RNA Therapeutics and Vaccines Market: Strategic Briefing for 2026 Decision-Makers

Executive summary

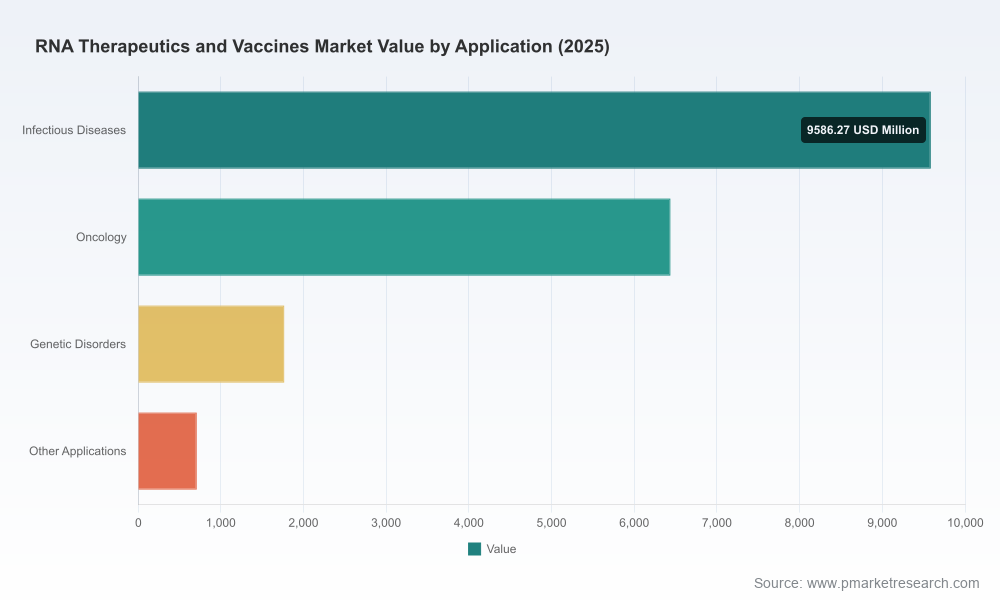

The RNA therapeutics and vaccines market has transitioned from breakthrough curiosity to mainstream strategic priority. Our PW Consulting market model (base year 2025) shows the industry expanding from roughly USD 8.5 billion in 2020 to USD 18.5 billion in 2025, and projecting to exceed USD 42 billion by 2032 at a compound annual growth rate (CAGR) of 12.5% over the 2026–2032 forecast window. Competitive concentration is material — the three largest players capture just over half of the market, and the top five command nearly two‑thirds — a structure that underpins both opportunity and barrier dynamics for new entrants and established players alike.

Rna Therapeutics And Vaccines Market

Why this matters for 2026 strategy

- Timing matters: 2026 is the hinge year where platform validation, regulatory precedent, and commercialization muscle converge. Firms that align clinical development, manufacturing scale, and payer engagement now will capture disproportionate share as the market professionalizes.

- Platform advantage will determine value capture: mRNA, RNAi and antisense technologies are moving from “science projects” to product portfolios. Proprietary delivery systems, thermostable formulations, and robust GMP capacity are the levers that translate R&D into realized revenue.

- Operational resilience is a competitive differentiator: Cold‑chain complexity, localized manufacturing constraints, and raw‑material volatility mean supply‑chain strategy is no longer a cost center but a strategic battleground.

- Concentration creates strategic playbooks: With >50% share among the top three players, alliances, licensing, and targeted M&A are realistic routes for mid‑sized firms to accelerate time to market without competing head‑on.

What the report delivers — practical, decision‑grade intelligence

Our Rna Therapeutics And Vaccines Market report is built around the explicit question senior leaders ask in 2026: “What should we do next quarter to materially improve our odds over the next three years?” To answer that we combine quantitative market modelling with tactical playbooks and executable tools.

Rna Therapeutics And Vaccines Market

- Full market sizing and validated growth scenarios (2026–2032), including upside/downside sensitivity tied to regulatory and supply‑chain inflection points.

- Pipeline and product‑level mapping that ties clinical stage, delivery modality and commercialization risk—presented as prioritization matrices to inform portfolio resource allocation.

- Manufacturing and capacity intelligence: a practical capacity map, lead times for key equipment, and an assessment of contract development and manufacturing organization (CDMO) options.

- Supply‑chain stress tests: vendor concentration analysis for IVT reagents, nucleotides and lipid excipients, and cost‑impact models reflecting recent raw‑material inflation.

- Regulatory & reimbursement playbooks: step‑by‑step guidance for accelerated approvals, leveraging precedent for updated seasonal vaccines, and payer evidence expectations for therapeutics beyond infectious disease.

- Commercial readiness and launch templates: channel strategies for vaccine campaigns, pricing levers, and post‑launch surveillance frameworks tailored to RNA modalities.

