Steam Turbine Market — Strategic Preview for 2026 Corporate Decisions

As corporate leaders and project sponsors prepare capital allocation plans for 2026, the steam turbine market is quietly entering a phase where incremental technology, regulatory shifts, and sectoral demand patterns will determine winners and losers. This preview synthesizes the essential macro trajectory, competitive dynamics, regulatory inflections, and near‑term tactical implications that PW Consulting’s full Steam Turbine Market study unpacks in operational detail. Think of this as the trailer: rigorous, evidence‑based, and strategically oriented — but designed to lead decision‑makers to the full report for the segmented datasets, supplier scorecards, and executable playbooks required for direct action.

Steam Turbine Market

Macro trajectory: modest growth, strategic significance

The market reached a base size in 2025 consistent with multi‑decade investments in thermal and combined‑cycle infrastructure. Our model — calibrated over the 2020–2025 historical window and projecting to 2032 — shows a steady, moderate expansion at a compound annual growth rate (CAGR) of roughly 2.8% through the forecast period. By 2026 the market is forecast to continue growing from the 2025 base, and it reaches its projected near‑term endpoint in the 2030–2032 window before flattening. The implication is clear: absolute market expansion is steady but not explosive, which shifts the strategic imperative away from hunting volume and toward capturing value through technology differentiation, aftermarket services, and project capture in expanding niches.

Steam Turbine Market

Why 2026 is a strategic inflection

- Regulatory gating: Several major jurisdictions implemented or announced tighter performance standards and retrofit timelines that materially affect new procurement specifications and life‑extension strategies for existing plants.

- Capital allocation pivot: Governments and institutions have signaled targeted funding to improve thermal cycle efficiency and to accelerate low‑carbon conversions, creating windows for co‑funded modernization programs.

- Niche demand vectors: Critical new demand from hyperscale AI data centers and advanced reactors is reshaping procurement timetables and technical requirements for steam turbine solutions.

For 2026 decisions, the combination of modest top‑line growth and concentrated, high‑value demand pockets creates opportunities for focused bets. The right moves are not necessarily bigger bids — they are smarter ones.

Steam Turbine Market

Key dynamics shaping investment and procurement choices

- Regulation and performance thresholds: Recent standards introduce efficiency subcategories and lifecycle conversion requirements in major markets, which re‑price older plant assets and accelerate decisions around conversion, CCS retrofits, or early replacement. These rules make efficiency claims and retrofit compatibility non‑negotiable in RFPs.

- Targeted public funding: Material allocations from energy agencies to improve steam cycle efficiency create co‑investment pathways for OEMs and EPCs — a lever for projects that would otherwise remain marginal.

- Hydrogen and fuel flexibility: OEM roadmaps and a few early field projects are already building hydrogen‑capable designs into steam turbine offerings. For firms evaluating R&D or partnership investments in 2026, hydrogen compatibility is a waypoint toward long‑term competitiveness rather than an optional feature.

- Data center driven combined‑cycle workstreams: Hyperscale computing demand is accelerating combined‑cycle deployments where steam turbines are integrated into high‑availability power islands. These projects emphasize rapid commissioning, modularity, and aggressive O&M SLAs.

- Supply chain volatility: Tariff regimes and alloy price movements have elevated input costs for critical nickel‑ and chromium‑based components, pressuring margins and making vertical integration or strategic sourcing partnerships more attractive.

Competitive landscape — who matters and why

The market is commercially consolidated in the sense that a handful of multinational OEMs and large regional suppliers dominate large utility and industrial procurements. The competitive set includes legacy OEMs with broad global footprints and newer challengers that are winning orders via price, local presence, or niche capabilities. Top players to monitor (company HQ, web reference, and strategic positioning) include:

- Siemens Energy AG — Erlangen, Germany (https://www.siemens-energy.com). A full‑spectrum supplier focused on high‑efficiency designs across conventional, combined‑cycle and nuclear applications, with recent wins in advanced reactor and hyperscale data center projects.

