Combustion Control Equipment Market — Strategic Briefing for 2026: Why Executive Teams Must Recalibrate Now

As PW Consulting’s lead industry analyst, I present a distilled executive briefing from our newly published Combustion Control Equipment Market report. This briefing is designed as a strategic "trailer": it surfaces the critical dynamics, decision levers, and competitive vectors that will determine success across OEMs, integrators, utilities, and large industrial energy users in 2026 — while intentionally reserving detailed segment-level figures for our full report.

Combustion Control Equipment Market

Executive snapshot

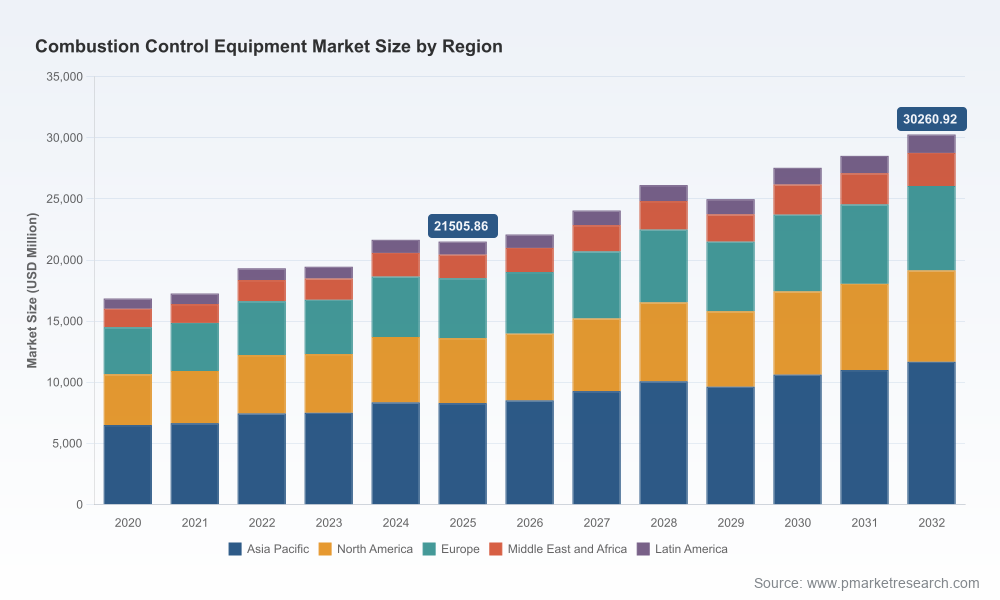

The global combustion control equipment market is at an inflection point. After a period of steady expansion through 2020–2025, the market is forecast to continue growing through 2032 at a compound annual growth rate (CAGR) of approximately 5.02%. Our base-year assessment places the market firmly in the multi‑billion USD range in 2025, and scenario planning indicates material upside for players who align product, services, and go‑to‑market strategies with tightening emissions rules, digitalization trends, and fuel‑flexibility requirements.

Combustion Control Equipment Market

Why this matters for 2026 decision cycles

- Regulatory momentum is shortening planning horizons. Compliance windows and certifications increasingly drive procurement timelines for large boilers and industrial furnaces.

- Efficiency gains are now a corporate sustainability lever. International energy authorities have set ambition levels that translate into procurement priorities for high‑efficiency combustion controls.

- Supply chain and labor cost pressures are raising the total cost of ownership (TCO) for hardware‑centric solutions, shifting value toward software, services, and integration capabilities.

Market dynamics shaping strategy

- Regulation and standards: Policy frameworks that mandate low‑NOx combustion controls for large installations and updated safety standards for furnaces and ovens have increased the baseline technical requirements for deployed systems. Compliance is not optional — it is now a core procurement filter.

- Efficiency imperatives: International targets for improved combustion efficiency are accelerating demand for advanced control algorithms, fuel‑adaptive burners, and measurable performance guarantees. Buyers are prioritizing solutions that demonstrably reduce fuel consumption per unit of output.

- Input cost and labor inflation: Component cost volatility (for example, stainless steel for sensor housings) and rising technician wages are increasing initial capex and aftermarket service costs. These pressures shorten the payback threshold for buyers and favor modular, easier‑to‑service architectures.

- Safety and certification: Advanced safety certifications (SIL 3 and equivalent) are becoming decisive in enterprise procurement, especially for large power and process applications where functional safety and uptime are mission critical.

Competitive landscape — what differentiation really looks like

The market presents a mix of global control houses, specialist burner manufacturers, and regional systems integrators. Market concentration is meaningful but far from monopolistic: the top tier holds a significant share while a long tail of specialized suppliers competes on niche performance, service, and local relationships.

Combustion Control Equipment Market

- Large automation incumbents (e.g., global process control and safety vendors) leverage integrated DCS and process‑level analytics to offer combustion control that is tightly coupled with plant‑wide optimization. These players increasingly bundle burner management, safety certifications, and lifecycle services.

