Technological Advancements Fuel Growth in the Astaxanthin Market Industry

Other |

2026-05-07 07:03:15

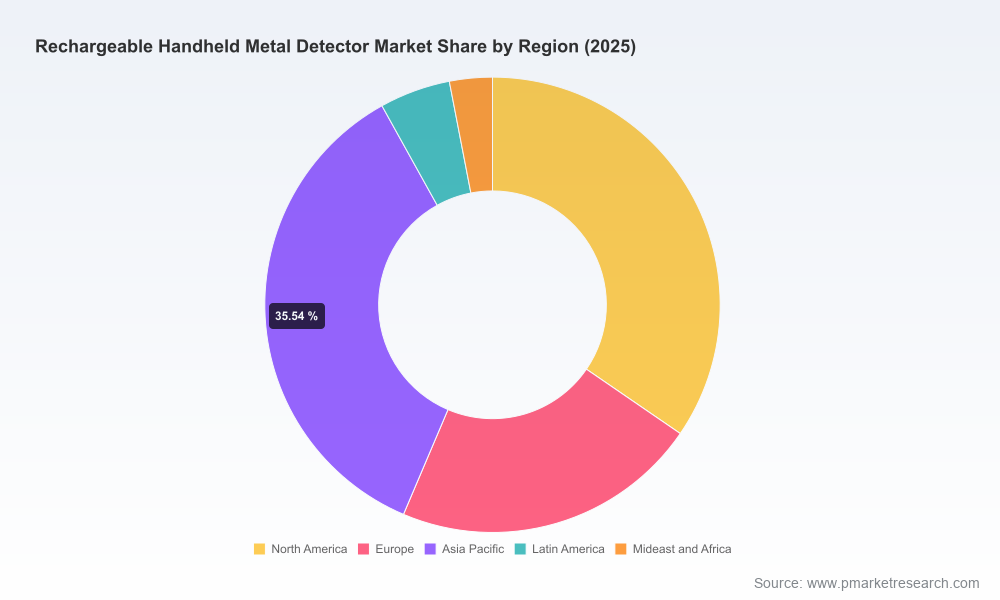

PW Consulting’s latest market intelligence on the Rechargeable Handheld Metal Detector market synthesizes five years of historical performance (2020–2025) and delivers a forward-looking view across the 2026–2032 forecast horizon. The market — measured in USD Million — reached approximately USD 240.5 Million in the report base year (2025) and, under our base case, is projected to expand to roughly USD 367.64 Million by 2032, implying a compound annual growth rate (CAGR) of about 6.25% through the forecast period. This briefing highlights the elements of our analysis that matter most to boards, procurement leads, product strategists, and M&A teams preparing decisions in 2026 — while reserving the full segmented intelligence for the complete report.

Rechargeable Handheld Metal Detector Market

Procurement and capex timing: Buyers in aviation, corrections, events, and critical infrastructure are balancing replacement cycles with evolving technical standards. The market’s steady mid-single-digit CAGR signals that incremental upgrades — rather than cyclical replacements — will dominate purchasing patterns, increasing the importance of lifecycle cost analysis and service offerings.

Rechargeable Handheld Metal Detector Market

Standards and compliance are shifting from product nicety to procurement gatekeeper: New and draft NIJ standards, and heightened expectations for traceable calibration and documented test regimes, are already reshaping vendor selection criteria.

Rechargeable Handheld Metal Detector Market

Battery and charging technology is a product differentiator: Lithium‑ion architectures with USB‑C charging and 15–100+ hour operation windows are now a table stake for serious vendors; energy management and user ergonomics materially affect total cost of ownership (TCO) in high-utilization environments.

Consolidation and concentration: The competitive landscape shows meaningful market concentration among a small set of global incumbents, but a broad OEM base remains active — creating unusual opportunities for vertical integration, private-label supply, and strategic partnerships.

Operational resilience matters: Supply-chain risk for critical raw materials and battery components requires buyers and manufacturers to develop alternative sourcing strategies and inventory buffers to avoid disruptions during peak procurement windows.

Integrated market sizing and methodology — transparent approach reconciling bottom-up shipments and top-down demand modeling for 2020–2025 and projections through 2032 (USD Million).

Segment architecture — device types, applications, and regional roll-ups, with scenario-modeled forecasts and sensitivity to regulatory and technology shifts (note: the executive summary here intentionally omits the report’s full segment tables).

Technology and product roadmap — in-depth assessment of battery chemistries, charging interfaces, multi-frequency detection, waterproofing standards, and embedded diagnostics tied to field‑maintenance economics.

Competitive profiles and benchmarking — vendor scorecards covering product portfolios, compliance posture, channel models, manufacturing footprints, pricing bands, and aftermarket services.

