Automated Sortation System Market — Strategic Outlook for 2026 Decision-Making

Executive preview

The automated sortation system market is maturing into a structurally important, technology-driven layer of modern logistics and distribution. Our analysis at PW Consulting shows the global market expanding from USD 356.0 million in 2020 to USD 432.0 million in 2025, with continued growth expected through the coming decade — reaching approximately USD 557.7 million by 2032 at a compound annual growth rate (CAGR) of about 3.99% over the forecast window. For executives evaluating capital allocation, platform selection, or M&A in 2026, this study crystallizes where to allocate scarce resources, how to mitigate compliance and operational risk, and which partnership models unlock fastest time-to-value.

Automated Sortation System Market

Why this research matters for 2026 decisions

- Timing of investments: The market’s steady CAGR indicates that 2026 is a pivotal year for converting pilot projects into scaled deployments without exposing operations to outsized obsolescence risk. Early movers who prioritize modularity and standardized integration reap outsized operational gains while avoiding costly forklift upgrades.

- Risk-adjusted procurement: Market concentration is meaningful — the top three vendors account for roughly 60% of market revenue and the top five approach 70%. Procurement teams must balance vendor strength and integration risk with agility and competitive pricing.

- Regulatory inflection points: Regulatory shifts (notably the EU AI Act, data privacy regimes, and evolving energy-efficiency mandates) are changing contract language, system architecture requirements, and validation processes. Systems bought without compliance foresight will face retrofit costs and slower approvals.

- Labor arbitrage and productivity: Real-world deployments show automated sortation can drive 40–60% reductions in post-sort labor requirements. That translates into new service-level possibilities — and new HR and operating models that executives must plan for in 2026.

What the full report delivers (practical, decision-grade content)

This publication is designed as a board- and C-suite-ready toolkit, not just an academic overview. Key deliverables include:

Automated Sortation System Market

- Top-down market sizing (2020–2025 historicals and 2026–2032 forecasts) with sensitivity scenarios tied to e-commerce volumes, labor cost inflation, and energy pricing.

- Vendor capability maps and competitive positioning frameworks that evaluate mechanical platforms (e.g., tilt-tray, cross-belt, shoe sorters), software stacks (WMS/WCS/edge AI), and service ecosystems.

- Implementation playbooks: phased rollout templates, sample SLAs, integration checklists for third-party robotics and vision systems, and a 12-month pilot-to-scale roadmap.

- Financial tools: CAPEX/OPEX models, 5–7 year TCO calculators, leasing vs. buy decision matrices, and NPV/IRR sensitivity analyses tailored for typical throughput profiles.

- Compliance & safety checklists: GDPR and traceability needs, EU AI Act readiness criteria, food- and pharma-grade contamination controls, and energy-efficiency benchmarking.

- Case studies and blueprints: real deployments covering healthcare, e-commerce, and retail that isolate implementation pitfalls and mitigation strategies.

Competitive landscape — what to watch in 2026

The supplier landscape combines global incumbents with specialized regional players. Leading mechanical and systems integrators continue to compete on throughput density, footprint efficiency, and ecosystem partnerships. In 2026, three dynamics will be decisive:

Automated Sortation System Market

- Modular platform differentiation: Established firms known for tilt-tray or linear sorters remain competitive on proven throughput, while innovators emphasize cross-belt and robotics-integrated approaches to handle heterogeneous parcels and returns flows.

- Software and controls as a strategic wedge: Vendors that pair sortation hardware with mature WCS/WMS integrations, deterministic control, and explainable AI will command premium renewal and services revenue.

- Partnerships and non-dilutive alliances: Expect more OEMs to pursue non-exclusive integrations with robotic pickers, vision vendors, and local integrators to broaden addressable use cases and shorten deployment windows.

Our report profiles the market’s principal suppliers — covering their core sortation technologies, typical application archetypes, global service footprint, and strategic posture. Rather than ranking by headline share alone, we map each vendor against five decision dimensions: throughput optimization, footprint efficiency, ease of integration, software maturity, and service continuity — enabling procurement and operations teams to narrow vendor shortlists aligned to specific business objectives.

Recent market moves that change 2026 playbooks

- Deployments that integrate robotic sortation into healthcare and specialty distribution demonstrate the economics of combining AS/RS and tSort-style robotic sortation for smaller, high-value parcels.

- Strategic partnerships between sortation OEMs and automation/software vendors are accelerating time-to-value and shifting buyer expectations toward bundled outcomes (not just equipment sales).

- Geopolitical and regulatory developments — including the EU AI Act becoming fully applicable — mean vendors must deliver audit-ready AI features and explainability as part of control systems, increasing procurement scrutiny on software roadmaps and compliance certifications.

