Primary Cell Culture Market 2026: Strategic Priorities for Executives — A PW Consulting Snapshot

Executive summary

As organizations prepare budgets and strategic roadmaps for 2026, primary cell culture has moved from a specialized laboratory input to a strategic enabler across drug discovery, regenerative medicine, and advanced in vitro modelling. PW Consulting’s latest market study — anchored on 2025 as the base year and projecting through 2032 — shows the market expanding at a sustained double‑digit pace (12.5% CAGR) and roughly doubling over the forecast horizon. This release is a precision brief: it synthesizes the market forces, regulatory inflection points, supplier dynamics, and actionable near‑term plays that senior leaders must consider when making decisions in 2026. Detailed segment-level figures are intentionally reserved for the full report to support targeted commercial and procurement actions.

Primary Cell Culture Market

Market snapshot: scale, trajectory, and concentration

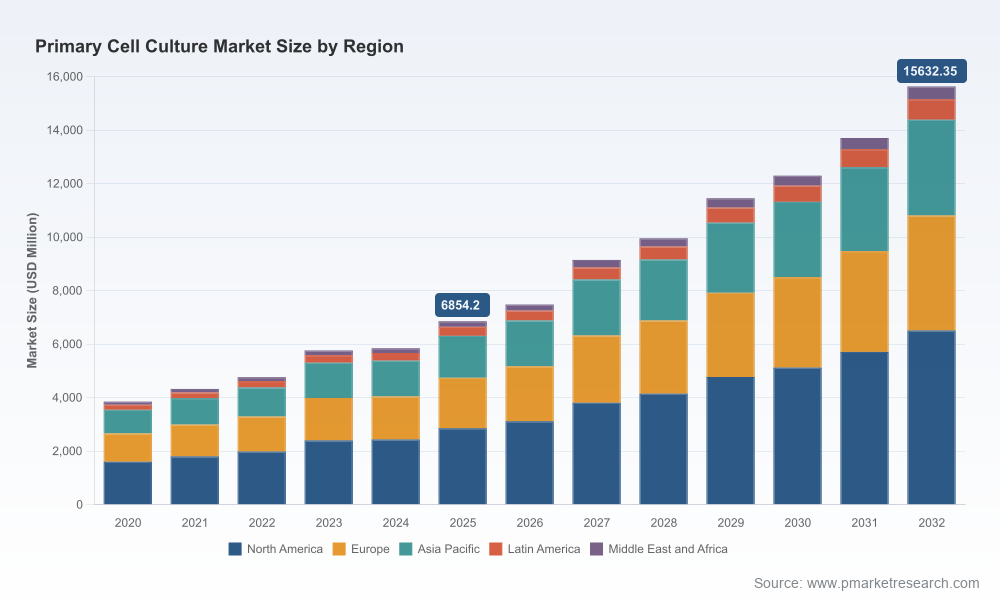

Our analysis quantifies a rapid acceleration between the historical window (2020–2025) and the forecast (2026–2032). The global market expanded from a multi‑billion USD base in 2020 to a substantially larger market by 2025, with a projected value exceeding USD 15 billion by 2032 (figures in USD Million). This growth is driven by converging scientific demand — higher adoption of primary cell models in IND‑enabling studies, organ‑on‑chip platforms, and cell therapy workflows — and by structural tailwinds such as increased public and private R&D funding.

Primary Cell Culture Market

Market structure is moderately consolidated: the top three suppliers account for a meaningful share of industry revenue, and the top five capture over half of the market. That level of concentration creates both strategic risk and opportunity. For buyers, dependency on a small set of global suppliers can expose projects to supply shocks; for suppliers, it highlights the potential upside of differentiated portfolios, scale economies, and regulatory pedigree.

Primary Cell Culture Market

Why 2026 is a decision inflection point

Several factors coalesce to make 2026 pivotal for corporate strategy:

- Regulatory momentum: Recent agency guidance has elevated the role of primary cell models in IND‑enabling safety packages for oncology and other high‑risk modalities, increasing demand for validated, well‑documented cell systems.

- Capital allocation timing: Public R&D funding and private capital — notably sizable allocations toward organ‑on‑chip and advanced in vitro platforms — will catalyze procurement cycles and strategic partnerships next year.

- Supply chain and input‑cost pressures: Price volatility in foundational reagents and episodic export controls are reshaping sourcing strategies and inventory design.

- Competitive dynamics: Suppliers are expanding catalogues, securing certifications, and showcasing new cell models at major conferences, signaling intensified product competition and faster commercialization timelines.

Operational risks and strategic levers

Executives should view primary cell culture not merely as a procurement line item but as a strategic capability that intersects R&D productivity, regulatory risk, and commercialization timelines. The most relevant levers to act on in 2026 fall into four categories:

- Sourcing resilience: Build multi‑sourced supply pools for critical cell types and raw materials; incorporate supplier scorecards that weight regulatory compliance, lot traceability, and cold‑chain reliability.

- Regulatory alignment: Prioritize cell models and suppliers that provide robust documentation aligned to recent regulatory guidance for IND submissions and clinical assay validation.

- Strategic partnerships: Consider co‑development agreements with niche providers that offer unique primary cells (e.g., organ‑specific, donor‑matched, or 3D scaffold–compatible products) to accelerate translational studies.

