Mahadev Book - Secure Gaming Experience With Easy Login And Fast Betting

Games |

2026-05-10 14:37:29

PW Consulting's latest Ballast Bag Market report (base year 2025) provides a forward-looking, actionable framework for executives planning capital allocation, product strategy, and M&A activity in the ballast bag value chain. Our analysis finds the global ballast bag market at an estimated USD 245.5 Million in 2025 and projects steady expansion to roughly USD 381.5 Million by 2032, representing a compounded annual growth rate (CAGR) of approximately 6.5% over the 2026–2032 forecast window. These headline figures underscore a market with durable end-market drivers — recreational marine growth, industrial/marine testing demand, and safety/regulatory tailwinds — while also concealing significant variation beneath the surface that will determine winners and losers in 2026.

Ballast Bag Market

Timing is decisive: With the market on a trajectory that accelerates through the late 2020s, the decisions a firm makes in 2026 about capacity, certification, and channel partnerships will compound materially by 2030–2032.

Ballast Bag Market

Risk and resilience: Our scenario models quantify the sensitivity of manufacturer margins to raw-material cost swings, regulatory gating, and shipping bottlenecks — enabling CEOs and CFOs to prioritize hedges and CAPEX defensibly.

Ballast Bag Market

Go-to-market clarity: The competitive map in this report isolates the commercially replicable assets — proprietary materials, domestic manufacturing, certifiable load-testing capability, and aftermarket service models — that buyers are willing to pay a premium for.

Market sizing and seven-year forecasts at the market level (base year 2025) with upside/downside scenarios and sensitivity analysis tied to raw-material and regulatory assumptions.

Action-ready go-to-market playbooks for OEMs, distributors, and specialized manufacturers that translate market movement into prioritized initiatives for product development, channel expansion, and aftermarket services.

Supply-chain and sourcing blueprints that map supplier tiers for PVC, polyurethane, polypropylene, and steel shot, including multi-sourcing checklists and nearshoring decision matrices.

Regulatory impact models covering maritime load-testing standards and jurisdictional legislative changes — enabling product redesign and certification roadmaps with estimated timelines and cost buckets.

Commercial due diligence templates and valuation precedents for M&A and strategic partnerships, inclusive of integration risk scorecards and synergies that matter to acquirers in 2026.

Customer segmentation and buyer persona work, built from primary interviews and transaction-level data, that supports targeted value propositions for OEMs, rental fleets, and test-house customers.

The market trajectory — rising from USD 245.5 Million in 2025 toward USD 381.5 Million by 2032 at a ~6.5% CAGR — is driven by three persistent dynamics that firms must translate into capability investments.

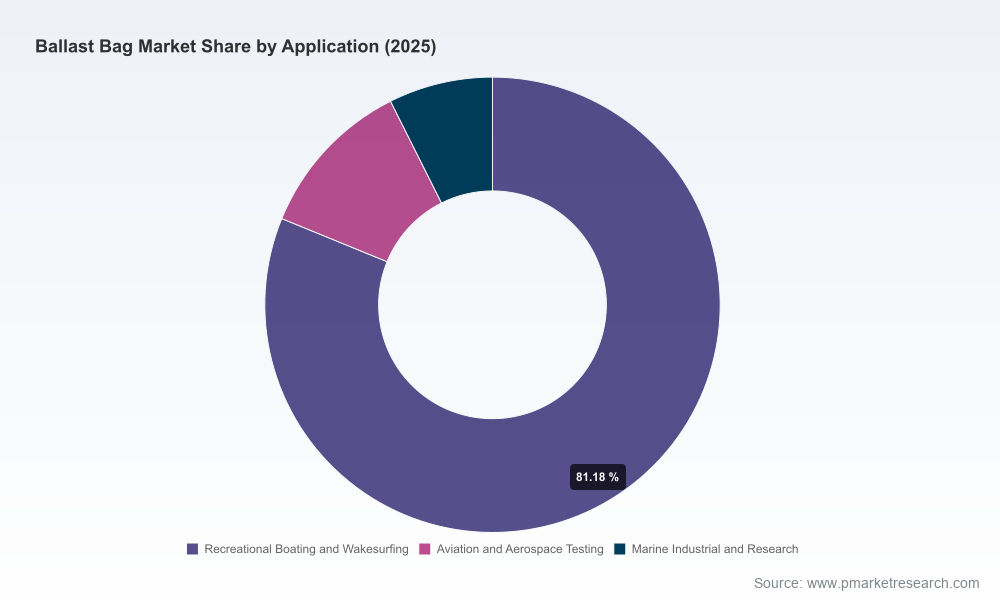

Demand diversification: Growth in recreational boating and wakesports continues to support consumer-grade water ballast systems, while parallel growth in marine and industrial testing (load testing, lifeboat and gangway certification) sustains demand for heavy-duty proof-load bags. Companies that bifurcate product lines and supply chains to serve both soft-sport and certified-industrial use cases will capture premium segments without eroding margins.

