Effective Strategies For Online Games That You Can Use Starting Today

Games |

2026-05-07 11:03:32

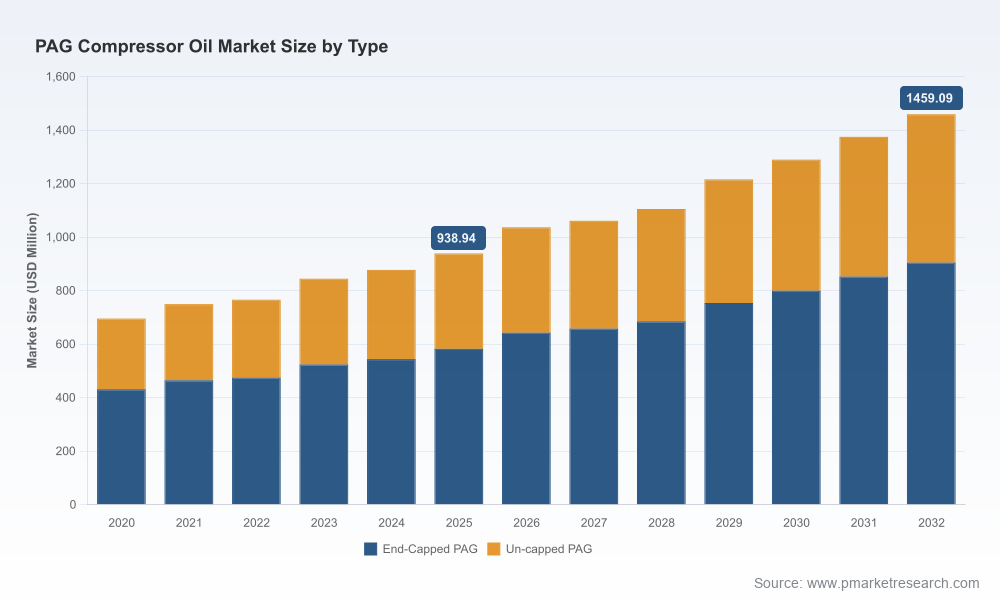

PW Consulting’s new Pag Compressor Oil Market report (base year 2025) translates five years of historical data (2020–2025) and a rigorous model into an action-oriented roadmap for corporate leaders navigating the next planning cycle. The global market, measured in USD Million, reached an estimated USD 938.94 Million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 6.51% across the 2026–2032 forecast window. By 2032 the market is modeled to approach USD 1,459.09 Million under our base-case assumptions. These headline metrics frame a sector that is neither a niche nor a commodity — it is a growth market shaped by technology transitions, regulatory pressure and concentrated supplier dynamics.

Pag Compressor Oil Market

Timing: 2026 is a pivot year for compressor oil demand patterns — OEM migration to low‑GWP refrigerants, new electric and hybrid vehicle platforms, and accelerating end‑user expectations for energy efficiency create asymmetries that will define supplier winners and losers.

Pag Compressor Oil Market

Decision leverage: Procurement, R&D and M&A teams need quantified scenarios that link raw material inflation, regulatory shift and OEM approvals to margin outcomes. Our model converts those drivers into financial exposures and opportunity buckets at company-relevant granularity.

Pag Compressor Oil Market

Execution focus: The growth trajectory (CAGR 6.51%) is attractive, but capture requires tactical moves — product qualification pipelines, inventory hedging, and targeted channel investments. The report prioritizes those levers by commercial impact and time-to-value.

The report combines macro forecasting with executable tools designed for fast operationalization by strategy and commercial teams. Key components include:

Market model (2020–2032): A transparent, spreadsheet-based model with demand drivers, sensitivity toggles for raw material cost, refrigerant-adoption curves, and regional ramp schedules. The model can be recalibrated to internal assumptions and used to stress-test pricing and margin scenarios.

Segment playbooks: Tactical playbooks for product teams covering formulation strategy (e.g., end-capped vs un-capped PAG approaches), qualification roadmaps for major OEMs, and aftermarket penetration strategies. Each playbook lists prioritized test protocols, expected lead times for approvals, and required partnership profiles.

Supplier and competitor scorecards: Multi-factor evaluation of manufacturers and base-stock suppliers across technology leadership, OEM approvals, regulatory readiness, supply security and pricing discipline. Scorecards are structured to help procurement shortlist partners for long‑term contracts.

Regulatory & technology risk matrix: Detailed mapping of EU F‑Gas Regulation, Kigali Amendment implications, and refrigerant transitions (notably the acceleration of low‑GWP refrigerants) with recommended mitigation actions and timelines for compliance-led product updates.

Raw‑material playbook: A pragmatic set of strategies addressing feedstock volatility for polyalkylene glycols (including hedging, supplier backward integration, and alternative chemistries), with example contract structures to protect margins during CPI/PPI-driven price swings.

Go-to-market and M&A guidance: Target lists and diligence frameworks for bolt-on acquisitions, partnership structures (joint development, licensing) and greenfield vs. contract-manufacturing decisions by geography.

