Energy Storage Bidirectional AC-DC Converter Market — Strategic Preview for 2026 Decision‑Makers

PW Consulting today releases a strategic preview of our forthcoming Energy Storage Bidirectional AC-DC Converter Market report. Prepared as an executive intelligence piece for corporate strategy, product management, procurement and investor teams, this briefing synthesizes our market sizing, competitive mapping, regulatory scanning and decision playbooks specifically calibrated for actions in 2026. The aim: give executives the evidence‑based orientation they need to prioritise investments and partnerships this year, while preserving the detailed segment economics and vendor scorecards for subscribers to the full report.

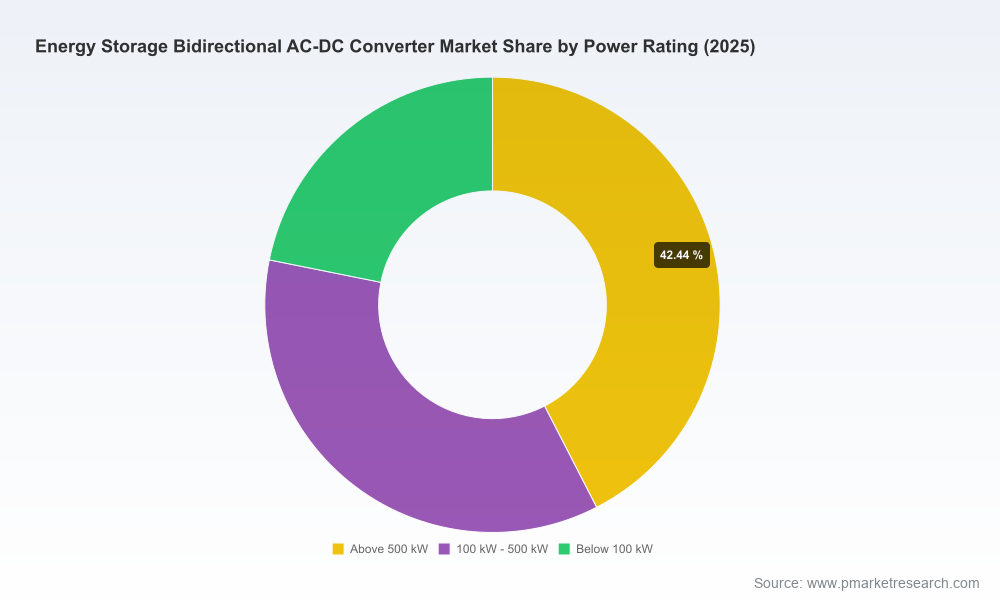

Energy Storage Bidirectional Ac Dc Converter Market

Market at a glance — macro scale and growth trajectory

The bidirectional AC‑DC converter market for energy storage has entered a sustained scale-up phase. After five years of accelerated expansion, our base‑year estimate for 2025 places the global market at approximately USD 3,950 Million (revenue basis). Under the set of technology adoption, cost decline and policy scenarios we model, the market is forecast to grow at a compound annual growth rate (CAGR) of roughly 16.5% across the 2026–2032 forecast window, reaching a multi‑billion‑dollar annual market by the end of the period.

Energy Storage Bidirectional Ac Dc Converter Market

Historic dynamics matter for near‑term strategy: installed demand and product variety expanded rapidly from 2020 to 2025, driven by parallel pushes in utility‑scale deployment, commercial & industrial (C&I) applications and growing residential and vehicle‑grid integration pilots. That acceleration both enlarges the commercial opportunity and raises technical interoperability and procurement complexity for buyers and integrators alike.

Energy Storage Bidirectional Ac Dc Converter Market

What this report delivers — practical intelligence for 2026 actions

- Quantified market sizing and scenario forecasts (2026–2032) to support budgeting, target setting and risk‑adjusted IRR calculations.

- Vendor benchmarking and technology gap analysis that compares topology choices (e.g., three‑level vs string approaches), modular architectures, efficiency bands and lifecycle models (including UPS and hybrid microgrid use cases).

- Procurement playbooks and RFP templates tailored to different buying profiles — utility procurement, C&I offtakers, aggregator platforms and residential rollouts — with scoring criteria for both capex and total cost of ownership.

- Regulatory impact assessments and a compliance roadmap covering emerging grid codes, carbon‑embedded pricing mechanisms and building energy code updates relevant to 2026 procurement decisions.

- Supply chain risk matrices and hedging strategies that map exposure to battery cell price trajectories, electronic components bottlenecks and regional content rules.

- Commercial go‑to‑market (GTM) playbooks covering channel strategies, JV and OEM models, service & software monetisation and aftermarket economics.

We design the report for immediate, operational use by strategy teams: decision calendars, milestone‑based procurement checkpoints and red‑team scenarios that stress test supplier roadmaps against grid code and material cost shocks. Detailed segmentation and vendor scorecards are intentionally withheld here to preserve the strategic value of the full dataset.

Competitive dynamics — who matters and why

The landscape combines well‑capitalised multinational incumbents, specialised power‑electronics houses and agile China‑based scale players. Our concentration metrics indicate an oligopolistic yet not fully consolidated market: roughly the top three vendors account for a material minority share, and the top five capture a majority share — a structure that creates both partnership opportunities and room for differentiated entrants.

