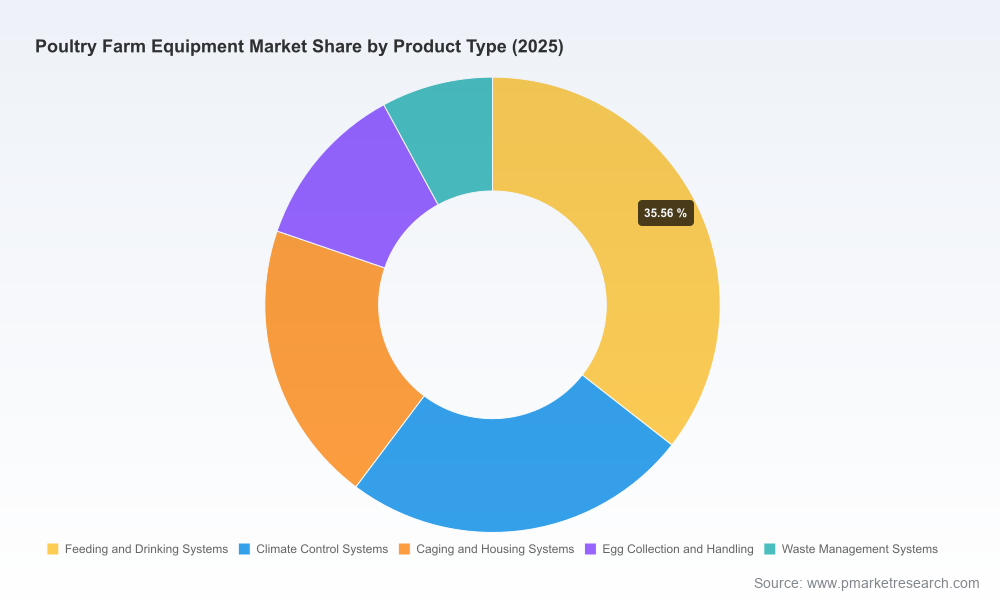

Poultry Farm Equipment Market 2026: Actionable Intelligence for Boardrooms — PW Consulting Strategic Brief

Executive Snapshot

PW Consulting’s latest Poultry Farm Equipment Market report — based on a 2025 base year and a 2026–2032 forecast horizon — translates market dynamics into a decision-grade roadmap for executives, investors, and operations leaders. The global market has expanded steadily from the low billions in 2020 to more than five billion USD (base year 2025), and our modeling points to sustained growth through 2032, with an expected compound annual growth rate of approximately 5.2% across the forecast period. By 2032 the industry is set to surpass the mid-single-digit billion USD mark, reflecting a combination of capacity expansion, automation uptake, and efficiency-driven retrofit demand.

Poultry Farm Equipment Market

Why This Report Matters for 2026 Planning Cycles

- Capital allocation clarity: Boards and CFOs require visibility into multi-year capex phasing for automation, climate control upgrades, and waste-management modernization. Our report maps investment timing to expected technology payback windows under realistic price and labor scenarios.

- M&A and partnership screening: Strategic and financial buyers can use the report’s company profiles and scorecards to accelerate target shortlisting and post-merger integration planning.

- Operational de-risking: Plant-level and regional scenarios quantify the sensitivity of returns to labor availability, raw-material cost swings, and energy price shocks — enabling hedging and supplier diversification strategies.

- Commercial strategy: Sales and product teams receive go-to-market playbooks aligned with adoption curves for IoT-enabled climate systems, automated feeding/drinking lines, and energy-efficient scalding solutions.

What the Report Contains — Practical, Executable Outputs

This is not a high-level summary; the report is a toolkit designed to be used during annual planning cycles. Key deliverables include:

Poultry Farm Equipment Market

- Multi-scenario financial models (base, upside, downside) that translate market trajectories into expected revenue, margin, and ROI implications for equipment manufacturers and integrators.

- Supplier and technology scorecards with comparable KPIs — reliability, lifecycle cost, retrofit complexity, data-integration readiness, and geographic service coverage — to streamline procurement decisions.

- Implementation playbooks for common modernization programs (e.g., retrofitting drinking/feeding lines, upgrading ventilation and climate-control systems, installing automated egg handling), complete with labor planning and estimated disruption windows.

- Regulatory and standards matrix highlighting animal-welfare, environmental, and energy-efficiency regulations likely to affect capex and O&M costs across primary markets.

- Commercial battlecards and pricing benchmarks for new product launches or tender responses, calibrated to our forecast demand curves and competitive positioning.

- An M&A diligence checklist focused on integration risk areas specific to poultry-equipment targets: parts inventory health, aftermarket contracts, IP related to automation, and field-service capability.

Competitive Landscape — Who Matters and Why

The market remains shaped by established equipment OEMs and a thriving set of regional specialists. Leading global suppliers maintain end-to-end portfolios — from feeding and drinking systems to climate control, egg handling, and manure management — while many regional manufacturers compete on price, customization, and service proximity. PW Consulting’s analysis synthesizes public filings, product roadmaps, and recent market moves to profile strategic intent across the vendor ecosystem.