Go‑to‑market playbooks — tailored strategies for OEMs, branded vendors, system integrators, and distributors; channel economics, promotional levers, and buyer personas for primary end‑markets.

Procurement & RFP toolkits — sample technical specs, evaluation matrices, TCO templates, and warranty & service contract clauses optimized for high-utilization deployments.

M&A and partnership screening — a deal-ready framework for identifying targets across capabilities (battery expertise, RF sensing, software diagnostics), with valuation heuristics and synergies mapping.

Our company analyses cover the leading global brands and a diversified OEM ecosystem. Incumbents with strong brand recognition and service networks continue to dominate institutional channels, while lower-cost manufacturers and OEMs compete aggressively on price and customization for emerging markets and second‑tier buyers.

Garrett Metal Detectors (Garland, Texas) — consistently advances product ergonomics and battery convenience, recently launching models that emphasize USB‑C charging, improved runtime and environmental ruggedness. Their product cadence highlights an approach centered on incremental innovation, certification, and broad channel reach.

CEIA (Arezzo, Italy) — positions itself on the performance and standards front, offering high‑sensitivity models that align with NIJ specifications; appeal is strongest where procurement mandates rigorous compliance and traceability.

Securina Detection System and other specialized Chinese manufacturers — deliver cost‑effective, feature‑rich devices (USB‑C, vibration alerts, configurable sensitivity) that are attractive for large-volume deployments such as education, events, and some transport segments.

Global systems players (Smiths Detection, NUCTECH, Autoclear) — integrate handhelds within broader security portfolios; their competitive advantage lies in systems-level contracts and cross-sell into aviation and government accounts.

Specialist innovators (GXC Inc., Westminster Group, various Shenzhen and Dongguan OEMs) — differentiate on battery life claims, compliance with NIJ standards, or cost and manufacturing flexibility. These players are often targets for strategic partnerships or white‑label arrangements.

Market concentration is meaningful: the top three players account for a material share of industry revenues while the top five amplify that concentration further. This two‑tier structure (global incumbents + agile OEMs) creates tactical windows for entrants that can marry compliance, service, and competitive pricing.

Product launches: Flagship and law‑enforcement focused launches during 2025–2026 underscore an emphasis on multifrequency detection, ruggedization (higher IP ratings), and USB‑C rechargeable architectures. These product moves accelerate the replacement cycle in mission‑critical accounts.

Standards: NIJ standards and drafts continue to influence RFP language and acceptance criteria. Buyers are increasingly embedding compliance checks into procurement stages, not after delivery.

Battery evolution: The industry now quotes operational runtimes ranging from modest half‑day use to multi‑day endurance claims — a variable that fundamentally changes service intervals, charging infrastructure needs, and aftermarket revenue opportunities.

Demand drivers: Rising public security concerns and the commercialisation of large‑scale events and transport hubs are sustaining demand across institutional and commercial segments.

For buyers (airports, event operators, government): Tighten technical specifications to include battery lifecycle metrics, standard charging interfaces (USB‑C), and environmental ingress protections. Combine procurement with outcome‑based SLAs to shift supplier incentives toward reliability and uptime.

For manufacturers: Prioritize battery management and software diagnostics as monetizable features. Invest selectively in NIJ compliance testing and visible certifications to lower procurement friction in institutional channels.

For distributors and integrators: Build bundled offers (device + spare batteries + charging stations + managed service) to increase gross margins and customer stickiness; leverage local service capabilities as a competitive moat.

For strategics and PE: Target OEMs or niche innovators with differentiated battery tech, ruggedization IP, or compliance testing capabilities. Synergies on manufacturing scale and channel access are the fastest routes to accretive growth.

Operationally: De-risk supply chains for battery cells and critical electronic components through multi‑sourcing and safety stock strategies. Quantify component lead times into procurement models to prevent project slippage.

Pilot and iterate: Before wide rollouts, run structured pilots that capture runtime, maintainability, false alarm rates, and user ergonomics. Use pilot data to refine procurement scoring and to negotiate volume discounts tied to measured performance.

PW Consulting combines market forecasting, vendor benchmarking, procurement toolkits, and M&A advisory into modular engagements tailored to executive priorities. Our services include scenario-based forecasting, vendor due diligence, technical validation, RFP drafting and evaluation, TCO modeling, and negotiation support — each designed to move clients from insight to execution in 60–90 days.

This briefing provides the strategic context and the operational levers that matter for near-term decisions. For the granular segmentation, country-level forecasts, vendor market shares, pricing matrices, and the full suite of procurement templates and benchmarking scorecards, consult the complete Rechargeable Handheld Metal Detector Market report. PW Consulting’s full report contains the empirical tables and playbooks needed to convert these insights into executable plans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Rechargeable Handheld Metal Detector Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com