Full Body Checkup at Home for Women’s Health

Health |

2026-04-30 05:09:32

PW Consulting’s new market research brief on the Preeclampsia Diagnostic Market is designed as a strategic playbook for executive teams preparing decisions in 2026. Leveraging a comprehensive historical series (2020–2025) and a seven‑year forecast (2026–2032), the report synthesizes regulatory milestones, reimbursement shifts, competitive positioning, and technological trajectories into pragmatic recommendations. The message is simple but urgent: with the market expanding at a robust compound annual growth rate of 8.32%, companies that align clinical evidence generation, commercialization partnerships, and payer strategy now will command disproportionate influence as the category matures.

Preeclampsia Diagnostic Market

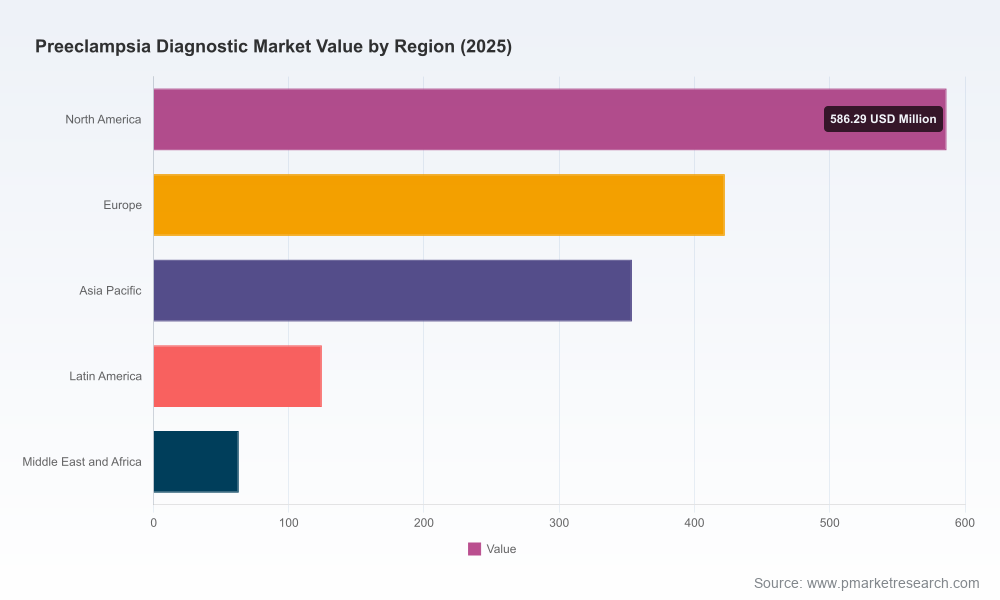

The latest model pegs the global preeclampsia diagnostics market at approximately USD 1.55 billion in 2025 and projects steady expansion across the forecast window. This growth trajectory reflects accelerating clinical adoption of biomarker‑based testing, wider platform availability in hospital and reference lab networks, and incremental reimbursement clarity in key jurisdictions. Market concentration metrics indicate a moderate level of incumbent dominance (CR3 ~42%; CR5 ~59%), which creates both stability and openings: established players can drive standardization, while agile innovators can capture niche clinical use cases and partnership opportunities.

Preeclampsia Diagnostic Market

For commercial leaders, these macro signals frame two immediate implications for 2026 planning: (1) scale still matters — investing in distribution and lab integration will compound returns — and (2) differentiated clinical evidence and go‑to‑market models remain effective levers to displace incumbents or to carve out high‑value niches.

Preeclampsia Diagnostic Market

PW Consulting’s report goes beyond headline figures. It is organized to support executable decisions and contains:

The report deliberately structures data to be directly usable by commercial, clinical, and corporate development teams while reserving the granular segmentation tables and regional allocations for licensed subscribers — a design choice intended to protect proprietary modeling while giving readers a clear path to the full intelligence set.

The competitive map in preeclampsia diagnostics straddles legacy diagnostics majors, specialized assay developers, and a cohort of translational start‑ups. Notable dynamics include:

Collectively, these dynamics produce a two‑track competitive environment: a standards layer (platform‑backed, guideline‑aligned tests) and an innovation layer (next‑generation biomarkers and prognostic panels). Companies should map their ambitions to one of the two tracks while maintaining optionality for strategic partnerships across tracks.

Regulatory endorsements have been pivotal in converting clinical promise into reimbursable practice. Recent clearances for sFlt‑1/PlGF ratio assays have acted as tipping points in certain markets by enabling standardized risk‑stratification protocols. Complementing regulation, guideline bodies in several regions now recognize PlGF‑based testing as an adjunct in suspected preterm preeclampsia, which materially affects hospital pathways.

On the reimbursement front, changes to obstetric billing (notably shifts to unbundled antepartum billing in some jurisdictions) and evolving code rules for high‑risk visits alter the economics of testing and monitoring. Clinical teams and reimbursement managers must revalidate value propositions under the new billing paradigms and prepare evidence dossiers that link diagnostics to demonstrated reductions in avoidable admissions, maternal morbidity, or length of stay.

Translating the report’s insights into a 12‑18 month action plan, PW Consulting recommends five priority moves for executive teams:

Executives planning resource allocation, R&D prioritization, or corporate development moves in 2026 need intelligence that converts epidemiology and technology trends into commercial impacts. PW Consulting’s study provides that conversion: a rigorously validated market model, scenario testing against regulatory and reimbursement inflection points, and pragmatic playbooks for evidence generation and market entry. Importantly, the report balances the need for tactical playbooks with strategic foresight — showing where consolidation is likely, where niche innovation will thrive, and how reimbursement can turn a promising assay into a sustainable revenue stream.

For organizations considering partnerships, launch sequencing, or acquisitions in 2026, the report identifies the combination of clinical evidence endpoints, channel economics, and operational investments that produce best‑case adoption timelines. Conversely, it highlights common pitfalls — underinvestment in lab integration, misread reimbursement windows, and delayed real‑world evidence generation — that erode first‑mover advantage.

To evaluate how these findings apply to your specific strategic questions — whether portfolio prioritization, commercial roll‑out design, or M&A target screening — PW Consulting offers tailored briefings that map the report’s models to company financials and go‑to‑market scenarios. The full report contains the detailed segmentation matrices, regional allocation models, and granular competitive benchmarking that underpin the strategic prescriptions summarized here.

Contact PW Consulting to schedule a strategic briefing and access the complete Preeclampsia Diagnostic Market report and accompanying scenario models. Our teams will translate the data into an actionable 2026 plan calibrated to your business objectives.

For detailed analysis of this topic, please visit the official page:Preeclampsia Diagnostic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com