–2025) with a forward-looking forecast through 2032, quantifying market scale, growth trajectory and competitive positioning while delivering pragmatic playbooks for procurement, product development and regulatory risk mitigation.

Anti Fog Polycarbonate Film And Sheet Market

Market at a glance

The market has demonstrated resilient expansion, moving from an assessed global revenue base in 2020 to an estimated USD 194.5 Million in 2025. Driven by steady adoption across personal protective equipment (PPE), automotive interiors, greenhouse glazing and electronics, the market is projected to grow at a compound annual growth rate (CAGR) of approximately 5.45% over the 2026–2032 forecast horizon, reaching a multi-hundred million-dollar industry by 2032. This steady growth underscores the transition of anti-fog polycarbonate from niche replacement to a mainstream specification in humidity-sensitive environments.

Anti Fog Polycarbonate Film And Sheet Market

Why this report matters to 2026 decision-makers

- Timing of strategic moves: 2026 is a pivotal year for firms evaluating capacity builds, vertical integration or strategic partnerships — the market’s trajectory supports measured expansion but rewards precision in product-market fit and regulatory preparedness.

- Supply-chain signal clarity: Recent raw-material volatility and tariff noise mean procurement strategies must be stress-tested against multiple scenarios; the report models those scenarios and quantifies sensitivity to feedstock price swings.

- Regulatory and sustainability risk: Evolving restrictions on additive chemistries and single-use plastics will affect product formulations, supplier selection and end-market access; our regulatory impact maps convert legal text into business implications.

- Competitive maneuvering: Consolidation, new capacity and differentiated coating technologies are reshaping the supplier landscape—our competitive scorecards enable rapid counterparty assessment for sourcing or M&A diligence.

Core market dynamics shaping 2026 strategies

The anti-fog polycarbonate segment is being re-ordered by four interlocking dynamics: raw-material cost pressure, regulatory tightening on specific additives, product-performance innovation (durability and PFAS-free chemistries), and demand maturation across medical, safety and agricultural applications.

Anti Fog Polycarbonate Film And Sheet Market

- Raw-material volatility: Feedstock pressures—most notably bisphenol A and associated upstream phenol/acetone markets—have increased production cost variability. Procurement teams should expect episodic price spikes that can compress margins if not hedged with flexible contracts or cost pass-through mechanisms.

- Regulatory tightening: Recent moves to restrict certain UV stabilizers and persistent organic pollutants in key jurisdictions have created compliance timelines that directly affect product formulations and labeling. The report translates regulatory milestones into workable product redevelopment roadmaps.

- Technology differentiation: Suppliers advancing long-lasting hydrophilic coatings, abrasion-resistant topcoats and PFAS-free chemistries are gaining distinct commercial traction. Buyers and OEMs should prioritize validated field performance over laboratory claims when evaluating new coatings.

- Demand diversification: While medical visors and safety shields remain critical drivers, greenhouse and architectural glazing, automotive interior optics and refrigeration/display cases are enlarging the addressable market. Each end market brings unique technical and procurement constraints that require tailored commercial approaches.

Competitive landscape — what to watch

The industry is a mix of global polymer majors, specialty coaters and regional sheet manufacturers. Market concentration data indicates a moderate level of aggregation at the top—enough that strategic partnerships and supplier selection decisions materially affect go-to-market outcomes.

- Global polymer and coatings leaders: Established firms offering engineered polycarbonate and coated films bring scale, validated performance grades and global distribution networks. Their portfolios typically emphasize proven, durable anti-fog solutions for high-humidity PPE and displays.

- Regional fabricators and specialty coaters: Several regional manufacturers provide nimble customization, rapid prototyping and integrated fabrication services—advantages for customers requiring bespoke dimensions or local inventory strategies.

- Recent activity to monitor: Capacity expansions and plant-level investments announced by major sheet producers signal improved availability for multiwall and corrugated formats in North America. At the same time, innovation from specialized coaters—such as PFAS-free formulations and ultra-durable hydrophilic treatments—creates new price-performance inflection points.

Companies spotlight

The report includes detailed profiles and competitive benchmarking of incumbent and emerging suppliers, with impartial assessments of technical capabilities, geographic reach and innovation roadmaps. Among the firms we analyze in depth are:

- Global polycarbonate and film developers offering long-term anti-fog grades and high-performance coatings suitable for visors and displays.

- Specialty coating providers focusing on permanent anti-fog and abrasion-resistant chemistries, including new PFAS-free lines.

- Regional sheet manufacturers and fabricators that combine surface treatments with local production and custom fabrication services for agricultural and architectural applications.

For practitioners conducting supplier due diligence in 2026, our supplier scorecards reduce discovery time by highlighting validated performance claims, warranty profiles and capacity constraints.

What the report delivers — practical, operational content

This is not a high-level outlook; the deliverable is engineered to be applied directly within commercial and engineering cycles:

- Actionable go-to-market frameworks that map product variants to prioritized end markets and buyer personas.