Strategic implications and recommended actions for 2026

Below are prioritized actions for executives preparing decisions in 2026. Each is calibrated to deliver defensible value while keeping options open as technology and regulation evolve.

- Adopt modularity as a procurement thesis: Specify modular mechanical lanes, plug-and-play controls, and open APIs. Favor architectures that allow incremental capacity additions without major disruption to operations.

- Embed compliance in selection criteria: Require vendors to demonstrate EU AI Act compliance pathways, GDPR alignment for telemetry and traceability, and documented energy-efficiency footprints. Make compliance a gating item, not a checkbox add-on.

- Phase capacity expansions with pilot-to-scale roadmaps: Run statistically valid pilots that include software upgrades, third-party integrations, and peak-event stress tests before committing to multi-site rollouts.

- Structure commercial models around outcomes: Negotiate performance-linked SLAs (throughput and uptime), multi-year maintenance agreements with clear spare-part commitments, and options to convert from lease to purchase to hedge CAPEX risk.

- Prioritize service and spare parts footprint: In regions where vendor presence is thin, secure third-party service agreements or local integrator partnerships to avoid unplanned downtime and costly emergency logistics.

- Invest in human capital transition plans: Design workforce re-skilling programs and new operating models that capture labor productivity gains while managing transition-related service risk and labor relations.

- Use scenario-based financial modeling: Build TCO sensitivity models for at least three throughput scenarios (baseline, surge, and recession) and stress-test assumptions around energy pricing and labor replacement rates.

- Explore bolt-on M&A and partnerships: Target small robotics or software firms with proven integrable modules that accelerate time-to-market and fill capability gaps without disrupting core operations.

Decision checklist for procurement and operations teams

- Are modularity and open API support mandatory in vendor contracts?

- Does the vendor provide an AI audit trail and compliance documentation aligned to current regulation?

- Is the TCO model stress-tested for energy and labor price volatility?

- Is there a credible regional service plan and spare-parts guarantee for the expected asset life?

- Have integration partners (robotics, vision, WMS) been validated in a multi-vendor pilot?

What we intentionally reserve for the full report

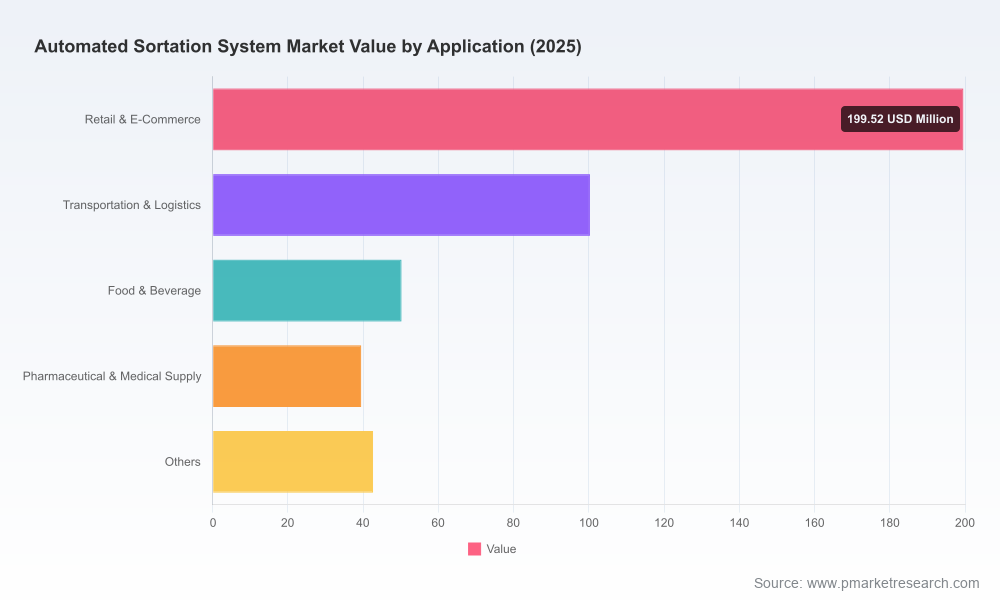

To preserve the value of our primary research and to support your precise sourcing and site-selection work, this introduction omits granular regional and application-level splits and the vendor-level revenue tables. The full PW Consulting Automated Sortation System Market report contains downloadable datasets, supplier scorecards, and interactive financial models that enable rapid vendor shortlisting, ROI calculations, and site-specific deployment planning.

Next steps

For procurement leaders, operations heads, and corporate strategists preparing 2026 budgets and roadmaps, the full report provides the evidence base and operational playbooks required to move from pilots to profitable scale. PW Consulting’s advisory teams are available to run an accelerated “sortation readiness” assessment, tailor the TCO model to your facility profile, or support RFP design and vendor negotiations.

For detailed analysis of this topic, please visit the official page:Automated Sortation System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com