Low Refractive Index Resin Market: Strategic Imperatives for 2026 — PW Consulting Insights

The Low Refractive Index (Low-RI) Resin market is transitioning from niche specialty chemistries into a strategic materials arena that will shape product roadmaps across photonics, AR/VR, fiber communications, and advanced packaging. Our newest PW Consulting market research positions executive teams to make high-consequence decisions in 2026 by combining a validated macro forecast with actionable, operable intelligence. At a glance: the market surpassed the mid‑hundreds (USD Million) mark in our 2025 base year and is projected to grow at a compound annual growth rate of 8.1% through our 2026–2032 forecast window. This growth is being driven by converging demands for higher optical performance, miniaturization (including co‑packaged optics), and stringent material property control (thermal stability, low shrinkage, environmental performance).

Low Refractive Index Resin Market

Executive synopsis — why this matters now

- Optical differentiation is now a materials problem. Systems-level improvements in lasers, waveguides, and AR/VR optics increasingly depend on resin chemistries that combine a targeted refractive index with thermal and mechanical robustness.

- Time-to-market and supply assurance have become strategic levers. Raw material volatility and regulatory pressure on fluorinated chemistries are forcing procurement, R&D, and regulatory teams to synchronize decisions faster and with higher cross‑functional visibility.

- Market structure favors careful portfolio plays. The competitive landscape shows measurable concentration among a small group of incumbents, creating both ballast and opportunity for fast‑moving entrants and technology licensees.

What the PW Consulting report delivers — operationally usable intelligence

We designed this report to be a decision tool rather than a descriptive paper. Key deliverables that executives and investment committees will find immediately actionable include:

Low Refractive Index Resin Market

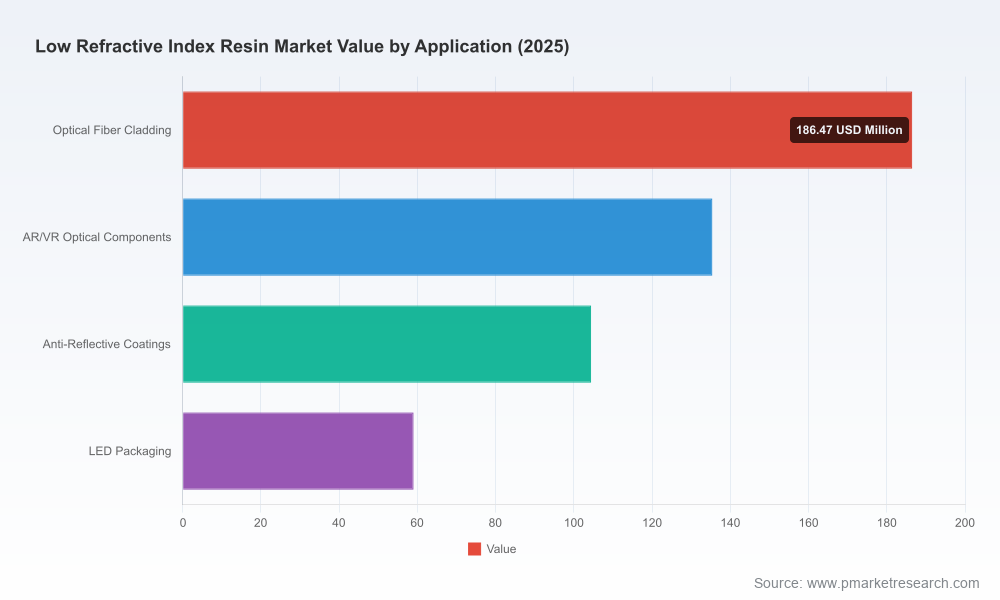

- Validated market sizing and an eight‑year forecast with scenario analysis that isolates demand by application clusters (photonic communications, AR/VR optics, anti‑reflective coatings, advanced lighting and packaging) and by resin chemistry families.

- Supply‑chain heatmaps and supplier scorecards aligned to commercial risk: availability of specialty monomers, single‑source exposure, and lead‑time sensitivity under stress scenarios.

- Regulatory impact assessment and compliance playbooks covering PFAS/fluorochemical controls, emerging regional certification requirements, and suggested product reformulation timelines to maintain market access.

- Technology & IP landscape: patent mapping, technology readiness levels for siloxane vs. fluorinated vs. acrylate chemistries, and recommendations for defensive and offensive IP actions.

- Commercial playbooks packed with go‑to‑market options—pricing frameworks for value‑based vs. cost‑plus models, co‑development contracting templates, and qualification roadmaps for OEM adoption.

- M&A and partnership screening: a prioritized list of capability gaps, integration risks and expected payback timelines for horizontal and vertical consolidation moves.

Note: this preview intentionally omits the granular regional and application split tables and company revenue shares. The full report contains the complete segmentation matrices and proprietary unit economics essential for transaction diligence.

