PW Consulting: Military Tactics Simulator Market Forecast to Expand at a 7.42% CAGR Through 2032

Other |

2026-07-02 08:06:25

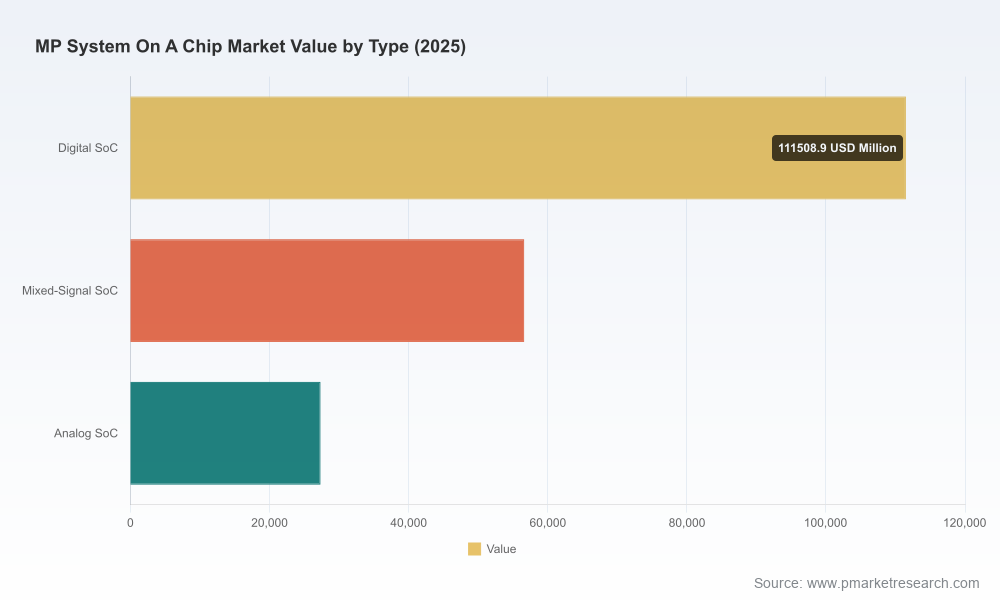

As enterprises finalize product roadmaps, capital allocation, and strategic partnerships for 2026, the Mp System-on-Chip (SoC) market is emerging as a decisive battleground for performance, integration, and supply-chain resilience. PW Consulting’s latest market study — anchored on 2025 as the base year and projecting through 2032 — shows the Mp SoC market surpassing USD 195.5 billion in 2025 and expanding to an estimated USD 363.16 billion by 2032, representing a compound annual growth rate (CAGR) of 9.25% for the forecast period. These macro dynamics underline a multi-year investment thesis: incumbents and challengers who synchronize node migration, heterogeneous integration, and customer-centric system design will capture outsized value.

Mp System On A Chip Market

Three concurrent technical and demand-side forces are reshaping the Mp SoC landscape. First, relentless functional consolidation — tighter coupling of CPU, GPU, AI accelerators, modem/IP, and domain-specific accelerators — is creating higher value per chip while increasing design complexity. Second, advanced process-node adoption and packaging innovations are compressing the performance-cost curve. Industry signals point to first-tier smartphone SoC manufacturers transitioning to 2nm process technology in 2026, a development that will materially change competitive positioning across mobile, automotive, and edge compute markets. Third, heterogeneous packaging and chiplet ecosystems are maturing: advanced interposers, high-bandwidth memory stacks, and chiplet standards are shifting the trade-offs between monolithic scaling and composable architectures.

Mp System On A Chip Market

These technical trends intersect with macro policy and infrastructure shifts. Public programs and export-control regimes continue to alter supplier footprints and technology access, prompting onshore capacity buildouts, alternative sourcing strategies, and an emphasis on “design for supply continuity.” Taken together, these forces create a market that is both large and strategically nuanced — one that rewards clarity of execution more than size alone.

Mp System On A Chip Market

Market structure. The market demonstrates a meaningful degree of concentration: the top three firms account for roughly 49% of industry revenues, while the top five capture over 62%. This configuration creates room for scale-driven incumbents to use vertical integration and ecosystem control as defensive advantages, while also giving differentiated players significant niche power.

Tier-1 integrators. Companies that couple world-class process partnerships with IP ecosystems and software stacks — firms such as Qualcomm, Apple, MediaTek, Samsung, Intel, AMD, and NVIDIA — are using integration strategies to extend beyond traditional boundaries (e.g., mobile into automotive and cloud AI into edge SoCs). Their advantages come from end-to-end co-optimization across device, OS, and silicon.

Domain specialists and systems houses. Players like NXP, STMicroelectronics, Texas Instruments, Broadcom, and select imaging SoC vendors focus on system-specific attributes: safety, real-time processing, analog integration, and specialized ISPs. These firms derive defensibility from certification ecosystems, long-term OEM relationships, and domain-specific roadmaps.

