Liposuction Surgery in Islamabad: Areas of the Body That Can Be Treated

Health |

2026-06-27 14:32:24

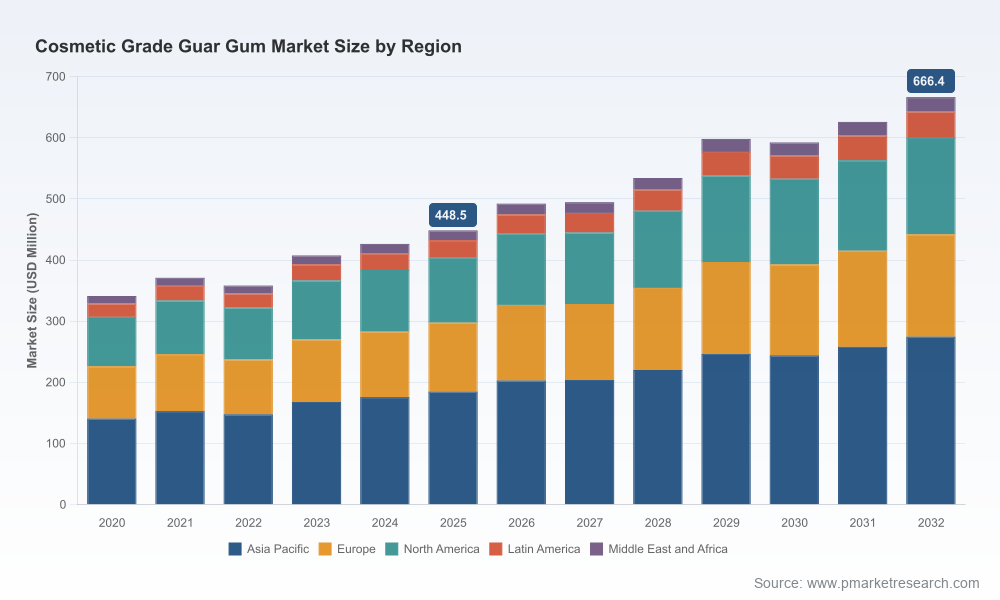

The global cosmetic grade guar gum market demonstrated resilient expansion over the 2020–2025 period, rising from a base of USD 341.2 Million in 2020 to USD 448.5 Million in 2025. Our base‑year assessment (2025) and forward modelling indicate a compound annual growth rate (CAGR) of 5.82% across the 2026–2032 forecast horizon, driving total market value toward USD 666.4 Million by 2032 under the central scenario. This growth trajectory reflects a convergence of formulation trends (clean and natural claims, texture and stability requirements), regulatory tightening around microbial purity and eco‑certification, and structural changes in supply chains and raw material pricing.

Cosmetic Grade Guar Gum Market

Timing and trajectory. Companies taking position in 2026 must calibrate investments against a market that is both maturing and expanding. Our market sizing shows steady expansion from 2020 through 2025 and an identifiable, investable growth path through 2032. That dual signal—stability plus upside—creates a narrow window to lock in supply, validate product specifications, and deploy capital for differentiation.

Cosmetic Grade Guar Gum Market

Quality, compliance and premiumisation. Cosmetic grade guar gum is no longer a simple commodity input. Regulatory frameworks and eco‑certification expectations (including ISO, GMP and COSMOS/ECOCERT compatibility) are elevating specification requirements: microbial purity, consistent rheology at low inclusion rates, and traceable sourcing are now prerequisites for entry into many premium formulations and retail channels.

Cosmetic Grade Guar Gum Market

Supply chain and origin dynamics. Production remains concentrated in traditional growing regions, but strategic moves—such as the emergence of domestic, USDA‑certified manufacturing in the United States—are reshaping supplier footprints and offering new options for nearshoring, quality assurance, and marketing provenance. Price and availability shocks in raw materials have been observed in recent cycles; buyers that implement proactive procurement and dual‑sourcing strategies will gain negotiating leverage and continuity of supply.

Competitive intensity and consolidation. The market displays a moderate concentration profile, making the behaviors of the leading suppliers materially influential on pricing, technical support, and standards setting. Competitive positioning today favors firms that pair technical service capabilities with rigorous quality systems and demonstrable sustainability credentials.

