Medical-Social Working Services Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-07-02 10:44:55

As utilities, OEMs, investors and service providers prepare budgets and procurement roadmaps for 2026, PW Consulting’s latest Hydroelectric Generator Repair Market report provides a focused intelligence product designed to convert market signals into executable strategies. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study quantifies the market’s size and trajectory, maps supplier capabilities, and delivers pragmatic tools for decision-makers facing mounting pressure from aging fleets, raw-material volatility, and shifting policy incentives.

Hydroelectric Generator Repair Market

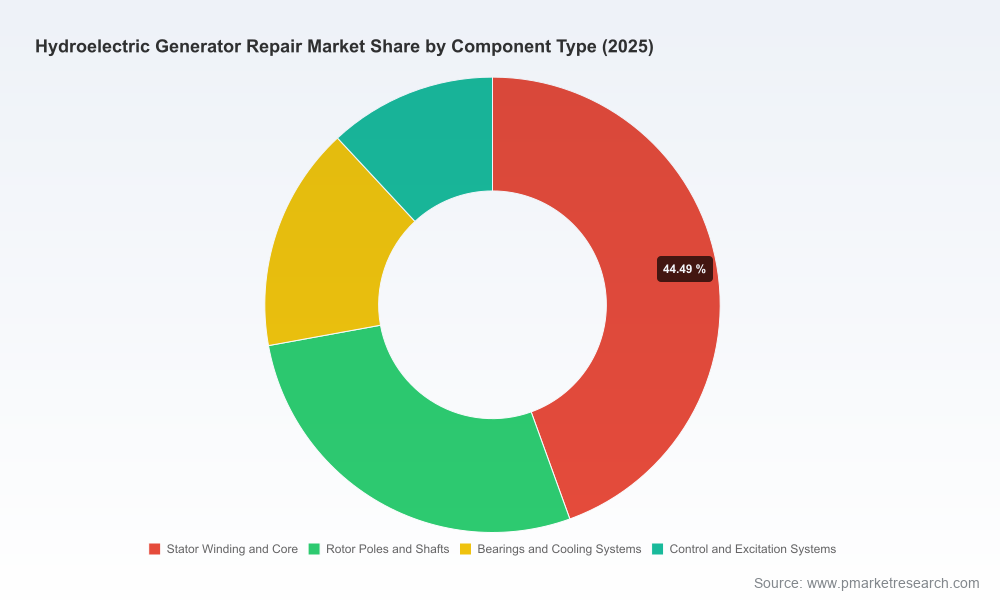

Actionable forecasting: The global hydroelectric generator repair market is estimated at roughly USD 5.12 billion in 2025 and, under our base case, is projected to grow at a compound annual growth rate (CAGR) of about 5.22% across the 2026–2032 forecast window—reaching just over USD 7.3 billion by 2032. That trajectory frames capital planning and service procurement windows for the coming strategic cycle.

Hydroelectric Generator Repair Market

Decision-focused outputs: Beyond macro forecasts, the study supplies procurement frameworks, repair-vs-replace decision matrices, risk-adjusted cost models and project prioritization tools that translate market signals into 12–36 month operational plans.

Hydroelectric Generator Repair Market

Timing and prioritization: With a large share of the global hydropower fleet reaching mid-life or older, the study identifies the optimal sequencing of refurbishment programs to maximize reliability, regulatory compliance and capacity flexibility—critical for organizations allocating 2026 capex and O&M budgets.

The repair market has shown both resilience and cyclical sensitivity. From an estimated market size near USD 3.95 billion in 2020, activity expanded into the mid-decade and reached approximately USD 5.12 billion in 2025. The growth path to 2032 is supported by continued modernization demand and renewed capital flows into hydro efficiency and grid resilience.

Several structural drivers underpin our projected 5.22% CAGR:

Aging asset base: Independent analyses indicate that nearly 40% of the global hydropower fleet is more than 40 years old. That cohort requires mid-life modernization—including turbine and generator refurbishments—to avoid performance degradation and to enable flexibility needed for variable renewable integration.

Policy and funding tailwinds: Targeted public programs (for example, incentives that have already distributed material funds for refurbishment) are accelerating owner-operator decisions to move forward with capital works during the 2024–2027 window.

Raw-material cost pressure: Key inputs—copper and steel—are subject to market tightness and price volatility. For example, copper mill shapes showed significant year-over-year producer price pressure in early 2026. These cost dynamics lengthen supplier lead times, increase repair bills and influence make-or-buy choices.

Operational modernization and digitalization: Recent overhaul projects that paired mechanical refurbishments with digitization of control systems signal a new standard—operators now expect repairs to deliver both reliability and operational intelligence.

The hydroelectric generator repair market combines global OEMs with deep technical breadth alongside specialized regional service houses and field-service specialists. This mix creates a competitive environment where incumbency, engineering depth, and rapid-response capability each deliver distinct commercial value.