Foundry and packaging enablers. Leaders in foundry and packaging technologies (including marquee process adopters and advanced packaging providers) are catalyzing new product classes: multi-die high-performance SoCs, HBM-enabled compute modules, and cost-optimized mobile SoCs at cutting nodes. Their roadmaps — and the timeliness of node ramps — will determine who can deliver next-gen performance first.

Process node acceleration: Industry activity around 2nm adoption in 2026 is compressing product cycles. For product owners, this means earlier decisions on IP licensing, verification resource allocation, and thermal/system integration to avoid being priced out of high-performance segments.

Packaging and chiplet standardization: The advancement of large reticle-size interposers and high-yield packaging options is enabling heterogeneous integration at scale. Standardization efforts around chiplet interconnects are lowering integration risk for multi-supplier SoC strategies.

Regulatory and geopolitical headwinds: Export controls and national semiconductor initiatives are creating divergence in equipment availability and capital incentives. Enterprises must now evaluate geopolitical scenario outcomes as a material input to capacity planning and supplier selection.

Domain awards and product demonstrations: Collaborative wins in automotive-grade interfaces and L4-capable subsystems indicate how software-hardware co-design is accelerating deployment timelines for safety-critical applications.

Prioritize node-plus-packaging roadmaps. Selecting a process node without a packaging and system-integration plan exposes firms to substantial thermal and cost risk. Strategic roadmaps must tightly couple node selection, packaging partner commitments, and target system BOMs.

Build modularity into product platforms. Embrace chiplet-friendly designs and software abstraction layers that enable incremental performance upgrades without full redesigns; this reduces time-to-market and aligns procurement with foundry cadence.

Adopt a supplier-flexibility stance. With policy-driven capacity shifts, companies should establish dual-sourcing where possible, qualify alternative toolchains, and consider strategic inventory holdings for critical IP blocks and packaging substrates.

Reframe M&A and ecosystem plays. Where scale is essential, pursue capabilities that shorten time-to-node adoption (IP, packaging tech, verification stacks). In niche segments, invest in domain-specific differentiation — safety features, analog integration, or specialized ISPs — rather than general-purpose performance arms races.

Embed regulatory risk in financial planning. Export controls and incentive programs materially affect capex economics. Scenario-based capital planning that includes regulatory variance is now table stakes for Board-level reviews.

The report is purpose-built for corporate strategists, CTOs, procurement leads, and corporate development teams preparing for 2026. Core deliverables include:

Proprietary market model with base-year reconciliation and 2026–2032 forecasts (by volume and revenue) that drive NPV-sensitive decision-making.

Competitive scorecards and capability maps for leading vendors across performance, integration, software ecosystem, and go-to-market reach.

Scenario analytics that quantify the P&L and timeline impact of alternative node-adoption paths, packaging choices, and chiplet adoption curves.

Actionable go-to-market playbooks for SoC developers and systems integrators — covering product architectures, certification roadmaps, and tiered sourcing strategies.

Supplier and foundry risk matrix with mitigation levers, including localization, strategic inventory, and contract structures tailored to semiconductor supply chains.

M&A and partnership checklist with integration milestones, IP due-diligence templates, and value-capture mechanisms for bolt-on technology acquisitions.

Executive teams: Use the report’s scenario outputs to stress-test capital plans and to prioritize investments that shrink time-to-revenue across the 2026–2028 window.

Product teams: Align verification and system-integration milestones to the projected cadence of advanced-node availability and packaging vendor readiness to avoid last-minute compromises.

Supply-chain leads: Deploy the supplier risk matrix to sequence supplier qualifications, contractual protections, and inventory strategies aligned to targeted product launches.

Corporate development: Apply the M&A checklist and vendor scorecards to identify acquisitions that unlock roadmaps and accelerate access to key IP or packaging capabilities.

We combine a macro-validated market model with ground-level supplier intelligence and engineering-aware scenario planning. That means our forecasts are not just top-down extrapolations; they reconcile to engineering milestones, node ramps, packaging readiness, and demonstrated product timelines from major vendors. We also provide practical decision-support artifacts — for example, contract language templates and integration checklists — that translate strategic choices into executable programs.

This executive release highlights the strategic contours of the Mp SoC market and the near-term choices that will shape competitive outcomes. The full PW Consulting report contains the detailed regional, application, and type-level breakdowns, complete vendor scorecards, and the downloadable scenario and financial models referenced above. Those granular segment tables and proprietary forecasts are accessible on the report page for clients who require the detailed inputs to operationalize 2026 plans.

For enterprise leaders preparing budgets, partnerships, or M&A activity in 2026, the report provides the templates and models to convert macro opportunity into actionable programs — helping you decide where to invest, where to partner, and where to defend.

For detailed analysis of this topic, please visit the official page:Mp System On A Chip Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com