TV Wall Mounts Market — 2026 Strategic Preview

Executive snapshot

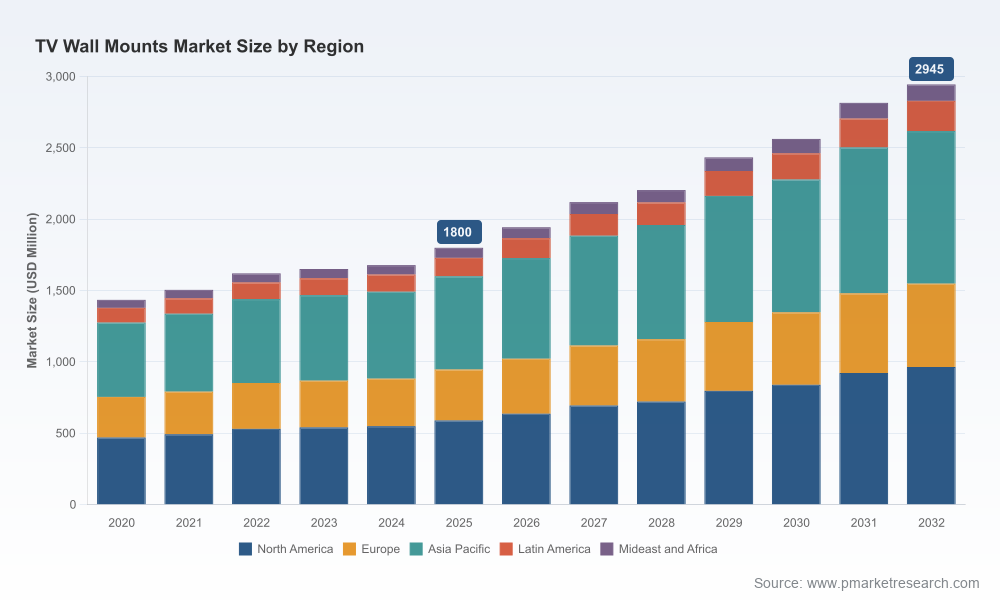

The global TV wall mounts market is entering a phase of sustained expansion as the industry transitions from hardware commoditization toward integrated value propositions that blend mechanical design, installation services and systems-level compatibility. Our base-year sizing places the market at USD 1,800 Million in 2025. Using 2020–2025 observed trends and forward-looking channel and technology adoption assumptions, PW Consulting forecasts the market to grow at a 7.3% CAGR through the 2026–2032 horizon, reaching approximately USD 2,945 Million by 2032. The market’s current structure reflects modest concentration (CR3 ≈ 38%, CR5 ≈ 45%), leaving room for both global platform players and nimble specialists to expand.

TV Wall Mounts Market

Why this research matters for 2026 decision‑makers

- Timing: 2026 is the inflection year for several secular forces — recovery in screen sales, accelerated smart‑home integrations, and new commercial AV deployments — that together create differentiated demand for mounts beyond simple hardware.

- Cost & sourcing pressure: Steel content and logistics remain material drivers of margins across SKUs. Executives who make sourcing, hedging and product‑mix choices in 1H–2H 2026 will lock in unit economics that persist for multiple product cycles.

- Regulatory & standardization levers: Ongoing updates to mounting interface standards and trade policy (notably recent Section 301 exclusions and tariff volatility) alter landed costs and should factor into supplier qualification and nearshore strategies.

- Competitive playbooks: The market rewards technically credible differentiation (large‑screen, weatherproof, or intelligent mounts) and operational excellence (installation networks, B2B channel partnerships, OEM approvals).

Market trajectory & implications

From a recovery standpoint, the market climbed from USD 1,435 Million in 2020 to USD 1,800 Million in 2025—evidence of steady demand during a period that included both supply shocks and channel re‑balancing. The forecast to USD 2,945 Million by 2032 assumes continued expansion across residential upgrades and expanding professional AV deployments in commercial and institutional segments. Importantly, growth is not uniform: price erosion in entry‑level SKUs is being offset by value capture in premium mounts for large OLED/4K displays, weatherized outdoor systems and integrated mounting + connectivity solutions targeted at installers and integrators.

TV Wall Mounts Market

Key dynamics shaping 2026 strategies

- Trade policy and landed cost volatility. Section 301 tariff dynamics have created tangible cost delta scenarios for China‑sourced components. Recent extensions to tariff exclusions have provided temporary relief, but strategic buyers must plan for tariff reinstatement risk and pricing pass‑throughs.

- Material & logistics inflation. Steel remains the dominant bill‑of‑materials input; analysts estimate it represents a substantial share of unit cost. Ocean container freight and port congestion keep landed costs structurally higher than pre‑pandemic norms, squeezing margin on low‑priced SKUs and accelerating interest in local production or component consolidation.

- Standards & interoperability. Mounting interoperability (VESA and evolving TV manufacturer specifications) is now a gating factor for OEM approval and retail listings. TV makers continue to change hole‑pattern specs and chassis profiles; this drives demand for adaptable or platform mounts that simplify compatibility.

- Product innovation & channel disruption. Wireless or non‑traditional mounting concepts debuted at CES 2026 indicate a future where hardware and software converge to reduce installation friction. Early entrants (e.g., wireless repositioning systems) create both opportunity and competitive threat to incumbent mount form factors.

- Channel complexity. Retail, ecommerce, pro‑AV integrators and OEM installers each prize different attributes (price, warranty, uptime, installability). Winning vendors will tailor assortments and service models to these channel economics rather than pursuing a one‑size‑fits‑all approach.

