Inside Bolts Market Analysis Demand Surges

Other |

2026-06-15 10:42:25

PW Consulting’s latest Aluminum Silicate Ceramic Market report (base year 2025; historical coverage 2020–2025; forecast 2026–2032) delivers a focused intelligence package designed to inform executive decision-making as the sector navigates a renewed wave of demand, regulation and supply-chain realignment. Our consolidated market model puts the global market at approximately USD 1,285.4 Million in 2025, growing at a compound annual growth rate (CAGR) of 6.12% through the 2026–2032 forecast horizon to reach the high‑single‑thousands by 2032. That trajectory reflects a blend of steady industrial end‑use consumption, accelerating high‑temperature insulation demand, and incremental adoption in advanced automotive and electronics applications.

Aluminum Silicate Ceramic Market

Regulatory acceleration: Stricter emissions and energy‑efficiency standards are increasing specification requirements for high‑temperature insulation and refractory materials. Aluminum silicate ceramic fibers and engineered products are benefiting from substitution away from heavier, less efficient alternatives.

Aluminum Silicate Ceramic Market

Raw‑material and input volatility: Synthetic mullite and related aluminum silicate chemistries depend on feedstocks such as kaolin, kyanite and bauxite. Our analysis shows price swings and availability constraints create real operating leverage for manufacturers who secure advantaged upstream positions or long‑term contracts.

Aluminum Silicate Ceramic Market

Supply‑chain and capacity moves: Recent capacity expansions and manufacturing line commissioning across leading ceramics players are re‑shaping regional supply balances and quality differentials—creating short windows for tactical market entry and customer lock‑in.

Technology convergence: The overlap between silicate ceramics and adjacent advanced ceramics (e.g., alumina, AlN substrates and multilayer substrates) drives cross‑sector demand and competition for high‑purity feedstocks and precision processing capabilities.

PW Consulting’s brief is built for leaders who must act in 2026. We combine robust quantitative modelling with pragmatic playbooks and decision frameworks, including:

Integrated market sizing and demand forecasts (2020–2032), stress‑tested in three macroeconomic and technology adoption scenarios.

Supplier and capacity mapping with plant‑level intelligence and expansion timelines; raw‑material sensitivity analysis and price‑shock simulations.

Commercial and technology benchmarking of incumbent and challenger firms, covering product portfolios, processing capabilities, IP positions and go‑to‑market strategies.

Regulatory impact matrix and adoption curves for low‑carbon binders (e.g., alkali‑activated aluminosilicates) and insulation standards that materially shift demand composition.

M&A and partnership playbook: target screening criteria, valuation heuristics and integration risk profiles tailored to producers, millers and specialty formulators.

Actionable recommendations by decision horizon—90 days (tactical procurement and hedging), 12 months (capacity and joint ventures) and 3–5 years (technology and product roadmaps).

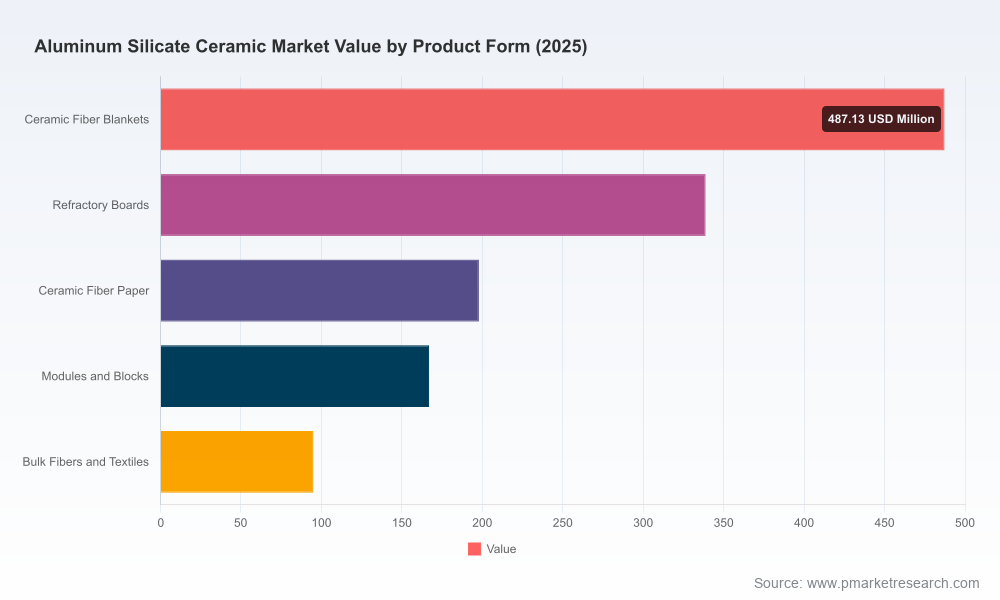

To preserve competitive confidentiality and to ensure the report functions as a decisive business tool, the public release intentionally omits granular regional, application and product split tables that are included in the full deliverable. These proprietary matrices are essential for executable commercial plans and are available exclusively via the report portal.

