Medical Weight Loss Millsboro at AlphaCare Medical

Health |

2026-05-20 07:27:35

The PCR for Respiratory Infection Diagnostic Market landscape of molecular diagnostics in the United States is experiencing a period of unprecedented growth, particularly within the realm of infectious disease management. As clinical laboratories and healthcare providers seek more precise ways to manage seasonal and chronic conditions, the US has emerged as the primary force in the sector. Leveraging a combination of rapid technological adoption and high healthcare expenditure, the country continues to lead the way in setting diagnostic standards.

This dominance is not merely a result of historical infrastructure but is driven by a proactive shift toward decentralized testing. From large-scale hospital laboratories to local urgent care centers, the integration of Polymerase Chain Reaction technology has become a non-negotiable standard for accuracy. This transition ensures that the US remains at the forefront of the global diagnostic arena, providing a blueprint for high-efficiency molecular workflows.

Download Sample Report - https://www.theinsightpartners.com/sample/TIPRE00023326

Strategic Market Valuation and Projections

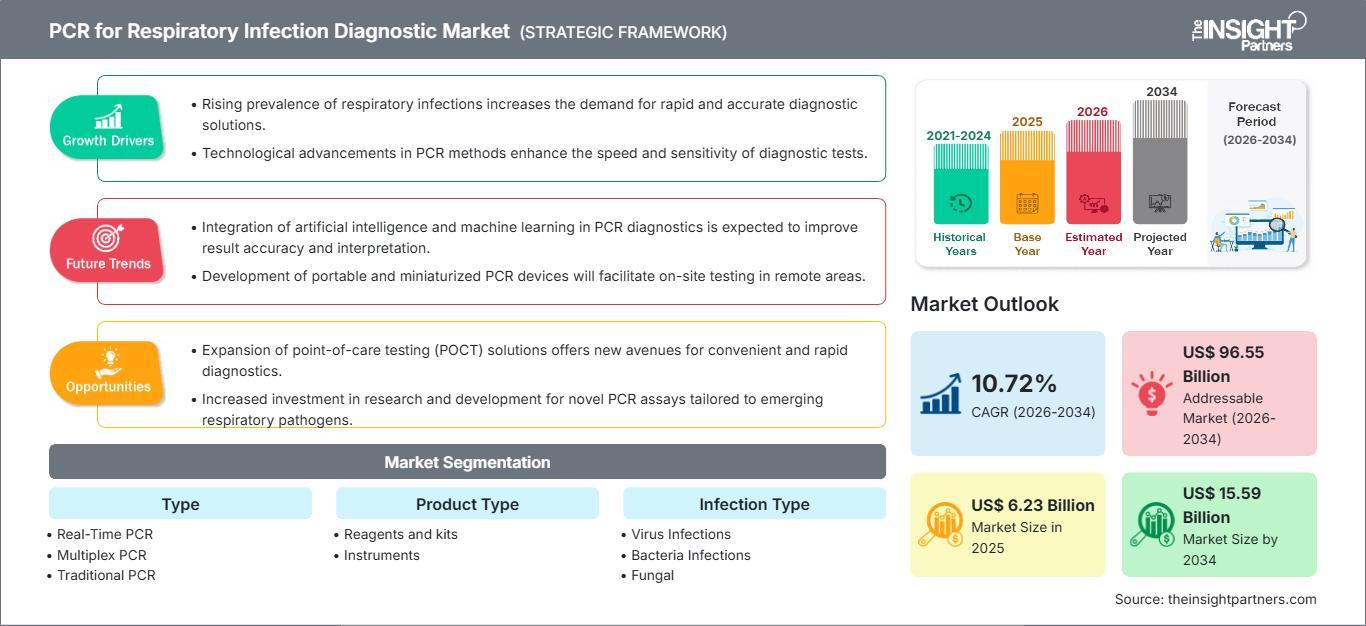

The size is expected to reach US$ 15.59 billion by 2034 from US$ 6.23 billion in 2025. This market is anticipated to register a CAGR of 10.72% during the forecast period of 2026 to 2034. Within this timeframe, the United States is projected to maintain its position as the largest regional stakeholder, fueled by a relentless drive for innovation and a stable reimbursement environment for molecular pathology.

Key Market Drivers for US Dominance

One of the most powerful drivers within the US market is the aggressive implementation of multiplex syndromic panels. US healthcare providers are increasingly moving away from "one-off" testing in favor of comprehensive respiratory panels that can identify multiple viral and bacterial pathogens in a single run. This shift is particularly critical during the "tripledemic" threats of COVID 19, Flu, and RSV, where rapid differentiation is essential for effective patient triage.

Another significant driver is the growing geriatric population in the United States. As the number of individuals aged 65 and older increases, the incidence of severe respiratory complications rises proportionally. This demographic shift necessitates a higher volume of sensitive PCR testing to ensure early intervention and reduce the risk of hospital-acquired infections, which are major concerns for US healthcare facilities.

Furthermore, the expansion of point of care (POC) molecular testing is revolutionizing the US diagnostic landscape. With more PCR platforms gaining CLIA-waived status, high-complexity testing is moving closer to the patient. This accessibility allows for immediate clinical decision-making in physician offices and pharmacies, which is a major catalyst for the market's sustained growth.

Technological Advancements and Automation

The US market is also characterized by a high demand for laboratory automation. To combat a shortage of specialized laboratory personnel, many US diagnostic centers are investing in "sample to result" systems. These platforms minimize manual handling and reduce the time to result, allowing high-throughput laboratories to process thousands of samples daily with minimal human error.

Technological innovation extends to the software level as well. The integration of artificial intelligence for result interpretation and the use of cloud-connected diagnostic instruments allow for real-time epidemiological surveillance across the country. This digital integration is a key factor that keeps the US market ahead of other regions in terms of diagnostic sophistication.

Top Industry Leaders in the US Market

The competitive landscape in the United States features a mix of global diagnostic giants and innovative biotech firms. These players are focused on developing high-sensitivity assays that can meet the rigorous demands of the US regulatory and clinical environment. Top players include:

Future Trajectory: Towards 2034

As the US continues to refine its diagnostic infrastructure, the focus is shifting toward "personalized" respiratory care. This involves using PCR not just for pathogen identification, but also for identifying genetic markers of drug resistance, particularly in bacterial infections like pneumonia and tuberculosis. This move toward precision medicine will further entrench the US as a leader in the respiratory diagnostics space.

With a projected market size of US$ 15.59 billion by 2034 and a CAGR of 10.72%, the US is set to remain the epicenter of PCR respiratory diagnostics. The combination of advanced technology, supportive government initiatives, and a clear clinical need ensures that the US will continue to dominate this vital sector for the foreseeable future.

Related Report : X-Ray Detectors Market Overview and Growth by 2028

Contact Information -

Email: [email protected]

Phone: +1-646-491-9876

Also Available in Korean German Japanese French Chinese Italian Spanish