Low Refractive Index Resin Market

Competitive dynamics — what to monitor in 2026

The Low‑RI resin space is characterized by a handful of specialist manufacturers that have combined chemistry know‑how, targeted product lines, and relationships with OEMs in photonics and advanced optics. Our research highlights several archetypes and signals to watch:

- Luvantix ADM Co., Ltd. — A technology and scale leader in UV‑curable low‑RI resins for fiber lasers and photonic modules. Strengths: portfolio breadth (including low‑RI grades with extreme thermal tolerance and low shrinkage), a multinational OEM customer base, and a compact patent estate focused on advanced manufacturing (notably two‑photon polymerization and micro GRIN optics). Recent product launches oriented to ultra‑thin micro GRIN lens arrays and zero‑shrinkage epoxies indicate a strategic push into co‑packaged optics and high‑performance packaging.

- Fospia — A fluorinated resin specialist whose product line targets fiber recoating and specialty optical fibers. The company’s emphasis on PFOA‑free formulations and silane integration places it in a defensible niche—particularly for customers requiring both chemical performance and evolving regulatory compliance.

- Inkron (Nagase Group) — Represents a siloxane‑led approach, focusing on very low indices and applications where fluorine avoidance is preferred. Inkron’s strengths are formulation flexibility for anti‑reflective and photonic device coatings, which are increasingly attractive where end‑of‑life and environmental profiling matter.

- MY Polymers, NTT‑AT, DIC — These players illustrate regional strengths and complementary capabilities: MY Polymers with global photonics market reach, NTT‑AT with precision refractive index control and high transparency offerings (though with some product discontinuations that signal portfolio trimming), and DIC with scale in UV‑curable optical films. Each is a potential partner or acquirer depending on strategic objectives.

Market concentration metrics confirm that the top tier controls a material share of revenue, but not at a level that prevents meaningful competitive entry. This implies the market is consolidating but remains contestable—an attractive dynamic for companies able to combine formulation differentiation with supply reliability.

Regulatory and raw‑material headwinds — plan for realism

- PFAS and fluoropolymer scrutiny are tangible. While some specialized fluoropolymers used in low‑RI applications are being reviewed under exemptions or are classified as low concern in certain regulatory submissions, jurisdictions are increasingly imposing substantive testing and disclosure requirements.

- Raw‑material volatility is non‑trivial. Key specialty monomers and fluorinated precursors have experienced significant year‑over‑year price swings, and lead‑time spikes are common when single suppliers face capacity constraints.

- Commercial risk from product discontinuations. The planned withdrawal of certain acrylate grades by established suppliers highlights the need for contingency planning and a proactive materials qualification pipeline.

Recommended mitigation tactics embedded in our report include supplier diversification scorecards, strategic inventory thresholds tied to reorder‑point simulations, formulation transition schedules, and a regulatory engagement calendar to preserve market access while accelerating safer alternatives.

Actionable recommendations for 2026 decision‑makers

- Prioritize applications with the fastest qualification cycle and highest material value capture—co‑packaged optics, AR/VR optics, and specialized fiber coatings—while staging investment in longer qualification plays.

- Accelerate fluorine‑alternatives R&D and pilot trials. A two‑track development program (near‑term fluorinated optimization + medium‑term siloxane/novel polymer replacement) minimizes regulatory exposure and creates commercial optionality.

- Negotiate multi‑year supply agreements with price‑indexing clauses and dual‑sourcing commitments for critical monomers; incorporate capacity reservation for pilot and ramp volumes.

- Use patent landscaping to identify white space for formulation patents and to design non‑infringing routes for proprietary performance—targeting areas like ultra‑low shrinkage, high thermal tolerance, and sub‑micron structuring compatibility.

- Embed environmental and product stewardship metrics into customer qualification packages; supply chain transparency will be a procurement gate in 2026 and beyond.

- Consider bolt‑on M&A or minority equity investments in suppliers with complementary technology—particularly siloxane specialists and firms with scalable photonics partnerships.

- Invest in qualification playbooks and collaborative pilots with tier‑1 OEMs to secure early design wins and long‑lead adoption in systems with multi‑year sourcing cycles.

How to use the full PW Consulting report

The full report is a working dossier for strategic planning cycles in 2026. It contains the granular segmentation tables, proprietary supplier scoring, unit economics by application and resin type, pricing elasticity curves, and a prioritized M&A target list with modeled synergies. If you are preparing capital budgets, negotiating long‑term supply, or defining an R&D portfolio for optical materials, the dataset and executable playbooks in the full report will materially reduce execution risk.

For compliance-sensitive projects and transaction diligence, our regulatory annex and patent‑by‑patent analysis offer the precision needed to de‑risk multi‑year investments.

Concluding perspective

Low‑RI resins are no longer a peripheral chemical sub‑segment; they are a strategic lever for optical system performance and supply‑chain differentiation. With market momentum forecast at an 8.1% CAGR across the 2026–2032 horizon and clear signs of consolidation and regulatory stress, 2026 is a pivot year. Companies that move early—securing supplies, diversifying chemistries, and locking in design wins—will enjoy asymmetric returns. PW Consulting’s report is designed to be the playbook for those moves: deep enough to build conviction, deliberately withholding proprietary micro‑split data here to protect the transactional value of the full study. Visit our official report page to access the complete analytics, models and templates required for confident 2026 decision‑making.

For detailed analysis of this topic, please visit the official page:Low Refractive Index Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com