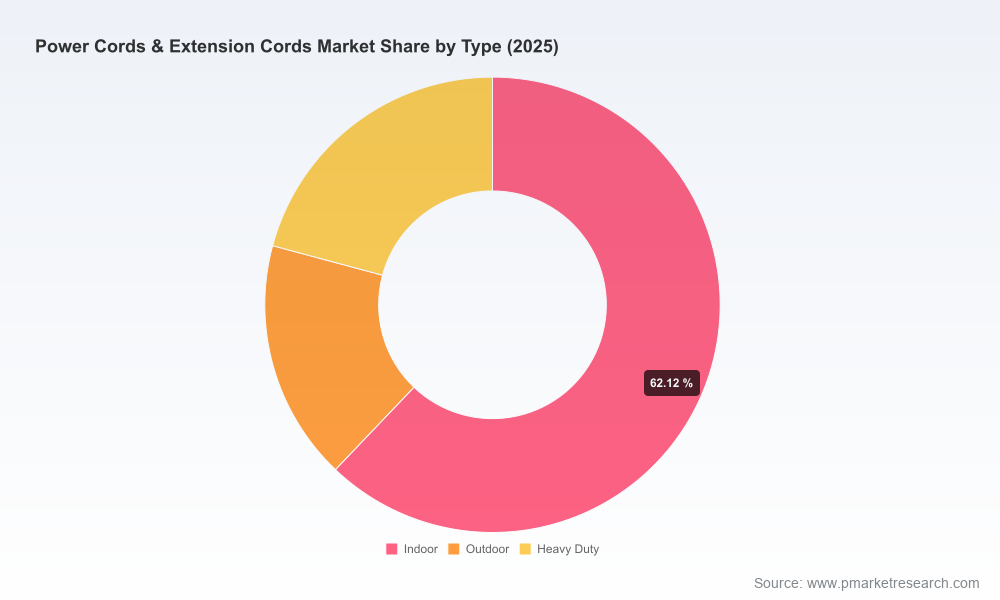

Power Cords & Extension Cords Market — 2026 Strategic Brief

Executive snapshot

As of our 2025 base year, the global Power Cords & Extension Cords market stands at approximately USD 4.4 billion (USD Million unit reporting). Between 2026 and 2032 the market is projected to grow at a compound annual growth rate (CAGR) of roughly 6.2%, rising toward an expected market size in the vicinity of USD 6.7 billion by 2032. The trajectory reflects steady end‑market demand across residential, commercial and industrial applications, coupled with ongoing product premiumization and regulatory-driven product upgrades.

Power Cords & Extension Cords Market

For executives and investors preparing strategic plans in 2026, this research functions as a decision-grade primer: it converts macro momentum into targeted implications for sourcing, product strategy, compliance investment and M&A prioritization, while preserving the granular datasets and segment tables for secure access in the full report.

Power Cords & Extension Cords Market

Why this report changes 2026 decisions

- Investment allocation: Translate market growth and margin sensitivity into prioritized capital projects (capacity expansion, automation, or localized production).

- Sourcing & procurement: Calibrate vendor strategies, hedge programs and inventory buffers in response to raw-material volatility and regional pricing differentials.

- Product roadmaps: Identify where to invest in higher value variants (medical-grade, heavy-duty, safety-enhanced cords) that command premium margins.

- Regulatory compliance: Scope certification timelines and redesign costs required to meet updated standards impacting cord set specifications.

- M&A and partnership scouting: Target scale or technology gaps with validated market sizing, competitor profiles and a transaction heatmap.

- Channel & commercial strategy: Optimize go-to-market plays by pairing product type with distribution partners, retail strategies and OEM contracts.

Market drivers, headwinds and near-term shocks

Three forces will primarily shape outcomes in 2026:

Power Cords & Extension Cords Market

- Regulatory tightening: Standards bodies updated UL 817 in July 2025, introducing new requirements for heater‑use power‑supply cords and tightening expectations across cord set safety. These changes create near-term compliance costs but also open differentiation routes for certified suppliers and higher-margin certified SKUs.

- Raw-material price volatility: PVC, a core input for insulation and jacketing, has displayed geographic price divergence through early 2026 — with reported April figures of roughly USD 735.45/MT in China and approximately USD 822.45/MT in the United States. Such differentials materially affect regional cost-to-serve and should inform sourcing and pass-through strategies.

- Demand heterogeneity & premiumization: Across residential retrofit cycles, commercial fit-outs, and industrial electrification, customers increasingly value safety features, longer lifecycles, and certified solutions. This supports a price‑tier segmentation strategy rather than a commodity race to the bottom.

Competitive landscape: structure and strategic implications

The market exhibits moderate fragmentation: the three leading firms collectively account for under one third of global revenues, while the top five approach roughly two-fifths of the market. That structure yields a competitive environment in which regional champions and specialized OEM suppliers coexist with larger integrated manufacturers.