- Specialist OEMs and burner makers maintain advantage through domain expertise in fuel staging, ignition systems, and burner hardware — critical where retrofit complexity or extreme duty cycles are involved.

- Regional players and integrators win on local code knowledge, aftermarket service networks, and rapid response — attributes often weighted higher than pure price by industrial buyers focused on uptime.

To illustrate the competitive set without divulging proprietary intelligence: established multinational automation and control firms provide the backbone of distributed control and safety architectures; specialist burner and valve manufacturers focus on combustion performance and hardware reliability; emerging providers differentiate through software‑driven optimization, digital twins, and predictive maintenance services.

Recent market signals — validation of themes

- Major automation players are publicly showcasing tighter integration between process control platforms and combustion control modules at global trade shows, signaling continued investment in product ecosystems that lock in enterprise customers.

- Product launches focused on enhanced boiler efficiency demonstrate supplier responses to customer TCO demands and sustainability KPIs.

- Certification updates by leading vendors underscore the premium buyers place on functional safety and compliance as part of procurement decisions.

What our report contains — practical, transaction‑ready intelligence

The PW Consulting report is built for decision makers who need to act in 2026. It moves beyond descriptive market sizing and into execution tools:

- Actionable market forecast scenarios mapped to regulatory timelines and fuel‑mix trajectories, with explicit implications for capex planning and retrofit cycles.

- Supplier evaluation frameworks and a reproducible vendor scorecard that weigh technical capability, certification status, software maturity, service reach, and balance‑sheet considerations.

- Go‑to‑market playbooks for OEMs and integrators, including partner archetypes, bundling strategies, and premium service offers that protect margins amid price pressure.

- TCO and ROI models tailored to common buyer archetypes (power generation plants, heavy process industries, and heat‑intensive manufacturing), calibrated to reflect current component cost dynamics and skilled labor inflation.

- M&A and partnership scouting intelligence highlighting where bolt‑on technologies (digital controls, advanced sensors, combustion analytics) can create defensible product differentiation.

Strategic imperatives by stakeholder

- For OEMs: Accelerate modular architectures and software‑first product roadmaps. Prioritize SIL‑certified safety modules and open APIs that enable rapid integration with plant DCS. Consider localized assembly or strategic supplier hedges to insulate against raw material volatility.

- For system integrators and service providers: Build service bundles with outcome‑based SLAs (efficiency guarantees, emissions thresholds). Invest in remote diagnostics and field technician training to capture aftermarket value as labor costs rise.

- For end‑users (utilities, process industries): Treat combustion control upgrades as strategic investments in fuel flexibility and emissions management. Use procurement to drive vendor accountability on lifecycle performance rather than acquiring lowest‑cost hardware.

- For investors and corporate development teams: Target assets that combine hardware know‑how with embedded software and recurring service revenue. Prioritize targets with strong safety certifications and proven retrofit credentials.

Risks, uncertainties, and near‑term indicators to watch

- Component price recovery or further volatility will materially affect OEM margins and buyer payback assumptions.

- Regulatory acceleration or regional rollouts of stricter emissions norms could create step‑functions in retrofit demand; conversely, delayed enforcement risks extending legacy equipment lifecycles.

- Labor market tightness for skilled combustion technicians will accelerate outsourcing and remote support models, making service networks a strategic asset.

How to use this briefing in your 2026 planning cycle

Use these insights as the executive hypothesis for budgeting, procurement, and M&A deliberations. Begin with three immediate actions:

- Stress‑test your product roadmap and procurement specifications against a regulatory acceleration scenario aligned to the latest emissions and safety standards.

- Recalibrate TCO models to incorporate current materials and labor trends; evaluate serviceing and software monetization as primary margin drivers.

- Map potential partner ecosystems (control platform vendors, sensor specialists, local service networks) and create a 12‑month integration pilot plan to de‑risk rollouts.

About the competitive entries cited

The market’s leadership includes global automation and control firms that integrate combustion management into broader process control platforms, specialist burner and valve manufacturers that underpin hardware performance in high‑duty applications, and a cohort of regional names that excel in service and compliance. Recent announcements and certifications from established vendors demonstrate the combination of product evolution and safety assurance that buyers now demand.

Next steps — get the full operational playbook

This release intentionally highlights the strategic takeaways and decision levers. The full PW Consulting Combustion Control Equipment Market report contains the granular segment forecasts, proprietary supplier scorecards, region‑by‑region demand drivers, and downloadable TCO tools that support transaction and procurement approvals in 2026. For teams preparing capital plans, vendor RFPs, or M&A diligence, the full report is mission‑critical reading.

PW Consulting stands ready to brief boards, investment committees, and executive teams on the bespoke implications for your asset base or portfolio. Contact our industry practice to schedule a confidential briefing and to access the complete dataset and decision toolkits.

For detailed analysis of this topic, please visit the official page:Combustion Control Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com