Merchant Cash Advance Market Share: Current Trends and Future Outlook

Networking |

2026-03-25 09:38:19

As industrial laser processing continues to migrate toward higher precision, greater throughput and lower total cost of ownership, the solid-state laser segment is emerging as a strategic platform for manufacturers, system integrators and investors. Our latest PW Consulting report benchmarks the market through 2025 and delivers a forward-looking forecast for 2026–2032, revealing a steady industry expansion underpinned by a 7.72% compound annual growth rate (CAGR). The market’s measured growth trajectory — from roughly USD 3.14 billion in 2025 to beyond USD 5.28 billion by 2032 — creates a narrow window in 2026 for companies to translate R&D, capacity and commercial initiatives into durable competitive advantage.

Solid State Lasers For Laser Processing Equipment Market

Technology inflection: Ultrafast and high-brightness architectures are moving from lab demonstrations into mainstream processing workflows, changing performance and value equations for precision micro-machining, medical device fabrication and advanced electronics assembly.

Solid State Lasers For Laser Processing Equipment Market

Regulatory and trade realities: New export-control interpretations and increasingly prescriptive machine-safety standards are compressing decision timelines for cross-border deployments and product certification programs.

Solid State Lasers For Laser Processing Equipment Market

Supply volatility: Raw-material pressures on rare-earth dopants and optics components are amplifying the financial impact of procurement choices made now versus later.

This report is designed as a practitioner’s guide for 2026 decisions rather than a theoretical treatise. Key deliverables include:

Macro-to-micro forecasts: A top-down market sizing through 2032 (with a 7.72% CAGR baseline), plus layered scenarios that stress-test demand under alternative macro and supply assumptions.

Commercial playbooks: Actionable GTM strategies for OEMs and integrators — pricing levers, service monetization, segmentation-based sales motions and channel optimization frameworks.

Technology roadmaps and component deep dives: Comparative assessments of diode-pumped solid-state (DPSS), ultrafast solid-state, solid-state fiber architectures and legacy lamp-pumped systems — highlighting where incremental innovation unlocks commercial returns.

Supply-chain and procurement blueprints: Risk heatmaps, contract structures, hedging tactics and near-shoring options for rare-earth dopants, opto-electronics and high-power thermal management subsystems.

Competitive benchmarking: Strategic profiles and capability matrices for incumbents and emerging challengers, coupled with M&A and partnership scenarios calibrated to market concentration realities.

Regulation and standards matrix: Practical checklists to accelerate compliance with IEC, ISO and export-control requirements relevant to laser processing equipment.

The sector is neither a fragmented hobbyist market nor a closed oligopoly: our concentration analysis shows a mid-to-high consolidation level among top players, indicating that three leading firms account for a meaningful portion of market volume while the top five further consolidate control. This structure creates both defensive and offensive opportunities — scale economies for incumbents and niche-entry windows for focused challengers.

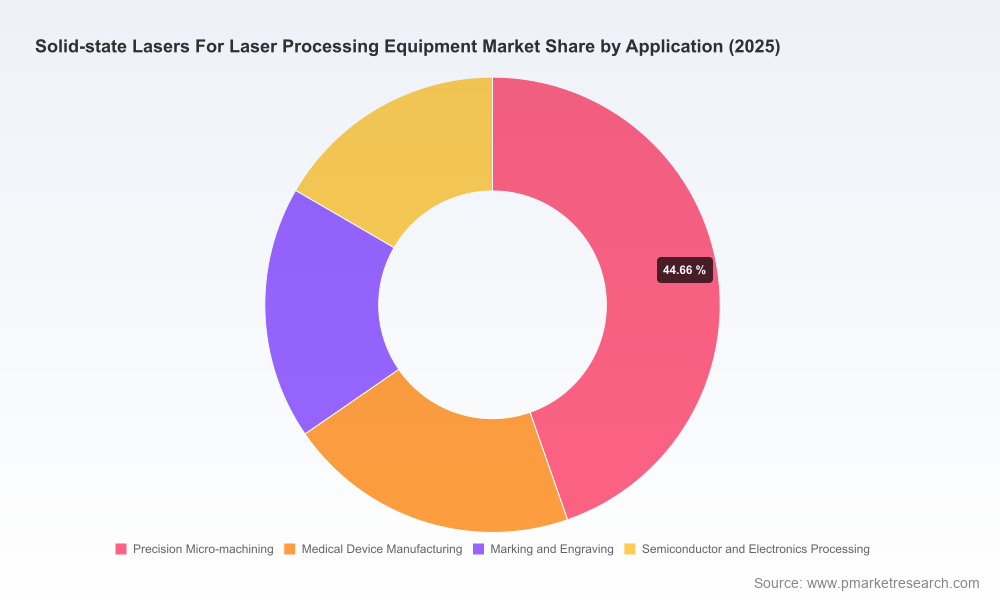

Demand drivers are multi-dimensional. End-market trends in micro-manufacturing, medical device production, marking/engraving and semiconductor/electronics processing continue to favor laser-based solutions for their repeatability, footprint and automation friendliness. At the same time, suppliers must navigate non-market forces: IEC 60825-1 and ISO 11553-series safety regimes now inform machine architecture early in the design cycle, and export-control frameworks make product routing and international sales motion contingent on classification and licensing strategies.

