Polyphenylene Sulfide (PPS) Fibers Market: Strategic Briefing for 2026 Decision‑Making

Executive preview

As organisations chart growth and resilience strategies for 2026, Polyphenylene Sulfide (PPS) fibers present a textbook case of a technically mature commodity entering a phase of demand diversification and strategic repositioning. Our updated PW Consulting market study—based on a 2025 base year and tracking the industry across 2020–2025 with forecasts to 2032—shows a steady, investment‑grade expansion path. The global market, which has grown consistently over the past half‑decade, is projected to continue upward at a compound annual growth rate (CAGR) of 4.7% through 2032. By presenting consolidated baseline metrics, scenario models, supplier scorecards and tactical playbooks, the research is designed to transform macro visibility into concrete 2026 actions for suppliers, OEMs, traders and private equity actors.

Polyphenylene Sulfide Fibers Market

Why the 2026 inflection matters

- Predictable growth, shifting drivers: The PPS fibers market’s steady CAGR masks important structural shifts—moving from concentration in traditional filtration and insulation uses toward higher‑value, specialty technical textiles and composite reinforcement. This creates differentiated margin pools and new routes to premiumisation.

- Supply chain sensitivity: Raw material and energy dynamics now exercise more influence on cost curves and plant location economics than in prior cycles. Firms must recalibrate sourcing strategies and capital plans with a shorter feedback loop between input shocks and finished‑goods pricing.

- Regulatory and trade volatility: Anti‑dumping reviews, environmental tightening in feedstock production jurisdictions, and increasingly stringent sustainability procurement criteria are all creating near‑term compliance and market access decisions for 2026.

Market trajectory in one view

Between 2020 and 2025 the market recorded consistent growth, reflecting sustained industrial demand and incremental adoption in high‑temperature, filtration and insulation niches. Our base‑case forecast to 2032 applies a 4.7% CAGR, projecting continued expansion as incumbent applications consolidate and adjacent end‑markets increase penetration. This trajectory underpins a multi‑year planning horizon for capacity, R&D and commercial investment decisions rather than short‑term inventory plays.

Polyphenylene Sulfide Fibers Market

What our study delivers (actionable content)

The report is constructed as a practitioner’s toolkit. It combines robust quantitative models with scenario testing and go‑to‑market frameworks to support board‑level and operational decisions in 2026:

Polyphenylene Sulfide Fibers Market

- Validated market sizing and trend maps (2020–2025 historicals; 2026–2032 forecasts) with sensitivity testing to raw material and energy price pathways.

- Segment‑level demand drivers and adoption timelines for core and adjacent applications, together with a proprietary framework for identifying high‑margin “pull‑through” opportunities.

- Competitive benchmarking: cost‑structure decomposition, technology positioning, and commercial reach for the leading suppliers—presented as an investment‑grade competitor matrix.

- Supply chain and capex playbook: tools to model brownfield vs greenfield capacity moves, energy‑cost stress testing (including kWh/ton inputs), and sourcing optimization for feedstocks under different trade scenarios.

- Regulatory & trade risk module: scenario responses to anti‑dumping measures, product standards shifts, and feedstock environmental constraints—coupled with compliance and lobbying pathways.

- M&A and partnership screeners: overlaying synergy scores, integration risk assessments and quick‑win vs long‑term return case studies for 2026 deal pipelines.

Competitive landscape — strategic implications

The PPS fibers value chain is neither a fragmented commodity basin nor a closed oligopoly; it exhibits a mid‑range concentration where a small set of specialised firms direct technology trajectories and quality benchmarks. The top three and top five producers collectively exert meaningful influence over pricing and premium grade availability—forcing others to compete on cost, niche performance or downstream integration.

- Kureha Corporation (Tokyo): A technical leader in high‑temperature and chemical‑resistant grades. Kureha’s product depth positions it well in filtration and insulation segments that prioritize performance over price. For 2026, strategic options for Kureha include targeted licensing partnerships in Southeast Asia and expanding flame‑retardant lines for electrical insulation.

- Toray Industries, Inc. (Tokyo): Toray’s integrated textile and polymer capability, coupled with its recent Southeast Asian plant acquisition, strengthens its supply security and regional market access. Toray is strategically placed to convert manufacturing scale into faster lead times and localized product adaptation—an advantage as customers demand shorter, more reliable supply chains.

- Toyobo MC Corporation (Osaka): With proprietary trilobal geometries for dust control, Toyobo controls a performance niche in bag‑filter applications. Its offering shows how product geometry and fabric engineering can capture value beyond polymer chemistry—an important lesson for firms that lack feedstock scale but can invest in application engineering.

- Solvay S.A. (Brussels): Solvay’s Ryton® portfolio and new eco‑line introduction reflect a commercially pragmatic route into sustainability‑oriented procurement. For buyers focused on ESG credentials, Solvay’s moves underscore the premium placed on bio‑feedstock and lower‑life‑cycle‑impact fibers.

- Leading Chinese and Korean producers (e.g., Zhejiang NHU, Sino Polymer, HUVIS, Sichuan Anfeier / UNFIRE): These producers are expanding capacity and pursuing cost‑competitive export strategies. Their proximity to feedstock supply chains and competitive capex cost structures enables them to pressure commodity segments, while they gradually move into higher‑performance grades via joint ventures and technology catch‑up.

