Telecom Electronic Manufacturing Services Market Trends, Insights and Future Outlook

Other |

2026-03-20 06:23:02

As global semiconductor roadmaps accelerate into the next wave of compute, memory, and power architectures, silicon wafers remain the foundational substrate that shapes capital allocation, supply-chain design, and competitive dynamics across the ecosystem. PW Consulting’s latest Silicon Wafer Market study (base year 2025, forecast 2026–2032) synthesizes five years of historical performance with scenario-driven forecasts to equip executives with the decision-grade insight they need for 2026 budgeting, partnerships, and M&A. This preview surfaces the strategic takeaways without revealing the proprietary granular splits that differentiate the full report.

Silicon Wafer Market

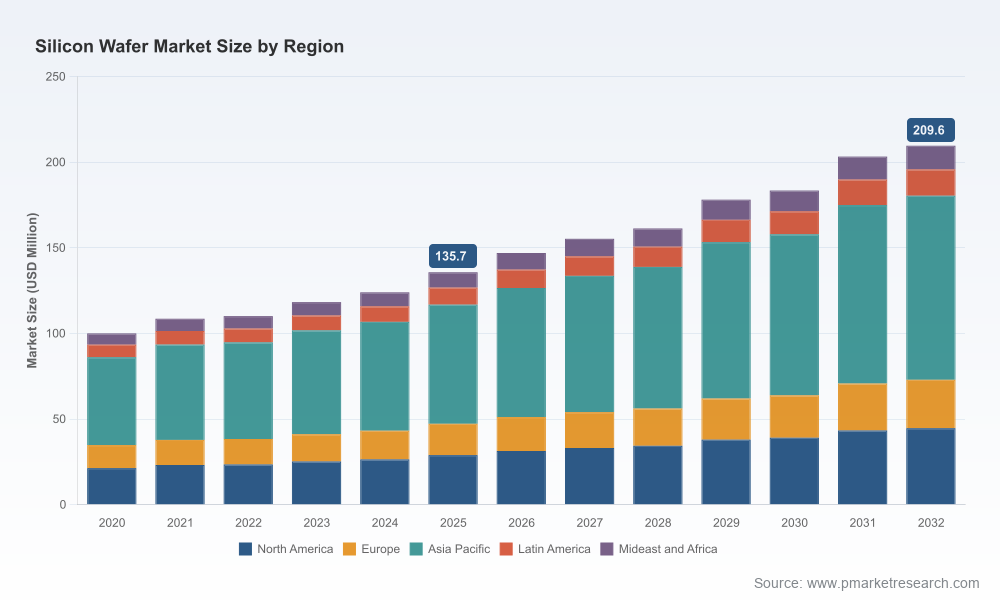

From a compact, disciplined supply base in 2020 to a more expansive and strategic market in 2025, the aggregate silicon wafer market expanded materially. Our analysis shows the market rising from an indexed baseline in 2020 to a larger and more diversified market by 2025, with continued expansion projected through 2032. Over the forecast window beginning in 2026, we model a compound annual growth rate of 6.5%, taking the market into a new structural phase where advanced epitaxial, high-bandwidth-memory (HBM)-targeted wafers, and differentiated SOI and specialty substrates increasingly command strategic attention.

Silicon Wafer Market

Why these headline numbers matter for 2026 decisions: the growth profile reflects not only cyclical demand from foundries and IDM capital investment but also secular shifts driven by AI/accelerator deployments, electrification in automotive, and the rising complexity of power devices. The scale and predictability of growth implied by the 6.5% CAGR enable more confident capital deployment — but only if firms correctly size the type and timing of investments (e.g., 300 mm epi lines vs. retrofit of 200 mm capacity) and integrate robust supply-side contingency plans.

Silicon Wafer Market

The silicon wafer market remains highly concentrated at the top. Our concentration metrics indicate that the three largest incumbents capture the majority share of global supply, while the five largest suppliers further consolidate market control. This structure creates both opportunity and risk: incumbents benefit from scale in yield optimization and customer qualifications, while new entrants and regional champions can win pockets of demand through nimble specialization and supportive industrial policy.