- GE Vernova Inc. — Cambridge, MA, USA (https://www.gevernova.com). A dominant installer of combined‑cycle steam capacity globally, with a product portfolio tailored to large power plants and reheat‑optimized designs.

- Mitsubishi Heavy Industries, Ltd. — Tokyo, Japan (https://www.mhi.com). Positions in high‑efficiency turbines and hydrogen co‑firing compatibility, leveraged into gas‑turbine combined‑cycle platforms.

- Dongfang Electric Corporation Ltd. — Chengdu, China (https://www.dongfang.com). A major supplier of large‑scale turbines for utility and industrial customers with strong domestic scale and export ambitions.

- Shanghai Electric Group Co., Ltd. — Shanghai, China (https://www.shanghai-electric.com). Large steam turbines for utility‑scale and combined‑cycle systems, competing aggressively on price and delivery.

- Doosan Enerbility Co., Ltd. — Seoul, South Korea (https://www.doosanenerbility.com). Active in combined‑cycle and data center power projects; notable for recent North American orders.

- Bharat Heavy Electricals Limited — New Delhi, India (https://www.bhel.in). Strong domestic presence focused on power generation and cogeneration applications.

- Toshiba Energy Systems & Solutions Corporation — Tokyo, Japan (https://www.toshiba-energy.com). Supplier of turbine‑generator sets for industrial and combined‑cycle uses.

- Ansaldo Energia S.p.A. — Genova, Italy (https://www.ansaldobreda.com). Specializes in combined‑cycle and cogeneration steam turbines, often chosen for tailored plant solutions.

- Harbin Electric Corporation — Harbin, China (https://www.heco.com.cn). Competitive on domestic and select export projects with an emphasis on cost and scale.

Collectively, the largest manufacturers command a meaningful share of total installed capacity; the market’s top tiers capture close to half of flows, leaving mid‑tier and regional vendors to fight over replacement, small‑scale industrial, and aftermarket business. This structure shapes bargaining power in procurement and the economics of aftermarket service contracts.

Recent deal and project signals (select)

- Siemens Energy was selected to supply steam turbine generator sets for a major 1 GW AI data center power project (Jan 2026).

- Doosan Enerbility signed a contract in March 2026 for two high‑capacity steam turbines and generators for a U.S. data center deployment.

- Siemens Energy secured a design and delivery contract for a condensing steam turbine for an advanced reactor program (Nov 2025), and reported a material order backlog that influenced supply availability and lead times.

These transactions highlight two strategic currents: hyperscale computing as an emerging anchor demand source, and advanced‑reactor procurement creating specialist opportunities in the nuclear condensed‑steam segment.

What the full PW Consulting report delivers (operational value)

PW Consulting’s comprehensive study translates the macro narrative into decision‑ready inputs. The full deliverable includes:

- Detailed market sizing and a transparent forecast model (base year 2025; 2026–2032 forecast) with downloadable spreadsheets.