Recent industry developments and near‑term levers

Several notable corporate moves and industry shocks are shaping strategic choices for 2026:

- Capacity and footprint adjustments: Toray’s Southeast Asia plant acquisition (2025) accelerates regional supply resilience and shortens lead times—a template for firms mitigating logistics risk.

- Product innovation: Kureha’s 2025 flame‑retardant grade and Solvay’s bio‑feedstock PPS line signal divergent but complementary premiumisation strategies—one focused on electrical applications, the other on sustainability‑driven procurement.

- R&D alliances: Celanese’s co‑development tie‑up for nanocomposite PPS fibers highlights a pathway into aerospace and other ultra‑high‑value segments where material performance can command significant margin uplift.

Dynamics that should inform 2026 planning

- Feedstock volatility: In 2024 p‑dichlorobenzene prices rose by over 12% following environmental clampdowns in key producing countries—this exemplifies how upstream environmental governance can rapidly propagate to finished‑goods economics.

- Trade and policy risk: A December 2025 sunset review into anti‑dumping measures for PPS imports introduces a meaningful commercial risk for exporters and purchasers. Firms should incorporate contingency sourcing and hedging into 2026 procurement strategies.

- Energy intensity: PPS production requires substantial electrical energy (roughly 3,200 kWh per metric ton), which places producers in high‑tariff regions at an immediate cost disadvantage and makes renewable energy sourcing a decisive competitive lever.

Practical strategic recommendations for 2026

The research translates into a short list of priority moves that executives can implement within 6–18 months:

- Map supply‑chain elasticity: Stress‑test your supplier and plant network against raw‑material and energy price shocks. Prioritise access to low‑cost energy or partial on‑site generation where possible.

- Segment your portfolio: Differentiate between commodity filtration supply (volume, cost focus) and specialty fiber lines (performance, margin focus). Allocate R&D and commercial resources accordingly.

- Accelerate regional presence selectively: Where demand concentration and regulatory risk align, favour bolt‑on capacity or toll‑manufacturing partnerships over large greenfield projects to preserve capital flexibility.

- Embed regulatory scenario planning: Prepare trade‑remedy playbooks (documentation, traceability, alternate sourcing) to maintain market access during anti‑dumping reviews and related investigations.

- Pursue targeted collaborations: For entrants or mid‑sized players, technology or offtake partnerships (e.g., with established OEMs or composite integrators) can be faster routes to premium segments than commodity competition.

How PW Consulting can accelerate your 2026 agenda

Our PPS fibers study is expressly designed to convert market visibility into executable plans. Clients who deploy the accompanying Excel models and supplier scorecards can expect to reduce capital mis‑allocation risk, sharpen pricing strategies, and identify 6–12 month arbitrage opportunities between feedstock movements and finished‑goods pricing.

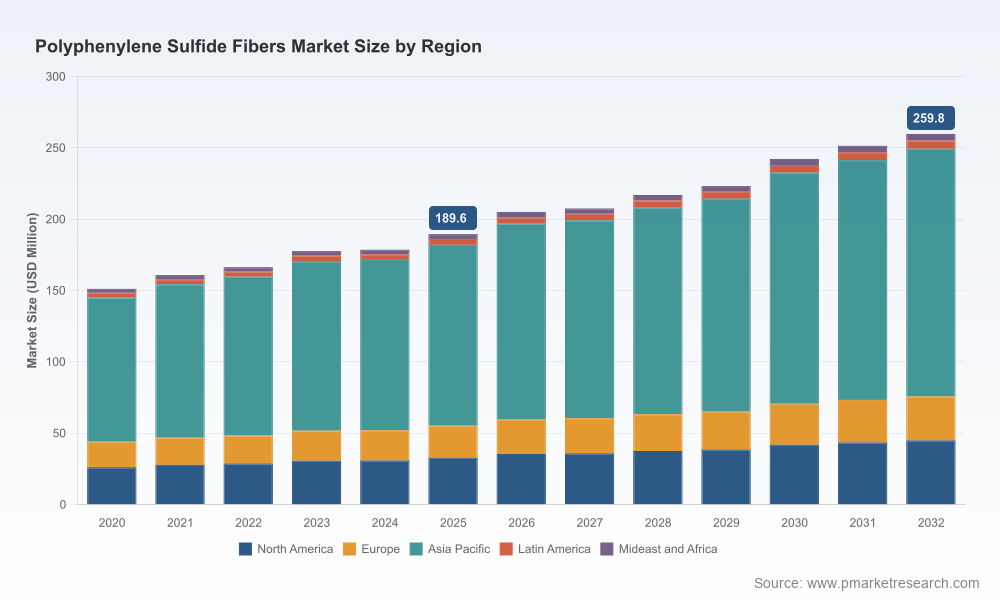

We deliberately shield detailed regional and application splits in this overview to preserve the integrity of the proprietary datasets and to encourage engagement with the full report, which contains the granular dashboards, raw data files and sensitivity simulations necessary for transaction‑grade decisions.

Closing view

For decision‑makers preparing budgets, capital plans and M&A pipelines in 2026, PPS fibers offer a mix of defensive and offensive plays: defensive measures to manage feedstock, energy and trade risks; offensive investments into property‑righted fiber geometries, eco‑feeds and composite integrations. The market’s steady growth provides a reliable backbone for these strategies—but winning will depend on aligning technical differentiation with nimble supply‑chain and regulatory responses. Our full study supplies the data, models and playbooks to make those tradeoffs with confidence.

For detailed analysis of this topic, please visit the official page:Polyphenylene Sulfide Fibers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com