Organic Pea Protein Market: Rising Demand for Clean-Label and Sustainable Protein Sources

Networking |

2026-06-16 10:18:52

Between cyclical end‑markets and structural energy transitions, the industrial gases sector sits at a strategic inflection point as companies plan 2026 budgets and multi‑year capital programs. PW Consulting’s forthcoming Industrial Gases Market study synthesizes five years of historical performance (2020–2025), a 2025 base year benchmarking, and a forward‑looking forecast (2026–2032) underpinned by a 6.5% compound annual growth rate (CAGR). This briefing highlights the research’s strategic value for C‑suite and deal teams preparing commitments in 2026 — while deliberately withholding the full set of segment granularity to preserve the commercial value of the complete report.

Industrial Gases Market

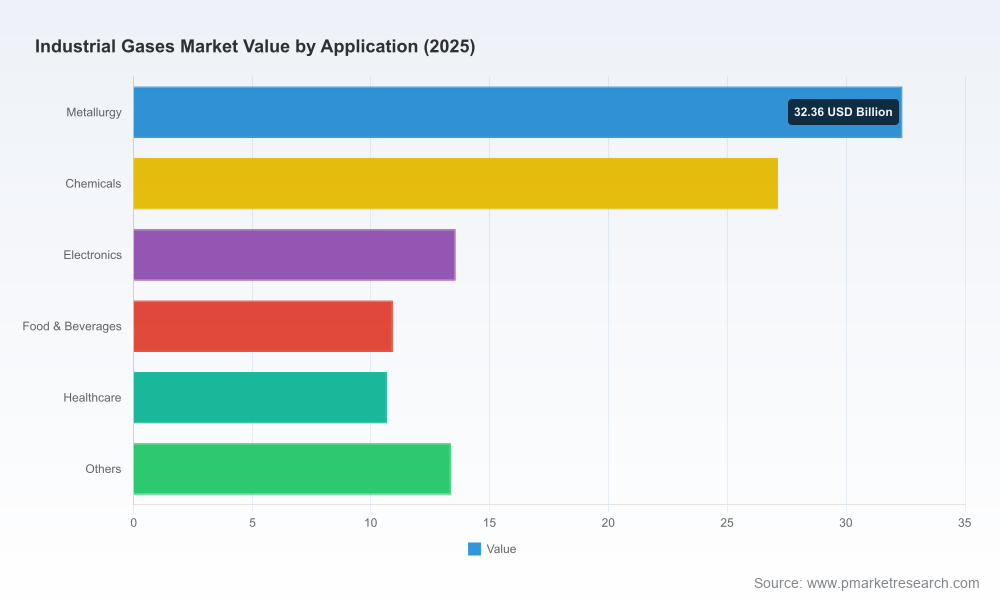

Our topline modelling shows the global industrial gases market expanding from approximately USD 80.5 billion in 2020 to USD 108.0 billion in 2025 (base year), and continuing along a healthy growth path through the forecast period. Under our central case the market reaches the mid‑hundreds by the early 2030s, reflecting broad demand in heavy industry, chemicals, electronics manufacturing, food & beverage, healthcare, and emerging clean‑energy deployments. The 6.5% CAGR embedded in our scenarios captures both steady organic consumption growth and incremental volumes tied to decarbonization and semiconductor capex cycles.

Industrial Gases Market

Capitalization and phasing: 2026 is the year many corporations finalize multi‑year CAPEX commitments for air separation units, electrolysis capacity, and cryogenic logistics. Our study provides cost‑to‑serve and phased investment schedules that help CFOs optimize timing and financing structures.

Industrial Gases Market

Contract strategy: With semiconductor and energy customers increasingly favoring long‑term supply agreements and on‑site solutions, procurement and commercial leaders need playbooks for offtake negotiation, risk allocation, and indexation clauses. The report translates market dynamics into negotiable contract archetypes.

Decarbonization prioritization: Hydrogen and low‑carbon oxygen production are high‑priority spend areas. We quantify project IRRs under alternate electricity price trajectories and provide decision rules for piloting electrolyzer capacity versus purchasing low‑carbon gases.

M&A and portfolio decisions: Given moderate market concentration among leading providers, growth through bolt‑on acquisitions and selective greenfield investments remains attractive. Our competitive benchmarking and target screening shorten due diligence timelines for 2026 deal teams.

The market’s operational and commercial environment is being reshaped by a combination of cost factors, regulation and customer concentration:

Raw materials and feedstock: Natural gas continues to serve as a primary feedstock for many production pathways (including air separation and reforming processes), creating direct exposure to gas price volatility. Procurement and hedging strategies therefore materially affect unit economics.

Energy intensity: Cryogenic air separation and large‑scale electrolyzers are electricity‑intensive. Electricity price fluctuations translate rapidly to margin compression or expansion, making power procurement arrangements and site selection (including access to renewables) critical levers.

Labor and operations: Post‑inflationary wage normalization and higher energy costs have compressed reported margins in recent periods. Headcount and productivity assumptions now factor into most operational plans; our plant‑level benchmarking allows managers to stress‑test staffing, automation and outsourcing options.

