Yellow Peeling in Dubai for Deep Skin Renewal and Natural Glow Enhancement

Health |

2026-05-14 08:01:41

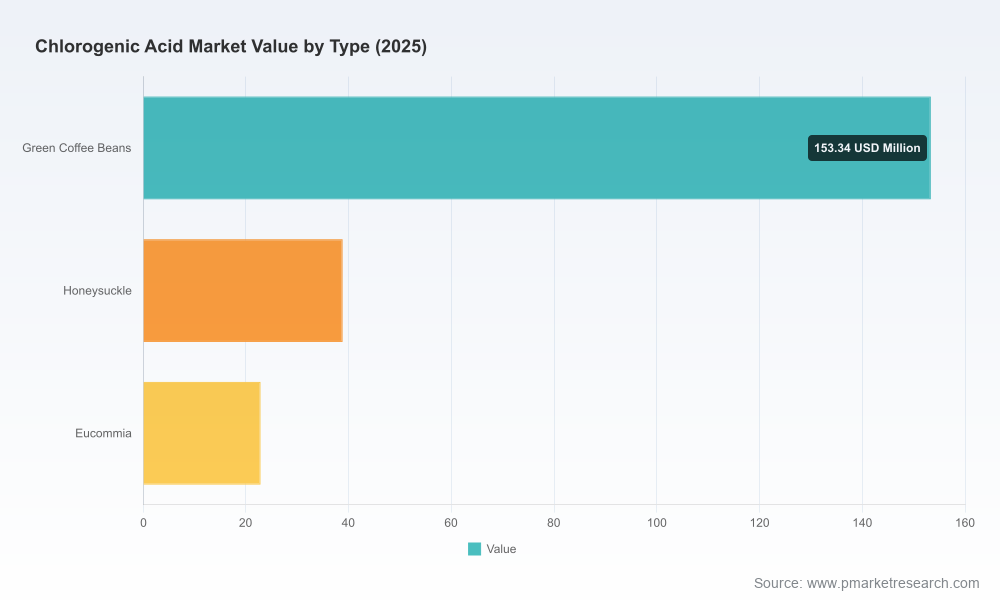

The chlorogenic acid (CGA) market is maturing from a niche botanical extract into a commercially significant ingredient across nutraceuticals, functional foods & beverages, cosmetics and select pharmaceutical applications. Our research baseline (base year 2025) shows the market has expanded from approximately USD 163 million in 2020 to about USD 215 million in 2025, and is projected to continue growing through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of roughly 5.7%, reaching an anticipated market size in excess of USD 315 million by 2032. These headline dynamics frame a medium-growth industry with clear pockets of margin expansion tied to product standardization, regulatory clarity and supply-chain optimization.

Chlorogenic Acid Market

This preview is designed to articulate why the full PW Consulting Chlorogenic Acid Market study is strategically relevant to corporate decision-making in 2026. We highlight the decision levers—sourcing, product development, regulatory strategy, pricing and inorganic growth—and map the evidence base that supports them. True to the “trailer” principle, we demonstrate methodological rigor and practical insight while withholding proprietary sub-segmentation detail to encourage engagement with the full report.

Chlorogenic Acid Market

The top-line trajectory—steady mid-single-digit CAGR through 2032—signals two important strategic realities. First, demand is predictable enough to support multi-year investments in processing and quality systems, but not so explosive that scale alone guarantees outsized returns. Second, incremental gains in purity, clinical validation and traceability can justify meaningful price premia, creating asymmetric opportunities for firms that invest selectively in differentiation rather than pure volume play.

Chlorogenic Acid Market

For 2026 planners, this means prioritizing capital allocation toward modular capacity expansions, long-term supplier contracts with built-in quality KPIs, and differentiated product pipelines (clinical claims, high-purity APIs, beverage-ready concentrates) rather than large, undifferentiated greenfield plants. The forecast horizon provides a runway for staged commitments—early mover premiums can be captured by signaling traceability and clinical backing, while preserving optionality for demand-side volatility.

The competitive field blends established specialty ingredient houses, vertically integrated botanical suppliers, and high-volume producers based in Asia. Key strategic archetypes emerge:

Representative companies illustrate these archetypes. Some European and North American firms emphasize standardized green coffee extracts with traceability and application support for nutraceuticals, beverages and cosmetics. Several established US-based players have built branded extracts aimed at metabolic health. Spain-based and specialist producers supply higher-purity botanical extracts and clinical-grade material. China-based manufacturers provide scale and competitive pricing, with several suppliers reporting broad export footprints. A growing number of India-based players focus on herbal APIs and formulations for both domestic and export markets.

Recent industry actions crystallize strategic directions. There have been capacity expansions in key raw-material sourcing regions to tighten traceability and supply security, and new product launches that push for higher CGA concentrations compatible with beverage and flavor systems. These moves reflect a two-track strategy: secure upstream sourcing while layering product innovation downstream.

This executive preview is a directional roadmap. The full PW Consulting Chlorogenic Acid Market report provides the granular intelligence that decision makers need to operationalize the recommendations above: supplier scorecards, jurisdiction-specific regulatory tables, price elasticity matrices, and proprietary segmentation that identifies the highest-value end-market pockets. For commercial negotiations, procurement optimization, and M&A diligence in 2026, that granularity materially alters outcome probabilities.

If your 2026 plans include capacity investments, strategic supplier consolidation, product launches with clinical claims, or cross-border acquisitions, the full report will deliver the actionable datasets and scenario workbooks to quantify trade-offs and to defend capital requests internally. We have prepared templated negotiation playbooks and a set of investment case models that align with the market scenarios described here.

The chlorogenic acid market sits at an inflection where predictable mid-single-digit growth meets opportunity for differentiation. Companies that combine supply security, regulatory foresight and product-led premiumization can capture disproportionate value despite the market’s measured overall growth rate. For 2026, the imperative is clear: convert headline stability into competitive advantage through targeted investments in traceability, clinical evidence and flexible commercial models. The full PW Consulting study provides the detailed maps and tools to make those investments defensible to boards and investors.

To access the complete dataset, supplier rankings, regulatory matrix and scenario workbooks that underpin these conclusions, please consult the full report on our site. The preview above frames the strategic choices; the full study equips you to act on them.

For detailed analysis of this topic, please visit the official page:Chlorogenic Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com