PW Consulting’s Cosmetic Grade Guar Gum Market report is designed as a practical playbook for strategic decision‑makers. It blends rigorous top‑down market sizing with bottom‑up commercial insights and is structured to answer the questions executives face in 2026:

We profile the active competitive set with an emphasis on capabilities that matter to cosmetic formulators: microbial control, consistent viscosity and rheology, eco‑certification readiness, regional supply footprints, and technical service for formulation support. Below are condensed strategic takeaways from the vendor universe.

Altrafine Gums (India) — A globally recognized manufacturer and exporter positioned on high‑purity cosmetic grades. Strengths: strict hygiene controls, emphasis on microbial purity, and an explicit focus on international compliance and eco‑certification readiness. Strategic implication: attractive partner for brands seeking certified suppliers that can support stringent quality audits and fast time‑to‑market for clean‑label products.

Supreme Gums Pvt Ltd (India) — A major producer offering cosmetic‑suitable grades with broad applications as a thickener and stabilizer. Strengths: scale and diversity of grades. Strategic implication: competitive pricing plus vertical integration opportunities for large buyers, but due diligence on microbial specs remains essential.

Sunita Hydrocolloids Pvt Ltd (SHPL, India) — Offers dedicated cosmetic grade (SUNCOS‑CG) with claimed performance benefits in foam structure and purity. Strengths: targeted product positioning for personal care formulators. Strategic implication: valuable for brands where sensory attributes (foam, feel) are priority differentiators.

Rama Gum Industries Ltd (India) — Supplier of pharmaceutical and cosmetic variants including modified hydroxypropyl grades. Strengths: regulatory pedigree and product breadth. Strategic implication: suitable for formulators requiring both functionality and compliance, particularly in medicated or cosmeceutical applications.

Guar Resources (Brownfield, Texas, USA) — The only U.S. manufacturer deriving guar from domestically grown, USDA‑certified organic beans; has publicly reaffirmed facility capabilities and sizable annual capacity. Strategic implication: nearshoring option for North American brands seeking traceability, organic claims, and reduced logistics complexity.

Hindustan Gums & Chemicals, Lucid Group, Shree Ram Industries — Established Indian players with diversified portfolios. Strengths: long production histories and multiple grade offerings. Strategic implication: stable partners for commoditised volumes—but specification gating remains a negotiation point for premium cosmetic grades.

AEP Colloids, Ampak Company Inc., Economy Polymers & Chemicals (USA) — Distributors and specialty suppliers with focus on formulation support and market access. Strengths: technical service and inventory positioning in key markets. Strategic implication: ideal channel partners for brands seeking rapid formulation guidance and shorter lead times.

Agro Gums — Bulk supplier focused on premium powder supply for personal care. Strategic implication: cost‑competitive option for high‑volume buyers who can accept longer qualification cycles.

Regulatory tightening and certification demands — Brands and manufacturers should anticipate escalating audit expectations on microbial limits and documentation for eco‑claims. Early investments in supplier audits and certificate‑of‑analysis routines will reduce time‑to‑shelf for new launches.

Raw material price and availability volatility — Feedstock cycles and mandi price movements influence producer margins and contract pricing. Scenario planning for price spikes, and contract designs that balance flexibility and security, are essential procurement actions for 2026.

Supply footprint diversification — The entry of credible domestic production in North America creates opportunities to reduce lead times and claim provenance. Conversely, over‑reliance on a single geography remains a common structural vulnerability for many buyers.

Product innovation and formulation migration — Demand for modified grades (e.g., cationic and hydroxypropyl variants) and ultra‑pure powders will continue to support premium pricing and technical service revenue streams for suppliers that can reliably deliver to spec.

We designed this report for decision‑makers who need executable intelligence, not just charts. Our deliverables include a calibrated financial model, a procurement playbook, supplier scorecards, and a prioritized action list for market entry, expansion, or consolidation strategies. The public summary above intentionally highlights core trends and strategic imperatives while reserving proprietary segmentation, granular pricing trajectories, and supplier‑level market shares for the full report.

To access the complete dataset, supplier appendices, and interactive scenario tools that underpin these conclusions, please visit our report page. The full report provides the detailed evidence base required to operationalize the strategies described here and to secure competitive advantage in the cosmetic grade guar gum market throughout 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Cosmetic Grade Guar Gum Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com