The Pag compressor oil marketplace shows moderate concentration: the top three players account for roughly 42% market share and a top five concentration of about 58% — a dynamic that yields both stability and pockets of aggressive specialization. These structural features shape strategic options for incumbents and challengers alike.

Integrated majors (e.g., ExxonMobil, Shell, Chevron, TotalEnergies, Phillips 66): Their strength is scale and OEM relationships. They provide OEM‑approved PAG formulations across industrial and refrigeration applications and can mobilize global distribution and qualification resources rapidly. This group benefits from integrated lubricant portfolios, long-standing OEM certifications, and balance-sheet capacity to sustain inventory during feedstock shocks.

Specialists and formulators (e.g., FUCHS, Klüber, Next Lubricants, Matrix Lubricants): These players win where specification, customization and service matter most — premium formulations for electric compressors, low‑ash refrigeration variants, or small-batch qualifications for niche refrigerants. Their agility makes them preferred partners for system integrators and aftermarket channels.

Base-stock and upstream players (e.g., BASF, Cargill): Control of PAG base stocks confers decisive supply security and margin capture. BASF’s backward integration, for example, is a strategic advantage in negotiating supply contracts and guaranteeing quality for high-spec formulations.

Emerging and regional players (e.g., Oscar Lubricants, Shrieve Chemical, AMSOIL): New product launches and targeted formulations for R134a, R1234yf and EV applications indicate an environment where focused R&D and niche commercialization can rapidly establish regional footholds.

Recent moves matter: Chevron’s acquisition activity and new product introductions from niche players reveal two concurrent trends — consolidation among scale players seeking margin resilience, and product‑level innovation from specialists aiming to capture premium OEM and aftermarket pockets.

Regulatory acceleration: The combined pressure of EU F‑Gas Regulation and multinational commitments under the Kigali Amendment is compressing OEM approval cycles for low‑GWP refrigerant-compatible lubricants. Companies that have pre‑qualified formulations for newer refrigerants will enjoy faster access to OEM retrofit projects and replacement demand.

Raw material volatility and margin squeeze: Polyalkylene glycol feedstocks such as ethylene oxide and propylene oxide have shown price swings tied to CPI/PPI movements and petrochemical cycle dynamics. Our model demonstrates how even moderate feedstock inflation materially alters supplier profitability unless pass-through mechanisms or hedges are implemented.

Electrification and new compressor architectures: The rise of electric HVAC compressors and electrified vehicle platforms shifts lubricant requirements — dielectric properties, thermal stability, and low-volatility formulations become differentiators. Product roadmaps must prioritize these performance axes to secure longer-term OEM specifications.

Supply security and localization: Global supply chains remain exposed to geopolitical and logistics risk. Backward integration or diversified sourcing from base-stock producers can be competitive advantages; conversely, centralized production increases vulnerability to feedstock price shocks and shipping disruptions.

Based on our scenario analysis, PW Consulting recommends three portfolio-level moves that should be prioritized in executive 2026 plans:

Lock strategic supply for base stocks: Execute multi-year agreements with tier‑1 base-stock suppliers or secure partial backward integration. The economics of PAG production mean that securing feedstock and capacity is a direct lever on margin stability.

Accelerate low‑GWP qualification lanes: Invest in R&D and co‑development with OEMs for R1234yf and next‑generation refrigerants. Time-to-qualification will be the gating factor for access to the fastest-growing replacement and OEM segments as regulatory timelines tighten.

Pursue bolt‑on capabilities that extend value: For incumbent lubricants players, small acquisitions or partnerships that add specialty formulation expertise, testing capacity, or regional distribution can deliver outsized returns. For challengers, focus on premium niche applications (electric compressors, high-temperature gas compression) where differentiation commands pricing power.

C-suite and board agendas in 2026 should use our analysis to align capital allocation with three horizons: near-term protection (contracting and hedging), mid-term capture (product qualification and channel investments), and long-term positioning (vertical integration and strategic M&A). The report’s scenario model enables leaders to quantify trade-offs — for example, the cost of faster OEM qualification versus the benefits of earlier access to a rapidly expanding vehicle A/C replacement market.

PW Consulting’s Pag Compressor Oil Market report is built to be operationally useful: it delivers the market model, supplier scorecards, regulatory timelines and a recommended action matrix. This executive summary intentionally highlights strategic conclusions while withholding the granular split data and company-level revenue tables that buyers rely on for procurement decisions.

Accessing the full report provides the complete datasets, regional and application-level forecasts, supplier-level revenue breakdowns, and downloadable tools to plug into corporate planning processes. For procurement teams, R&D leaders, and corporate development officers preparing 2026 plans, the full analytics are essential for converting market growth into competitive advantage.

Contact PW Consulting or visit our report landing page to review the full intelligence package, licensing options for the model and bespoke advisory engagements to translate findings into a prioritized 90‑day action plan.

For detailed analysis of this topic, please visit the official page:Pag Compressor Oil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com