- Procurement playbooks including contract structures, hedging scenarios, and a supplier risk matrix calibrated to raw-material and trade-policy volatility.

- CapEx guidance and phased expansion scenarios for manufacturing executives—ranging from niche coating lines to full-sheet extrusion capacity.

- Regulatory compliance templates and reformulation timelines that translate jurisdictional controls into product change roadmaps.

- Pricing models and margin simulations that illustrate sensitivity to BPA feedstock swings and coating-cost differentials.

- M&A and partnership decision frameworks optimized for acquiring technology versus acquiring capacity.

Strategic recommendations for 2026

Based on a synthesis of market sizing, supplier intelligence and scenario modeling, PW Consulting recommends a set of prioritized actions for manufacturers, OEMs and large buyers:

- Adopt a tiered procurement architecture: Combine global strategic suppliers for validated, high-performance grades with regional fabricators for localized service and rapid replenishment.

- Invest in formulation resilience: Accelerate development or qualification of PFAS-free and alternative UV stabilizer chemistries to stay ahead of regulatory timelines and reduce rework risk.

- Prioritize validated field-life metrics: Require multi-season or multi-year performance verification for coating claims—especially for greenhouse, architectural and refrigerated-display applications—before awarding long-term contracts.

- Scenario-proof capex plans: When sizing new capacity, model upside to demand (medical surge, agricultural retrofits) and downside (material-cost shocks, tariff impacts), and consider modular expansions or toll-coating partnerships to keep fixed commitments manageable.

- Embed regulatory change management: Convert regulatory watchlists into trigger-based product development milestones so compliance activities are funded and scheduled, not reactive.

- Explore collaborative R&D: For OEMs, co-investing in coating R&D with trusted suppliers can secure first-mover advantage on durable, environmentally compliant anti-fog solutions.

How to use this preview — and where to find more

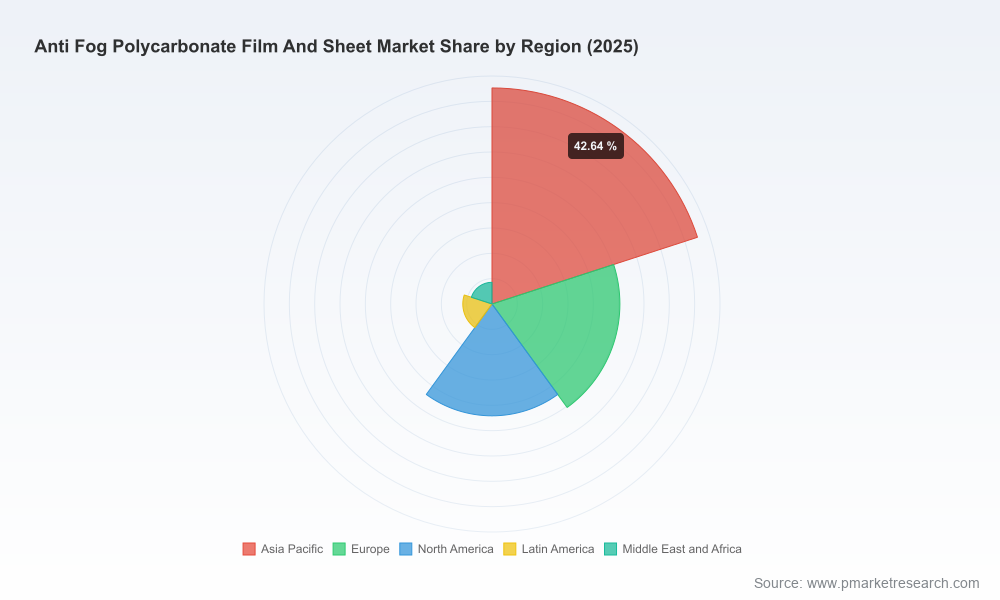

This briefing intentionally omits detailed subsegment tables and granular regional/application level shares to preserve the full analytical value of the source report and to encourage direct engagement. PW Consulting’s full report contains the proprietary segmentation matrices, supplier scorecards, and downloadable modeling templates that enable teams to plug in their own assumptions and run bespoke scenarios.

For procurement leaders, product managers and corporate strategists preparing for 2026, the full study provides the evidence base and operational tools required to accelerate decision cycles while managing regulatory and raw-material risks. If your 2026 plan includes capacity investments, formulation changes, or new market entry, our report converts forecast theory into a prioritized action plan.

Closing note

Anti-fog polycarbonate films and sheets are transitioning from specialized solutions to embedded specifications across multiple humidity-sensitive sectors. The market’s steady growth and evolving technology landscape reward players who combine commercial discipline with technical foresight. PW Consulting’s study equips decision-makers with the forward-looking scenarios, supplier intelligence, and executable playbooks needed to make confident, timely choices in 2026—without having to reinvent the analytical groundwork.

For detailed analysis of this topic, please visit the official page:Anti Fog Polycarbonate Film And Sheet Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com