Global OEM leaders (examples include established European and North American firms) bring full electromechanical solutions—rehabilitation, modernization and large-unit roll-in/roll-out capabilities backed by long-term service contracts and global spares networks. Their value proposition is integration: combining generator repairs with turbine and plant-level modernization programs.

Specialist service providers and field shops (including several long-tenured North American and Asia-Pacific firms) excel at in-situ machining, rewinds, bearing and shaft repairs, and fast mobilization. These providers often deliver superior unit economics for targeted interventions and emergency restoration work.

Mid-sized engineering firms and regional players provide a hybrid model—project management, retrofits and niche upgrades—competing on local presence, rapid mobilization, and lower total installed cost for less complex scopes.

Market concentration is moderate: while several large firms capture meaningful program-level work, much of the market remains addressable by specialist and regional providers—especially for in-situ and O&M-centric scopes. This structure creates opportunities for strategic partnerships, alliance models and selective outsourcing based on risk tolerance and schedule.

For procurement teams, the practical implication is clear: structure solicitations to evaluate both integrated OEM offers and specialist scopes-of-work, with selection criteria that weigh lifecycle costs, lead-time exposure for critical materials, and embedded digital capabilities.

Large-scale overhauls with digitization: Major utility overhauls that combine mechanical refurbishment with digital upgrades validate a growing buyer preference for “repair-plus-modernize” contracts. These projects set benchmarks for expected performance outcomes in RFPs and for contractual KPIs tied to availability and ancillary services.

Government-driven solicitations for turbine replacement and rewinds indicate an active pipeline of public-sector work with stringent procurement and compliance requirements—opportunities that favor suppliers with proven bid-to-execution capabilities.

Completed penstock and associated civil works projects reinforce the interdependence of generator repair scope and upstream hydraulic infrastructure condition—highlighting the need for integrated asset condition assessments prior to committing to generator-only interventions.

Updated federal analyses of fleet upgrades provide transparency into capacity impacts from refurbishment programs—information operators can use to prioritize projects with the highest near-term contribution to dispatchable capacity and revenue recovery.

This research product is engineered for direct operational use. Key deliverables include:

Executive dashboards translating macro forecasts into portfolio-level funding scenarios and sensitivity runs for raw-material price shocks.

Repair vs. replace decision framework with NPV-based thresholds, retrofit timelines and recommended inspection cadences by unit-age cohorts.

Procurement playbooks and RFP templates built to capture lifecycle performance guarantees, spare parts logistics clauses, and digital-commissioning milestones.

Supplier capability matrices and comparative evaluations focused on technical competencies, turnaround-time performance, and warranty structures (note: the full vendor scorecards and regional revenue splits are published in the full report to preserve commercial confidentiality and to support client-tailored licensing).

Case studies and remediation roadmaps from recent major projects—illustrating cost drivers, common failure modes, and remediation sequencing that delivered measurable availability improvements.

Risk register templates covering supply-chain lead times for copper and custom steel components, regulatory funding dependencies, and environmental compliance triggers.

For owner-operators: Treat 2026 as a decision year to convert deferred maintenance into staged modernization programs. Prioritize units delivering the greatest near-term dispatch value and those with long lead-time spares exposure.

For service providers and OEMs: Differentiate by offering bundled “repair + digital” packages with measurable performance SLAs and modular financing options to overcome capex constraints.

For procurement and project managers: Include commodity-price escalation clauses and alternative sourcing plans for copper and specialty steel in all contracts; validate supplier lead-time claims with third-party audits.

For financiers and investors: Focus on projects that unlock capacity or flexibility value within a 24–48 month horizon and where public incentives or cost-sharing de-risk performance.

For policy makers and regulators: Design incentive structures that reward outcomes (availability, flexibility, reduced emissions) rather than purely capital spend, to maximize public return on refurbishment programs.

Our methodology combines asset-level failure-mode analysis, supplier capability mapping, and an econometric treatment of commodity and policy scenarios to produce decision-ready outputs. Importantly, the full report contains the granular segmentation tables, regional and application splits, and vendor revenue share analyses that are deliberately withheld from this summary to protect commercially sensitive modeling and to facilitate licensing options tailored to client needs.

To accelerate your 2026 planning cycle, PW Consulting offers targeted briefings and bespoke scenario modeling workshops to stress-test portfolios against commodity shocks, funding windows, and competitive procurement dynamics.

Schedule a briefing with our hydropower practice to translate the report’s scenarios into a 12–24 month capital and procurement plan.

Request access to the full vendor scorecards, regional segmentation tables and the repair-cost models that underlie our forecasts (available under license).

Use our RFP templates and risk registers as a foundation for immediate 2026 tendering activity—customized versions are offered as part of our advisory packages.

In an industry defined by legacy assets, material constraints and evolving policy support, 2026 will be the year that separates reactive maintenance from strategic modernization. PW Consulting’s Hydroelectric Generator Repair Market report provides the market sizing, scenario planning and practical tools that enable leaders to convert that opportunity into measurable operational and financial performance.

For detailed analysis of this topic, please visit the official page:Hydroelectric Generator Repair Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com