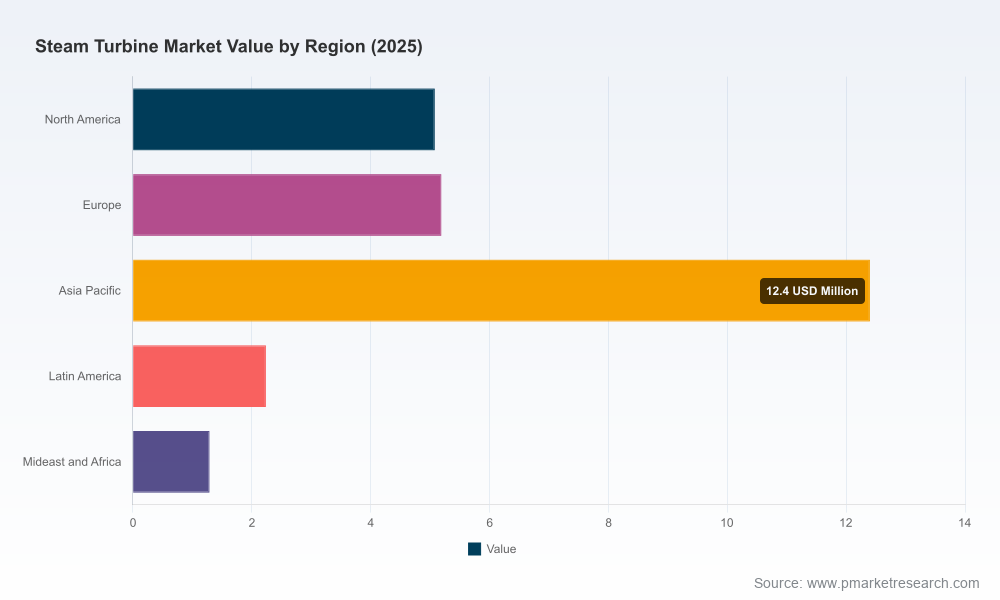

- Segmented demand models by region, application and turbine type, with sensitivity scenarios reflecting regulatory and fuel‑price shocks (note: segmented numeric tables are available in the full report).

- Supplier benchmarking across technical capability, delivery lead time, aftermarket footprint, and risk exposure, enabling fast shortlist creation for procurement teams.

- Technology deep dives: hydrogen co‑firing readiness, high‑temperature alloys, advanced seals and rotor designs, and digitalization roadmaps for condition‑based maintenance.

- Supply chain stress tests: commodity exposure mapping, tariff scenario analyses, and strategic sourcing playbooks.

- Policy impact analysis: quantifying how specific standards and incentive programs change asset lifecycles and retrofit economics across our forecast horizon.

- Transaction advisory annex: M&A and JV target screening, valuation overlays, and go‑to‑market considerations for OEMs seeking to expand into data center or SMR/advanced reactor segments.

Practical 2026 action agenda for corporate leaders

- Align procurement specifications to regulatory forward paths: embed efficiency and retrofit compatibility clauses now to avoid stranded asset risk as performance standards tighten.

- Prioritize modular, serviceable designs for data center and combined‑cycle bids: shorter lead times and robust O&M service commitments win in these fast‑turnaround projects.

- De‑risk alloy exposure: secure multi‑tier sourcing contracts or consider strategic inventory contracts with suppliers where nickel and chromium affordability is material to margins.

- Invest in hydrogen readiness: small, staged upgrades to accept higher hydrogen blends are lower cost than late‑stage retrofits and preserve optionality for fuel‑switching markets.

- Monetize aftermarket: shift commercial focus toward long‑duration service agreements and digital performance contracts that stabilize revenue as equipment sales growth remains moderate.

- Leverage co‑funding: pursue projects that layer public R&D/efficiency funds onto private capital to improve project IRR and shorten payback for high‑efficiency upgrades.

Closing: where to place your bet in 2026

The steam turbine market in 2026 resembles a mature industrial market with targeted pockets of disruptive growth. The strategic premium goes to organizations that convert technical differentiation into contractual outcomes — whether through hydrogen‑ready turbines, performance‑based service agreements, or winning the procurement playbooks favored by hyperscale and advanced‑reactor customers. If your 2026 plan includes procurement, manufacturing investments, or M&A in the steam turbine ecosystem, the decisions you take now should reflect the dual realities of modest aggregate growth and concentrated, high‑value niche demand.

PW Consulting’s full Steam Turbine Market report contains the segmented figures, supplier scorecards, downloadable forecast models, and transaction annex that translate this preview into a 90‑day execution plan. For the granular data that underpins procurement bids, supplier shortlists, and portfolio allocation models, access the complete study through our report page.

For detailed analysis of this topic, please visit the official page:Steam Turbine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com