Regulatory and market access: Stringent purity and safety standards (e.g., in healthcare and electronics) impose capital and quality‑assurance requirements that raise the bar for new entrants. Additionally, European carbon mechanisms (including CBAM and EU ETS) are altering cross‑border cost competitiveness and have measurable implications for outsourced hydrogen sales and related allowances.

The industrial gases industry remains consolidated at the top: the three largest global players collectively account for a material majority of market share, and the top five increase concentration further. This structure creates both stability and competitive friction in procurement, pricing and asset roll‑outs.

Major incumbents — including Air Liquide, Air Products and Chemicals, Linde, Messer, Matheson Tri‑Gas, Nippon Sanso, BASF and Iwatani — are pursuing differentiated strategies across supply agreements, asset expansion, and low‑carbon innovation. Recent selective developments illustrate these strategic trajectories:

Supply agreements with semiconductor manufacturers are accelerating. In 2025 several leading gas providers signed long‑term contracts and announced capacity commitments to support new semiconductor fabs — a trend that intensifies offtake competition and favors vertically integrated solutions.

Decarbonization projects are moving from pilots to scale. Large electrolysis investments and integrated low‑carbon hydrogen initiatives led by prominent providers reflect a shift to capex‑heavy, long‑duration projects — requiring new financing approaches and partnership models with energy incumbents.

Selective capacity expansions continue at the regional level to support logistics and just‑in‑time manufacturing needs. These expansions are being balanced against disciplined capital allocation as firms weigh long‑term demand uncertainty post‑2026.

For procurement and strategy teams this concentration profile implies two practical realities for 2026: (1) a limited but high‑impact set of counterparty choices, and (2) intensified pricing dynamics around specialty gases, semiconductor grade supplies, and low‑carbon products.

Our full report is structured to support immediate decision‑making across commercial, operations and M&A functions. Key deliverables include:

Top‑down market model (2020–2032) with base‑case, downside and upside scenarios that reflect demand shocks, energy cost paths and policy interventions.

Plant‑level cost models and power sensitivity analyses for ASUs and electrolyzers — calibrated to regional power and feedstock curves.

Commercial playbooks: template long‑term supply agreements, indexation clauses, and offtake negotiation checklists tailored for semiconductor, steel and chemicals customers.

Competitive scorecards: strategic positioning, capacity footprint, recent deal activity and likely next moves for each major producer.

Decarbonization business cases: techno‑economic analysis of hydrogen pathways, break‑even power prices, and suggested financing constructs.

M&A and JV screening: prioritized target list, valuation ranges and integration risk maps for bolt‑on acquisition strategies.

Regulatory compliance matrix: jurisdictional purity, safety and carbon reporting requirements accompanied by implementation timelines.

Commercial sensitivity dashboards and executive one‑pagers for board and investor communication.

Note: In keeping with the “trailer” approach, we do not disclose detailed regional/application splits or embedded segment revenue tables here. The full report includes granular sub‑segment data, interactive models and downloadable datasets that power negotiation and financial modelling exercises.

Execute stress‑tested CAPEX phasing: adopt a two‑stage investment approach for new ASUs/electrolyzers that allows option value capture if electricity or feedstock prices escalate.

Lock strategic offtakes with flexible indexation: negotiate long‑term offtakes with embedded flexibility for purity tiers and volume ramps tied to customer fab schedules.

Prioritize grid‑adjacent, renewable‑sourced locations: secure power purchase agreements early for low‑carbon projects to protect project IRRs against volatile market prices.

Use competitive concentration to your advantage: engage top suppliers with bilateral pilots and capacity reservation clauses to de‑risk supply for critical processes.

Build a regulatory forward‑view: incorporate CBAM/EU ETS trajectories into cross‑border pricing and trading strategies, and quantify allowance exposure in 2026 budgeting.

Prepare for partnership finance models: consider project JVs and green bonds for CAPEX‑heavy decarbonization projects to preserve corporate balance sheet flexibility.

The study combines bottom‑up asset surveys, proprietary demand models, company disclosures and market intelligence gathered through 2025. Base‑year calibration uses audited company reports and validated supply agreements; scenario analysis spans 2026–2032 with explicit stress paths for energy, feedstock and policy variables. We applied conservative assumptions where public data diverged and documented sensitivities to support robust decision‑making.

PW Consulting recommends three immediate steps for leadership teams preparing 2026 decisions:

Commission a 48‑hour stress test using your existing project pipeline against our power/feedstock scenarios to identify weak links in planned roll‑outs.

Run an offtake negotiation mock with our commercial playbook to surface clauses that preserve optionality while securing necessary volumes.

Schedule a strategic briefing with our industry team to review the full dataset and interactive models — the granular segment and regional outputs are included only in the complete report to preserve client value.

In a market where supply agreements, decarbonization capital and semiconductor demand converge, the right intelligence — and the timing of decisions — will determine winners and laggards in 2026 and beyond. PW Consulting’s Industrial Gases Market study delivers the structured analysis needed to make those calls with confidence.

For detailed analysis of this topic, please visit the official page:Industrial Gases Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com