Poultry Farm Equipment Market

- Large integrated OEMs: Firms with full-suite offerings continue to compete on bundled solutions (housing + automation + climate), aftermarket service networks, and international project execution capabilities. These players are actively promoting systems that reduce labor dependency and support welfare compliance.

- Automation and component specialists: Companies focused on feeding/drinking efficiency, sensor networks, and egg handling are differentiating through animal-welfare design, lower TCO, and software-enabled monitoring.

- Regional manufacturers: Local producers remain critical to cost-sensitive retrofit demand and smallholder farm segments, providing faster lead times and locally adapted designs.

Representative companies covered in the report (profiles, strategic assessments, and vendor scorecards) include long-standing global names as well as fast-growing regional players. For example, leading European and U.S. OEMs emphasize turnkey systems and incubation/hatchery specialization, while a range of Asian manufacturers focus on competitive pricing and rapid scale. Recent market activity underscores this dynamic: a global OEM showcased a new patented feeding system at a major trade show in January 2026; another large equipment business reported improved mix and synergy-driven efficiencies in late 2025; and multiple manufacturers signaled readiness for growth by investing in product modernization.

Market Dynamics Driving Strategic Choices in 2026

- Labor dynamics accelerate automation: Persistent labor shortages — and high turnover in repetitive processing roles — are catalyzing investments in sorting, sexing, catching, and handling automation. The operational case for automation is strongest where labor scarcity is chronic and wage inflation compresses margins.

- Raw-material price volatility affects margins: Fluctuating steel and component prices continue to pressure OEM margins and can shift the relative attractiveness of in-house manufacturing versus outsourced modules. Our sensitivity models quantify the break-even points for different sourcing strategies.

- IoT and smart farming converge with welfare and traceability: Adoption of sensors for temperature, ventilation, feed, and water monitoring is rising — driven by both productivity gains and regulatory/retailer demands for traceability and welfare metrics.

- Energy-efficiency becomes a procurement priority: Equipment buyers are prioritizing solutions — including redesigned scalding operations and energy-efficient steam systems — that reduce long-term energy spend and meet sustainability pledges.

Strategic Imperatives for Executives

Based on our scenario analyses and supplier benchmarking, executives should consider the following actions for 2026 planning:

- Re-sequence capex: Prioritize investments with the fastest, most certain payback (automation modules, targeted climate control upgrades). Defer large-scale housing rebuilds unless tied to immediate compliance or capacity requirements.

- Lock in critical inputs: Negotiate medium-term contracts for steel and high-value components or adopt design changes that reduce reliance on at-risk inputs.

- Strengthen aftermarket and service play: Build field-service capacity and data-enabled maintenance offerings to monetize installed base and differentiate from low-cost competitors.

- Embed digital roadmaps: Create a phased IoT adoption plan that begins with low-friction sensors and moves toward closed-loop control systems linked to farm-management software.

- Use M&A tactically: Acquire complementary automation or regional service providers to accelerate market entry and secure parts/supply chains.

Risk and Sensitivity — What Keeps CFOs Awake

Our stress-testing highlights three key risk vectors:

- Commodity-driven margin erosion: Sudden spikes in steel or electronic component costs can compress OEM margins and delay retrofit projects on the customer side.

- Regulatory shifts: New animal-welfare or environmental rules can accelerate the retirement of legacy systems, creating both disruption and opportunity depending on supplier readiness.

- Adoption lag: Where smallholder farms dominate, slower digital adoption rates may extend payback timelines for advanced systems; targeted financing and service models become critical in these contexts.

How to Use This Report in Your 2026 Playbook

PW Consulting designed this deliverable to be a working document for corporate strategy, commercial planning, and operations. Clients typically use it to:

- Set realistic top-line and EBITDA targets tied to phased equipment rollouts;

- Prioritize product development investments where the market shows accelerating demand (e.g., low-water drinking systems, closed-loop climate controls, energy-efficient processing equipment);

- Prepare buyer-seller negotiation strategies using our supplier scorecards and lifecycle-cost models;

- Design pilot projects that de-risk rollouts — and produce the operational metrics needed to move from pilot to full-scale deployment.

Next Steps and How to Access the Full Intelligence

This briefing highlights strategic takeaways and the kinds of operational tools contained in PW Consulting’s complete Poultry Farm Equipment Market report. To explore the full dataset, vendor scorecards, region- and product-level scenario outputs, and downloadable financial models — including our proprietary sensitivity analyses — visit the report landing page or contact your PW Consulting advisor. The report is structured to plug directly into 2026 budgeting and three-year strategic planning cycles, enabling decision-makers to convert market trends into measurable operational actions.

For boards and executives preparing capital plans and competitive responses in 2026, this research provides the field-proven frameworks, market-tested benchmarks, and executable playbooks needed to convert uncertainty into defensible advantage.

For detailed analysis of this topic, please visit the official page:Poultry Farm Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com