- Honle Group (Germany; China operations) — Positions itself with high‑efficiency, three‑level topologies and modular cabinets scalable toward multi‑MW. Strengths: proven efficiency (>98.5% claimed), hybrid microgrid capability and multi‑mode operation (on‑grid/off‑grid/UPS). For buyers: an option where high efficiency and modular expansion are procurement priorities.

- Infypower (China) — Focus on high power density modules, isolated/non‑isolated variants and solutions targeted at industrial & commercial ESS and V2G. Strengths: compact designs and integration readiness for C&I and fleet electrification projects.

- Shenzhen UUGreenPower — Strong in residential integration and V2G charging stacks, with an emphasis on bidirectional charging modules that link home storage and EV fleets to grid services.

- Shenzhen Acadie New Energy (ANE) — Product launches in the 50–280 kW envelope show a focus on modular cabinetisation for ESS applications and testing integration; recent 105 kW releases reflect a push to capture mid‑market on‑grid and off‑grid segments.

- Epic Power Converters (Spain) — Niche player in bidirectional DC/DC and hybrid storage interfaces, attractive for projects combining supercapacitors, battery hybridization and energy recovery applications.

- ABB and Delta Electronics — Large, diversified incumbents offering high‑power PCS and bi‑directional systems for utility and traction markets, with global delivery capability and deep grid‑code engineering capacity.

- Sungrow — Strong scale vendor for utility‑scale applications, combining liquid cooling and string PCS approaches that address grid stability and high‑throughput deployments.

Recent market activity underlines the strategic vectors for 2026: product refreshes and commercial wins (e.g., Shenzhen Acadie’s 105 kW product launch in early 2026 and Hitachi/KS Energy collaborations on high‑voltage BESS projects) point to continued segmentation by use‑case and voltage class rather than a single convergent architecture. Commissioning of MW‑scale projects with mid‑power PCS also validates a mix of modular and medium‑power approaches in real deployments.

Regulatory and cost signals shaping 2026 procurement

- Policy drivers: California’s 2025 energy code update (effective 2026) and U.S. national directives on grid impact evaluation create near‑term demand pull in specific markets and heighten compliance requirements for projects sited in regulated jurisdictions.

- Carbon‑accounting influences: Progress on market mechanisms such as the EU’s carbon border adjustment initiatives is driving buyers to factor embedded emissions into supplier selection and to favour localised or low‑carbon supply chains.

- Battery and component cost trajectories: Public analyses indicate continued declines in utility‑scale battery capital costs and cell prices (including LFP dynamics), which compress project capex and change the relative economics of converter design choices (e.g., power vs energy tradeoffs, cooling strategies).

Implication: procurement teams must now balance unit economics with compliance timelines and lifecycle carbon footprints. Delaying procurement to chase lower cell prices may reduce up‑front capex but increases exposure to changing regulatory windows and missed revenue from early market participation.

Recommended strategic moves for 2026

- Adopt a split‑track procurement posture: secure modular, proven converter platforms for near‑term projects while keeping options for next‑generation high‑efficiency modules for follow‑on deployments. Structure contracts with clear upgrade and interoperability clauses.

- Prioritise suppliers with demonstrated grid‑code engineering and system‑level integration capabilities. For utility and traction projects, deep experience in commissioning and dynamic control wins tests and interconnection approvals.

- Hedge supply chain exposure: negotiate conditional price review clauses on major cell and component inputs, consider pre‑payment or offtake arrangements where necessary, and evaluate geographic diversification or local assembly to mitigate carbon and trade rule risk.

- Invest in firmware/software differentiators and O&M frameworks. Margins and lifetime value are increasingly driven by controls, lifecycle services and performance maximisation rather than the converter hardware alone.

- Explore targeted M&A or strategic partnerships: for established OEMs, tuck‑ins that add V2G, residential inverter stacks or DC‑coupled hybrid solutions can accelerate portfolio breadth; for developers, partnerships that secure long‑term supply and service SLAs are decisive.

- Embed regulatory scenario planning into procurement committees: require supplier evidence on embedded emissions, certification roadmaps and contingency plans for sudden code changes (e.g., wildfire‑related suspensions or new interconnection requirements).

How PW Consulting supports 2026 decision cycles

Our full report and advisory packages include vendor scorecards, downloadable RFP templates, techno‑economic models calibrated to regional tariff and ancillary service markets, scenario stress tests for policy and cost shocks, and a procurement readiness checklist for 0–24 month project timelines. We also offer bespoke workshops to translate these insights into supply‑side negotiation strategies and product roadmaps.

This preview is designed to orient executives to the major inflection points in 2026. For teams preparing capital allocations, supplier negotiations or product investments this year, our deep datasets — including the full segmentation, vendor benchmarking and forecast tables — will materially shorten time to decision and reduce execution risk. Access to the complete report and supporting models is available via the PW Consulting publications page. Subscribers benefit from a follow‑on briefing that aligns the analysis to a client’s portfolio and procurement cadence.

PW Consulting remains focused on turning technical complexity into executable strategy. The bidirectional AC‑DC converter market is transitioning from early adoption to commercial scale; the choices made in 2026 will determine who captures the growth, who protects margins and who becomes a preferred systems partner in the next decade.

For detailed analysis of this topic, please visit the official page:Energy Storage Bidirectional Ac Dc Converter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com