- Cost and inventory optimisation: Revisit stocking models for heat‑sensitive and cryopreserved materials in light of reagent cost inflation and geopolitical export controls; implement scenario planning for elevated FBS pricing and constrained supply.

Competitive landscape: what to watch

The competitive field combines multinational life science giants, specialized cell banks, and innovative niche players. Our report dissects strategy across product breadth, geographic reach, quality certifications, and go‑to‑market approaches. Selected firm‑level observations for 2026 planning include:

- Thermo Fisher Scientific (Gibco): Continues to scale with targeted product expansion, recently adding new pulmonary cell models. Their global supply footprint and integrated portfolio make them a default partner for large pharma and CROs seeking end‑to‑end consistency.

- Lonza: Focused on cryopreserved primary cells with donor‑matched offerings and optimized media. Their emphasis on clinical‑grade workflows positions them for cell therapy and regenerative medicine projects that cross from R&D into manufacturing.

- Merck KGaA (Sigma‑Aldrich): Leverages a broad reagents catalogue to bundle cells with complementary consumables and assay reagents, enabling buyers to simplify supplier management.

- ATCC: Maintains an advantage on authentication and quality certifications; their outreach at scientific conferences signals continued investment in immune and neural primary models.

- Sartorius (PromoCell): Certification achievements and serum‑free kit offerings make them attractive to labs prioritizing regulatory provenance and reduced animal‑derived inputs.

- Specialized suppliers (ScienCell, Celprogen, AcceGen, BioIVT): These players differentiate through extensive catalog diversity, 3D‑scaffold solutions, and metabolically competent liver cells — capabilities that map directly to ADME/Tox and translational research needs.

Recent corporate moves — product launches, catalog updates, trade show showcases, and certification wins — suggest suppliers are racing to secure share in high‑value application areas. Executives should interpret these developments as indicators of where competition and innovation will compress margins and accelerate standards over the next 12–18 months.

Regulatory, supply chain, and funding signals decoded

Our market dynamics section synthesizes external signals that materially affect 2026 choices:

- Regulatory emphasis on primary cell models for IND‑enabling work increases the value of validated, traceable cell banks; procurement and quality teams must demand documentation that satisfies regulators’ expectations.

- Restrictions and heightened controls on human primary cell exports in certain jurisdictions introduce potential friction for multinational trials and global supply chains; plan for alternate sourcing and compliant logistics pathways.

- Price inflation in key inputs (for example, serum) and constrained raw material availability necessitate inventory hedging and supplier partnership models that share risk through term pricing or consignment arrangements.

- Targeted public investment into organ‑on‑chip and advanced in vitro modelling expands potential demand corridors for specialized primary cells and co‑development opportunities with device makers.

- Payer and reimbursement shifts relating to primary cell–based assays in early‑phase clinical testing change the economics of preclinical validation — this should influence portfolio prioritization.

What PW Consulting’s report delivers for 2026 decision makers

Our full report is structured to be immediately useful to corporate strategists, procurement leads, R&D heads, and M&A teams. Key deliverables include actionable tools, not just descriptive analysis:

- Executive playbooks for procurement and supplier risk mitigation tailored to different organizational profiles (biotech, mid‑sized pharma, CRO, academic).

- Validated supplier scorecards and a shortlist of counterparty archetypes mapped to use‑case suitability (e.g., ADME/Tox, oncology IND packages, organ‑on‑chip integration).

- Scenario models that quantify P&L and timeline impacts under alternate reagent price, regulatory, and supply disruption scenarios.

- Go‑to‑market and partnership frameworks for suppliers and new entrants, including pricing strategies, certification roadmaps, and channel optimization guidance.

- A strategic M&A radar that identifies capability gaps most likely to be targeted by acquirers over the next 18–24 months.

These deliverables are paired with primary research — supplier interviews, procurement surveys, and conference intelligence — and a reproducible methodology for updating forecasts as new signals emerge.

How to use this insight in 2026 planning

Practical next steps for leaders planning budgets and programs in 2026:

- Incorporate a supplier concentration review into capital allocation: quantify exposure to top suppliers and set threshold triggers for diversifying or contracting with secondary providers.

- Revisit assay development timelines to reflect regulatory expectations for primary cell model validation; allocate budget to documentation and bridging studies where necessary.

- Negotiate reagent and cell supply agreements that include contingency clauses for export control changes and reagent price spikes.

- Pursue strategic collaborations with specialized cell providers to de‑risk translational milestones and accelerate time‑to‑candidate decisions.

- Monitor supplier certification activity and trade show pipelines as leading indicators of new product roadmaps and market entry timing.

Closing — the value proposition of the full study

PW Consulting’s Primary Cell Culture Market study is designed to convert market insight into immediate, fundable actions for 2026. The headline macro trajectory and concentration metrics establish the broad competitive canvas; the report’s operational modules — scorecards, scenario models, procurement playbooks, and M&A radar — translate that canvas into executable priorities. To preserve the tactical advantage and because strategic decisions hinge on fine‑grained segment and regional data, detailed breakdowns and proprietary scoring are available exclusively in the full report.

For companies making budgetary and strategic calls in 2026, the right question is not whether to engage the primary cell market — it is how to engage it with a mix of resilience, regulatory foresight, and partnership‑driven innovation. PW Consulting’s full study provides the calibrated data and decision tools to answer that question with confidence.

For detailed analysis of this topic, please visit the official page:Primary Cell Culture Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com