Operational levers — what to prioritize in 2026

- Sourcing & nearshoring scenarios: Develop dual‑sourcing plans and cost‑to‑serve models that quantify tariff exposures, lead‑time variability, and freight pass‑through at SKU granularity.

- Design for installability: Invest in mechanical simplification and modularity to reduce average installation time — a direct lever to increase installer margins and downstream willingness to pay for premium products.

- Value capture via services: Bundle installation, extended warranty and trade‑in programs to shift competition away from base price and toward recurring revenue streams.

- Margin hedging: Use material hedges and fixed‑price logistics contracts for 12–18 month horizons to stabilize gross margins during procurement cycles.

- Standards compliance & OEM engagement: Proactively certify products against evolving TV manufacturer mount profiles to gain preferred supplier status with major TV brands and systems integrators.

Competitive landscape — practical takeaways

The market blends household consumer brands, pro‑AV specialists and value‑oriented challengers. Each cluster brings a distinct strategic orientation; the right partnership or M&A target depends on whether a company wants scale, channel access, high‑margin premium positioning or rapid entry into professional AV.

TV Wall Mounts Market

- Sanus (US) — Strong in hybrid tilt/full‑motion designs and weatherproof/outdoor solutions; attractive for players seeking proven aesthetics and AV integration accessories.

- Vogel’s (Netherlands) — Premium engineering pedigree with solutions tailored for large and OLED panels; good benchmark for quality positioning and price resilience in mature retail markets.

- Peerless‑AV (US) — Deep commercial and professional AV focus; relevant for firms aiming to grow in enterprise and large‑venue deployments where service and compliance matter.

- Mount‑It! (US) — Heavy‑duty articulating brackets and XXL mounts; a playbook for capturing installs that require load‑rated products and installer‑friendly mechanics.

- OmniMount (US) — Emphasis on articulating and ceiling mounts for large 4K/UHD screens; useful for companies targeting high‑end residential and commercial display installations.

- ECHOGEAR (Canada) — Value and compatibility focus; instructive for routes‑to‑market that compete on price without sacrificing compatibility and warranty.

- Kanto (Canada) — Design‑forward full‑motion brackets; a model for combining modern aesthetics with reliable functionality to target style‑sensitive consumers.

- VideoSecu (US) — Broad SKU portfolio covering universal and heavy‑duty mounts; relevant for distributors seeking breadth and quick fill‑rates.

- AVF (UK) — Niche strength in commercial and healthcare mounts; highlights the opportunity in regulated verticals where specialized certifications and service are premium drivers.

Strategically, incumbents with strong distribution and margin frameworks are best positioned to withstand raw material and freight pressures. Meanwhile, specialized players with a clear vertical focus (hospitality, healthcare, outdoor) can extract higher unit economics despite the market’s moderate concentration.

What the full PW Consulting report delivers (practical, executional content)

Our study is intentionally structured to move from insight to action. The full report contains:

- Market sizing and topline forecasts (base year 2025, historic 2020–2025 and forecast 2026–2032), with scenario outputs for tariff reinstatement and freight‑shock events.

- Detailed segmentation by region, product type and application with modeled revenue curves and sensitivity bands — (note: segment‑level figures are reserved for the full report and client dashboards).

- Supplier scorecards, cost‑build models (including steel and logistics line items), and recommended procurement levers for margin protection.

- Channel and go‑to‑market playbooks tailored to D2C, retail, pro‑AV integrators and OEM channels, including pricing ladders and promotional elasticity tests.

- Company profiles, capability matrices and M&A target shortlists aligned to specific strategic objectives (scale, vertical specialization, or technology acquisition).

- Installation economics and service packaging templates that quantify installer take‑rates and incremental ARPU from aftercare offerings.

- Regulatory and standards tracker (including VESA updates) and an action matrix for product certification and compliance timelines.

Strategic recommendations for 2026

- Run SKU‑level landed cost scenarios now: Model 2026 procurement under both tariff relief and tariff reinstatement to determine minimum viable product pricing and identify SKUs to localize.

- Pursue modular product platforms: Invest in a small number of platform architectures that can be configured for both consumer and commercial customers to lower NPI cycle time and inventory complexity.

- Commercialize installation as a product: Pilot bundled installation + warranty offers in select markets to validate ARPU uplift and customer lifetime value improvements.

- Prioritize partnerships over ad hoc M&A for software and wireless innovations: Validate integration pathways with early adopters before capital‑intensive acquisitions.

- Benchmark against top players’ channel strategies: Use supplier and competitor scorecards to rebalance SKUs between retail, ecommerce and pro‑AV channels based on margin yield.

Closing — a guided next step

This preview is designed to surface the structural forces that will determine winners and losers in 2026. It intentionally omits the granular regional and application splits, SKU‑level pricing curves and the detailed company financials that justify tactical plays; those elements are available in the full PW Consulting TV Wall Mounts Market report and interactive datasets. If you are planning procurement, portfolio repositioning, channel expansion or M&A activity in 2026, the full study provides the executable roadmaps, scenario models and vendor shortlists you will need to act decisively.

PW Consulting’s team stands ready to translate these findings into a customized 90‑day action plan for procurement, product or corporate development leaders. Reach out to our industry desk to schedule a briefing and access the proprietary dashboard with scenario toggles for tariffs, steel and freight cost exposures.

For detailed analysis of this topic, please visit the official page:TV Wall Mounts Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com