Key players profiled in this study include:

- Southwire Company LLC — an integrated manufacturer and supplier with strength in building wire and extension cord systems for industrial and commercial segments. Southwire’s scale and channel relationships make it a natural candidate for capacity plays and bundling with upstream cable products.

- Volex plc — a global integrated cord and connector manufacturer serving consumer, data center and industrial customers. Volex’s engineering and contract-manufacturing capabilities position it well for OEM partnerships and rapid customization.

- Havells Ltd — a consumer and commercial player with broad product portfolios in home electricals, providing distribution reach in fast-growing markets.

- Goldmedal Electricals and regional manufacturers such as Ningbo Biaoda and Jiaxing Hongzhou — examples of strong cost-competitive players that also serve multinational supply chains as OEM/ODM partners.

- Specialists and premium suppliers (e.g., Kord King, Electri‑Cord Manufacturing, Webber Electronics, Z‑Tronix, Quail Electronics) — focused on medical-grade, hospital-grade, heavy-duty and geographically certified cord sets; these firms command higher margins in niche segments and are attractive targets for buyers seeking differentiation.

Strategic takeaways from the competitive map:

- Scale matters for channel control and OEM contracts, but specialization (certified medical, heavy-duty) defends margins and can justify higher multiple valuations.

- Regional manufacturing footprints and low-cost OEM partners remain indispensable given raw-material and labor cost dispersion.

- Consolidation opportunities exist for firms seeking to expand product breadth or acquire certifications and assembly capacity rapidly.

What the full report delivers (practical, action-oriented contents)

We designed the study as a toolkit for 2026 operational and strategic moves — not as an academic overview. Highlights include:

- A comprehensive market model (historical 2020–2025; forecast 2026–2032) with scenario outputs and sensitivity to key variables.

- Segment frameworks across type, application and geography with interactive dashboards — granular tables and downloadable spreadsheets are included in the full package.

- Regulatory impact assessment (including implications of the July 2025 UL 817 revision), cost-to-certify estimates, and suggested timelines for compliance projects.

- Raw-material cost build-ups and a PVC sensitivity model that allows procurement teams to stress-test margin outcomes under different price paths and sourcing mixes.

- Supplier & OEM database with capability matrices, lead-time benchmarks and quality indicators tailored for sourcing RFPs.

- Commercial playbooks: channel structures, pricing benchmarks, product launch checklists and negotiation templates for distributors and large OEMs.

- M&A heatmap and valuation comparables, including precedent deals, integration risks and a shortlist of targets by strategic rationale (scale, capability, certification).

- Practical templates: CAPEX calculators, SKU rationalization worksheets, NPV models for new factory investments and a procurement hedging primer.

Actionable recommendations for 2026 (prioritized)

- Immediate: Audit your product portfolio for UL 817 exposure and fast-track certification or redesign programs for heater‑use cord applications to avoid supply disruptions and recall risk.

- Procurement: Implement a tiered hedging strategy for PVC inputs, combine long‑term contracts with regional spot coverage, and qualify alternative materials and suppliers to reduce single‑source risk.

- Commercial: Rebalance SKUs toward certified and premium variants where willingness-to-pay is higher; develop bundled service offerings (warranty, traceability, installation support) for B2B customers.

- Manufacturing footprint: Model nearshoring and dual-sourcing scenarios — fixed-cost investments should be sized against the forecast CAGR and local labor/cost curves rather than raw capacity expansion alone.

- M&A & partnerships: Target smaller specialists with certification depth or unique die/molding capabilities to accelerate entry into high-margin segments without lengthy organic ramp-up.

- Digital & quality: Invest in product traceability, supplier scorecards and digital order-to-delivery visibility — they compress working capital and enhance compliance reporting.

How to use this research in boardroom and operational planning

For C-suite and Board-level planning, the study provides the market narrative and validated numerical scaffolding to set FY26–27 capital allocation, define inorganic growth corridors, and quantify regulatory capital needs. For procurement and operations teams, it supplies the raw-material sensitivity models, supplier shortlists and benchmarking tools required to negotiate contracts and plan capacity.

We also provide engagement options for bespoke work: rapid due-diligence packages for transactions, a 90‑day supplier diversification sprint, or a certification-cost immersion for engineering teams. These services embed the report’s outputs into executable plans tailored to client constraints and timetables.

Closing note — the teaser principle in action

This brief demonstrates the analysis depth and the strategic framing you will receive in PW Consulting’s full market study. To preserve the commercial integrity of the proprietary segment tables, regional and application breakdowns, and downloadable financial models (all included in the paid report), we have intentionally withheld the granular line‑by‑line segment figures here. These datasets, together with the full company profiles and transaction annexes, are available through the report portal and form the basis for our advisory engagements.

If your 2026 plan depends on precise segment sizing, supplier benchmarking, or certification-cost estimates, the full report and our follow‑on consulting packages will connect the dots from market signal to executable program.

For detailed analysis of this topic, please visit the official page:Power Cords & Extension Cords Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com