The market structure combines several global, technically sophisticated incumbents with regionally focused specialists. Leading firms demonstrate distinct strategic postures:

CoorsTek Inc. — A global leader in engineered technical ceramics, leveraging advanced processing and high‑purity capability to expand in both industrial and medical segments. Recent actions include commissioning a new manufacturing line to boost high‑purity alumina and related silicate outputs and securing favorable legal outcomes that protect strategic IP positions in key markets.

Saint‑Gobain Ceramics & Plastics — A major diversified producer with deep product breadth and global distribution; its portfolio supports refractory and industrial applications where lifecycle and standards compliance matter most.

Kyocera Corporation — Emphasizing high‑performance alumina and silicate components for electronics and automotive OEMs, Kyocera’s facility expansions underline the cross‑pollination between advanced electronics ceramics and traditional silicate applications.

Morgan Advanced Materials and CeramTec — Both firms combine thermal‑management expertise and product engineering to capture high‑value insulation and specialty substrate opportunities.

Regional specialists (e.g., Luyang Energy‑Saving Materials, Taisheng New Material Technology) — These producers command strong positions in regional refractory and fiber markets, benefiting from localized feedstock access and cost structures.

Smaller precision suppliers (e.g., Elan Technology, ACM, LSP Industrial Ceramics, C‑Mac, International Syalons) — Provide bespoke components, cordierite and other magnesium aluminum silicate products essential for thermal‑shock‑resistant and niche technical applications.

Market concentration is meaningful but nuanced: a handful of top firms control significant share in engineered and high‑purity segments, while a fragmented mid‑tier supplies commodity thermal insulation and refractory products—creating acquisition and partnership opportunities for both scale and capability.

Recent industry events underscore the strategic interplay between capacity and market access. For example, CoorsTek’s operational and legal developments in 2025–2026 enhance its platform for premium silicate and oxide ceramics, while announcements by electronics ceramic producers to expand AlN and related capacities have indirect implications for supply chains and cross‑sector demand for high‑grade feedstocks.

Input dynamics — Our monitoring of commodity flows in late 2025 shows short‑term price softening in certain aluminosilicate streams, driven by construction demand variability, yet feedstock tightness for synthetic mullite components (kaolin, kyanite, bauxite) remains a structural risk. Manufacturers that vertically integrate or lock in multi‑year supply agreements will benefit from predictable margins.

Substitution risk — Adoption of geopolymer binders and low‑carbon cement alternatives presents both a market opportunity and a displacement threat. PW Consulting’s analysis incorporates quantified CO2‑delta scenarios showing geopolymer binders can offer substantially lower emissions versus conventional cement systems, accelerating uptake in green construction programs.

Regulation and standards — Energy efficiency and emissions regulations are increasing the total cost of ownership premium for end customers, raising the share of applications where advanced silicate ceramics are the preferred solution.

Negotiate layered feedstock contracts with price collars and optionality to mitigate input shocks and protect margin in high‑temperature product lines.

Prioritize product development for lightweight insulation systems and modular refractory components that deliver measurable energy savings to industrial customers.

Deploy regional capacity analysis to determine where a modest greenfield or brownfield expansion delivers payback under conservative demand scenarios.

Engage in selective M&A to acquire formulation IP, kiln technology or regional market access—prioritize targets that complement core manufacturing processes and shorten the path to premium applications.

Accelerate certification and standards compliance programs to capture procurement share in regulated industries (power generation, petrochemical, iron & steel).

Invest in recycling and circularity pilots to capture cost and sustainability advantages as regulatory scrutiny intensifies.

Run scenario planning that includes both a rapid geopolymer adoption path and a sustained heavy‑industry demand path to stress capital allocation decisions.

Hedge exposure to energy and freight cost volatility through contractual instruments and network redesign.

Strengthen test‑to‑application programs with OEMs in aerospace and electronics to move into higher margin component segments.

Leverage the full commercial playbook—pricing, channel partnerships, and digitally enabled service offers (e.g., predictive thermal maintenance)—to differentiate from commodity suppliers.

Executives should treat the PW Consulting report as an operational toolkit: use the supply‑map and capacity timelines to prioritize negotiations, the cost‑curve analytics to set capital thresholds, and the regulatory matrix to synchronize product certification roadmaps with upcoming standards. For organizations evaluating M&A, the report’s target screening framework reduces diligence time and aligns valuation to operational synergies.

We intentionally present a high‑value executive summary and actionable playbooks here while reserving proprietary segmentation tables, plant‑level capacity data and client‑grade scenario outputs for the full report. These detailed datasets are what enable transaction‑grade decisions and are available through PW Consulting’s report portal.

For access to the full report, bespoke briefings, or to engage PW Consulting for a tailored market entry or acquisition study in aluminum silicate ceramics, please visit our report access page or contact our Industrial Materials practice. PW Consulting’s market models and on‑site verification protocols give you the actionable insight required to make confident, time‑sensitive decisions in 2026 and beyond.

PW Consulting — turning ceramic market complexity into executable strategy.

For detailed analysis of this topic, please visit the official page:Aluminum Silicate Ceramic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com