Materials and sustainability pressures: Heavy-duty PVC-coated fabrics and woven polypropylene remain the dominant construction materials for load-bearing and testing applications; steel shot and polyurethane variants serve niche performance needs. Expect increasing buyer and regulatory pressure to document recycled-content inputs and lifecycle impacts — a trend that favors manufacturers who can demonstrate validated recycled feedstocks or closed-loop recovery programs.

Regulatory and standards convergence: Compliance with industry standards (e.g., recognized proof-load and underwater testing standards) is becoming a market access requirement in many segments. Additionally, recent jurisdictional moves to regulate wake-enhancing ballast configurations illustrate how localized legislation can create compliance complexity for boat- and equipment-makers. Firms that embed certification workflows into product roadmaps will reduce time-to-market and thermalize price competition.

Our analysis shows that material selection (PVC coated fabrics, polypropylene tapes, Cordura-like deniers for fabrics, polyurethane formulations, and recycled steel shot) is a primary lever for cost, durability, and certification status. Three operational implications follow:

Vertical integration or strategic partnerships for polymer compound supply can buffer manufacturers from cyclical feedstock price swings.

Investment in fabrication and welding technologies for thermoplastic membranes directly improves warranty-backed durability and reduces field-replacement costs.

Documented recycled-content capability creates a defensible commercial differentiation and opens procurement channels with eco-conscious OEMs and fleets.

Regulatory moves at state and national levels are beginning to shape product design and advisory requirements. For example, new legislative attention to wake-enhancing equipment highlights the risk of product restrictions or retrofitting mandates that can impact aftermarket sales and OEM specifications. Separately, proof-load and underwater testing standards define minimum performance and test-reporting obligations that providers must meet to compete for industrial contracts.

Practical recommendation: establish a 12–18 month certification sprint for industrial product lines, including test-house partnerships and pre-certification pilots, to avoid losing multi-year contracts to certified incumbents.

The market remains populated by a mix of specialized manufacturers with distinct go-to-market models. Key archetypes include:

Specialist consumer-focused manufacturers who emphasize proprietary layered vinyl systems, durability, and domestic production to appeal to performance-minded recreational users.

Shot-filled and modular-weight bag producers that leverage recycled metallurgy and robust textile shells for precise ballasting solutions favored by wakesport athletes and aftermarket buyers.

Industrial-scale fabricators that supply proof-load, lifeboat, and gangway testing bags, often complying with recognized industry standards and serving shipyards and test houses.

OEM-aligned suppliers who combine custom-fit design and rapid logistics to serve boat manufacturers and specialty equipment makers.

Representative competitors profiled in the report include established US manufacturers known for durable vinyl and Cordura-style shells, California artisans focused on recycled-steel shot solutions, rapid-fulfillment players offering warranty-backed consumer products, and international fabricators that specialize in certified proof-load testing systems for maritime use. Each profile unpacks product architectures, manufacturing footprints, IP or proprietary material advantages, and channel strategies — but the report deliberately retains detailed segment-by-segment numbers for subscribers.

Prioritize certification for industrial lines. If you target marine or lifting-test buyers, allocate resources now to meet recognized proof-load and underwater testing standards; certification cycles and factory acceptance testing can take 9–18 months.

Differentiate on materials and warranties for consumer products. Invest in layered thermoplastic systems and warranty-backed durability claims to command price premiums in the recreational segment.

Secure multi-source polymer supply and consider recycled-content contracts to reduce price volatility and appeal to sustainability-conscious buyers.

Design a modular product architecture that allows cross-selling between recreational and industrial channels without significant retooling.

Identify acquisitive targets or distribution partnerships that close gaps in certification capability, logistics reach, or specialty fabrication methods — execute diligences using the report’s integration scorecards.

This report is structured as more than market intelligence; it is a playbook. PW Consulting pairs the published analysis with client workshops, a financial model kit for deal and scenario analysis, and a supplier-mapping service to operationalize supply-chain moves within 90–180 days. For executives who need a rapid decision surface for 2026, our advisory teams can deliver prioritized roadmaps and program-management resources tailored to a firm’s risk appetite and capital constraints.

The public summary above is designed to demonstrate the analytical depth and strategic rigor we apply. To preserve commercial value for subscribers, the report intentionally withholds the granular regional and application-level splits and the full segmentation matrix that clients use to create transactional playbooks. For end-to-end access to the models, proprietary segmentation, and executable templates, please visit PW Consulting’s Ballast Bag Market microsite or contact our industry team to arrange a briefing and data package tailored to your strategic priorities.

For detailed analysis of this topic, please visit the official page:Ballast Bag Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com