- Deal‑making toolkit: valuation benchmarks, earn‑out structures, and integration checklists for licensing or M&A in RNA assets and manufacturing capacity.

- Interactive decision support assets: downloadable ROI calculators, go‑to‑market checklists, and scenario dashboards to stress test strategic options.

Competitive landscape: who to watch and why

The market is anchored by platform owners who combine clinical pipelines with commercial footprints. Our analysis highlights distinct strategic archetypes:

Rna Therapeutics And Vaccines Market

- Platform incumbents with commercial scale: Companies that have translated mRNA platforms into approved vaccines and are now expanding indications and lifecycle variants. Their strengths: regulatory relationships, established manufacturing runs, and revenue streams that subsidize platform expansion.

- Specialist innovators: Firms focused on next‑generation delivery (self‑amplifying RNA, mucosal routes) or niche indications. These players are the primary sources of disruptive technology and often become preferred partners or acquisition targets.

- RNA modality veterans: Companies with deep RNAi or antisense expertise that bring validated pharmacology and regulatory experience in rare and genetic diseases—important for therapeutic diversification beyond vaccines.

Representative companies covered in our competitive chapter include well‑known platform holders with marketed mRNA vaccines and broad pipelines, delivery innovators advancing intranasal and self‑amplifying approaches, and RNA therapeutics specialists with approved siRNA and antisense medicines. The chapter synthesizes strategic intent, pipeline timing, manufacturing footprints, and likely partnership corridors — enabling buyers to map potential allies or acquisition targets by capability rather than by headline size.

Near‑term catalysts and headwinds shaping 2026 moves

- Regulatory momentum and precedent: Continued active review of updated mRNA vaccines has created a faster pathway for variant‑adapted shots and will shape regulatory expectations for safety data in expanded indications. Expect regulators to refine guidance on platform comparability and bridging data.

- Commercial approvals and lifecycle updates: Recent and anticipated approvals for updated seasonal and variant vaccines accelerate market normalization for RNA products, changing commercial launch timelines and inventory planning.

- Technological advances in delivery and stability: Progress toward thermostable lipid‑nanoparticle (LNP) formulations and mucosal delivery expands addressable markets by lowering cold‑chain barriers, but these remain development and scale risks in 2026.

- Supply‑chain and cost pressure: IVT reagents and key enzymes have experienced significant cost increases recently; firms must model input‑cost pass‑throughs, supplier diversification, and in‑house production economics.

- Funding and collaboration flows: Public and consortium funding for pandemic preparedness and infectious disease platforms is creating co‑investment opportunities for proof‑of‑concept and scale‑up initiatives.

- Geopolitical overlay: Tariff policy and export controls on specialized materials can materially affect production economics and sourcing strategies for globally integrated manufacturers.

Actionable strategic recommendations for 2026

- Prioritize platform de‑risking in core indications: Use the report’s prioritization matrix to shift near‑term R&D spend toward candidates with the clearest regulatory precedent and commercial pathways, while staging higher‑risk bets alongside milestone‑based partnerships.

- Invest in modular manufacturing capacity: Opt for flexible, geographically diversified capacity that can be repurposed across vaccine and therapeutic production to hedge demand uncertainty and reduce cold‑chain leg‑risk.

- Lock supply of critical inputs: Negotiate strategic supply agreements, consider backward integration for enzymatic reagents, and build multi‑tier supplier lists to mitigate raw‑material inflation and lead‑time spikes.

- Design reimbursement evidence plans now: Generate early real‑world evidence and health‑economic models for priority assets—payers will demand comparative effectiveness beyond regulatory approvals, especially for non‑acute indications.

- Targeted M&A and partnerships over scale‑on‑scale fights: Focus on acquiring delivery capabilities, CDMO capacity, or regulatory talent that accelerates commercialization rather than expanding broad therapeutic breadth without clear synergies.

- Operationalize regulatory engagement: Formalize pre‑submission dialogues with regulators and build bridging strategies for platform modifications to streamline future approvals.

- Scenario plan for logistics shocks: Create contingency plans for cold‑chain disruptions and evaluate thermostable formulation adoption as a strategic hedging lever.

How PW Consulting can support your 2026 decisions

The Rna Therapeutics And Vaccines Market report is purpose‑built to convert market intelligence into boardroom‑ready decisions. If your near‑term priorities include portfolio triage, CDMO selection, manufacturing site investment, or targeted M&A, our report furnishes the data, decision frameworks, and negotiated playbooks to act with conviction. The public executive brief above is a strategic trailer — the full report contains the granular segment modelling, supplier scoring, and scenario dashboards executives use to commit capital and resources in 2026.

To access the complete analysis, including the segment‑level forecasts, detailed competitive scorecards, and the downloadable decision tools, please consult the full report on our site or contact PW Consulting for a tailored executive briefing and workshop.

For detailed analysis of this topic, please visit the official page:Rna Therapeutics And Vaccines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com