Solid-state laser technologies in active commercial deployment span DPSS, ultrafast solid-state and lamp-pumped architectures, with ytterbium-doped fiber lasers increasingly discussed in the same strategic space due to their solid-state nature and process-relevant attributes. Key technology trends the report analyzes include:

Pulse engineering: From pulse-on-demand ultrafast systems to high-average-power picosecond platforms, pulse control is becoming a primary performance discriminator for high-value applications.

Beam quality vs. throughput trade-offs: Manufacturers are optimizing coupling optics and thermal management to shift previously inverse relationships between beam quality and usable power.

Modularity and serviceability: Designs that de-risk maintenance and shorten MTTR are commanding higher adoption in contract manufacturing and medical device verticals.

The report includes detailed profiles of the market’s most influential players and maps strategic positioning across product, channel and innovation vectors. Highlights:

Trumpf: A long-standing leader in disk and rod solid-state platforms, leveraging integrated machine systems and recent product introductions to push ultrafast capabilities into industrial workflows.

Coherent: Focused on high-power picosecond and industrial-grade platforms, expanding its portfolio to address micromachining and high-throughput microfabrication needs.

IPG Photonics: Known for high-brightness fiber-based solid-state lasers, its strength in scalable, robust modules positions it favorably for cutting, welding and additive manufacturing applications.

Lumibird (formerly Quantel): A specialist in Q-switched Nd:YAG systems for marking and ablation, maintaining relevance through compact, cost-effective designs for OEMs.

Spectra-Physics (MKS Instruments): Active in ultrafast, high-precision offerings supporting microstructuring and surface-treatment applications where pulse shape and stability matter most.

ROFIN-SINAR (Coherent subsidiary): Continues to supply pulsed solid-state solutions for industrial cutting and drilling, supported by integration into Coherent’s broader product ecosystem.

Recent product moves — such as March 2025 launches of ultrafast pulse-on-demand systems and late-2024 introductions of high-power picosecond platforms — indicate suppliers are racing to translate laboratory-class capabilities into production-ready modules. Our competitive scoring assigns relative strengths across R&D velocity, channel reach, service networks and balance-sheet capacity to invest in scale.

Procurement sensitivity is an immediate operational risk. Neodymium and ytterbium dopants, along with specialty optics and cooling subsystems, are subject to supply constraints and price volatility — our external-source synthesis indicates dopant price swings of 20–30% in recent cycles. Export controls for high-power systems and the need to certify machines under IEC/ISO frameworks create non-linear cost and time-to-market implications for cross-border business models.

For executives calibrating budgets and corporate development agendas in 2026, PW Consulting recommends the following prioritized moves:

Lock in supply resilience: Execute multi-year supply agreements, qualify secondary dopant and optics sources, and create inventory hedges for critical components.

Focus R&D on process-adjacent differentiation: Prioritize pulse shaping, process monitoring and integration-ready modules that reduce system integration friction for OEM customers.

Segment-targeted GTM: Deploy bespoke commercial packages for high-margin verticals (e.g., medical device manufacturing) that bundle certification, service and performance guarantees.

Regulatory-first product planning: Incorporate IEC/ISO compliance and export-classification assessments into product roadmaps to avoid retrofitting costs and lost sales windows.

Pursue bolt-on M&A selectively: Target suppliers of optics, beam-delivery modules, or process-software to accelerate time-to-market and defend margin structures.

Monetize service and data: Build predictive maintenance and consumables-revenue streams to stabilize topline volatility as hardware cycles lengthen.

Scenario financial modeling: Use the report’s alternate-demand scenarios to stress-test capital allocation plans and to set trigger points for capacity expansion.

The PW Consulting report is structured to be directly integrable into board and investment committee materials. It includes downloadable models, a decision-support dashboard and a checklist-driven regulatory annex that accelerates GTM and compliance tasks. For strategy teams, the most immediate use cases are: prioritizing R&D funding, sizing bolt-on M&A targets, negotiating supplier contracts with forward-looking clauses, and defining service-based revenue pilots that start delivering within 12–18 months.

Solid-state laser technologies for processing now offer a rare combination: predictable, above-market growth (7.72% CAGR over our forecast period), an innovation window where incremental performance gains materially change an application’s economics, and a concentration profile that rewards both scale and focused specialization. 2026 is the year to convert strategic intent into structural advantage — by locking supply pathways, aligning product roadmaps with regulatory realities, and investing in commercial plays that capture the long-term value of system-level solutions.

To review the full dataset, segmented forecasts, company scorecards and downloadable strategy tools, access the complete PW Consulting Solid State Lasers For Laser Processing Equipment Market report and interactive dashboard on our website. The headline insights are here; the operational playbooks and granular segment intelligence are in the full report.

For detailed analysis of this topic, please visit the official page:Solid State Lasers For Laser Processing Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com