For corporate strategists, concentration has direct implications for competitive positioning and procurement strategy. Buyers negotiating long-term supply agreements must balance the reliability that top-tier suppliers offer with price resilience and optionality. Suppliers must weigh the economics of expanding capacity against margin pressure and the multi-year cadence of wafer qualification cycles for leading-edge customers.

The competitive map remains anchored by a set of global players that combine manufacturing breadth with customer proximity and advanced process capabilities. Key firms profiled in our study include long-standing Japanese and European incumbents, large Taiwanese suppliers with global production footprints, and regional specialists focused on MEMS, RF and power markets. Each company brings a distinct strategic posture:

Our full report contains a detailed supplier matrix that maps capabilities (diameters, epi, SOI, specialty), geopolitical exposure, and customer alignment — the operational intelligence executives need when negotiating contracts, planning dual-sourcing strategies, or evaluating acquisition targets.

The industry environment entering 2026 is marked by accelerated wafer shipments tied to AI and high-bandwidth-memory demand, continued expansion of epitaxial capacity, and strategic policy interventions. Independent shipment tallies show meaningful year-on-year increases, and several manufacturers announced new facility starts and first deliveries of advanced wafers late in 2025 and early 2026. At the same time, some planned projects have been rescheduled in response to structural market shifts, underscoring the importance of timing and flexibility in capex plans.

Policy actions — including national targets for domestic advanced wafer sourcing and public support for regional manufacturing projects — are reshaping decisions at both supplier and buyer levels. These interventions create near-term demand catalysts and longer-term localization pressures that affect where and how wafer supply is secured. For participants evaluating 2026 strategies, the interplay between private capex plans and public policy support will be a decisive factor.

Upstream constraints in semiconductor-grade polysilicon and the energy intensity of its production are recurrent themes in our scenario work. Polysilicon availability, price volatility, and the carbon-intensity profile of supply chains can materially affect wafer producers’ cost structures and their ability to meet ramp schedules — particularly for advanced epitaxial and specialty substrates. Our study models stress cases that quantify the impact of feedstock disruption on lead times, wafer pricing, and customer qualification velocity.

Designed for senior executives, supply-chain leads, and corporate development teams, the full Silicon Wafer Market study delivers actionable playbooks and tools. Highlights include:

These practical deliverables are intentionally granular and scenario-driven in the main report; this preview highlights their existence and strategic role without disclosing the calibrated inputs that underpin our recommendations.

Based on our synthesis of market growth, concentration, and supplier activity, PW Consulting recommends executives prioritize four linked imperatives this year:

For acquirers and investors, the market’s concentration profile presents both defensive and offensive M&A logics — acquiring capability breadth to shorten qualification cycles, or snapping up niche players to target high-growth subsegments. Our full valuation models and integration checklists in the report convert industry dynamics into near-term valuation implications.

Decisions taken in 2026 about capacity build-out, supplier partnerships, and product roadmaps will lock in competitive advantage for years. The market’s steady baseline growth, combined with episodic demand spikes tied to advanced compute and memory, means that timing and type of investment matter as much as magnitude. PW Consulting’s Silicon Wafer Market study brings together historical baselines, a 2026–2032 forecast anchored at a 6.5% CAGR, and a rich set of tactical playbooks so that corporate leaders can translate market signals into executable plans.

We have intentionally withheld proprietary regional and application-level splits from this summary to preserve the analytic value that is available in the full study. Senior leaders who require the detailed segmentation, supplier capability scores, downloadable datasets, and our scenario-run models can access the full report and supporting tools on our publication page.

If your 2026 planning cycle touches procurement, capacity strategy, or corporate development in the semiconductor value chain, PW Consulting’s full Silicon Wafer Market study is designed to be both the reference and the playbook you use to make those decisions. Contact our team for an executive briefing, bespoke scenario runs, or to license the underlying market model and supplier matrices that power our recommendations.

For detailed analysis of this topic, please visit the official page:Silicon Wafer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com