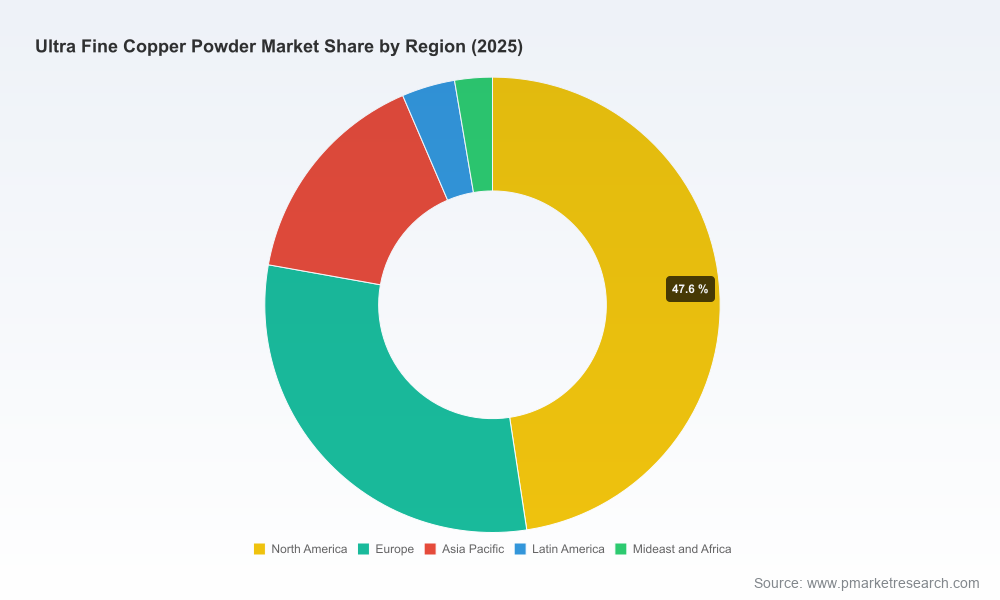

Ultra Fine Copper Powder Market: A Strategic Preview for 2026 Decision-Makers

This briefing is a targeted, strategy-first preview of PW Consulting’s forthcoming Ultra Fine Copper Powder Market study. It synthesizes the hard market facts you need to shape 2026 plans, demonstrates the analytical depth behind our work, and maps the concrete strategic options available to producers, buyers and investors — while intentionally withholding granular segment-level tables and regional breakdowns to prompt direct access to the full study for transaction-ready detail.

Ultra Fine Copper Powder Market

Why this market matters in 2026

Ultra fine copper powder (UFCP) occupies a distinctive intersection of advanced materials and electrification trends. From high-density electronics (MLCC electrodes, conductive inks) to emerging uses in additive manufacturing and next‑generation power devices, demand drivers are broadening and moving up the value chain. Our modeling shows the global market expanding at a compound annual growth rate (CAGR) of 7.42% in the forecast window (2026–2032), building on robust growth from the 2020 baseline through the 2025 reference year. In nominal terms, the market has moved materially from a five‑year legacy base into a higher‑growth phase, and our central forecast projects meaningful expansion by the end of the 2032 horizon.

Ultra Fine Copper Powder Market

What PW Consulting delivers — practical, executable intelligence

- Forward-looking market sizing and revenue drive-models (base year 2025; forecast period 2026–2032) that convert macro trends into actionable demand scenarios for procurement and capacity planning.

- Segmentation frameworks (by production technology, particle morphology and application archetypes) that explain where technical differentiation translates into margin premium — without disclosing the detailed splits in this preview.

- Supply-side diagnostics — energy and raw-material intensity maps for atomization and wet-process routes, unit-cost curves under alternate energy-price scenarios, and sensitivity tests that show breakpoints for competitive viability.

- Regulatory and compliance playbooks — a granular REACH and nanoparticle-safety risk matrix with capex estimates for pollution control and emissions abatement options, tailored to different plant sizes and geographies.

- Competitive benchmarking and supplier scorecards — technology, capacity, product breadth and go-to-market strength for Tier‑1 and regional players, designed to support sourcing decisions, JVs and M&A screening.

- Commercial tools — price-elasticity matrices, customer willingness-to-pay segmentation, and route-to-market playbooks for high-value applications like MLCC electrode pastes, conductive inks, and additive manufacturing feedstock.

- Deal support modules — target lists, synergy estimators and quick valuation heuristics for buy-side due diligence or divestiture planning.

Market dynamics through a 2026 lens

- Demand sophistication: End-markets are increasingly valuing ultra‑fine powders for specific performance attributes (particle size distribution, surface treatments, purity). This is shifting competition away from commodity copper to engineered grades that command premium pricing and stronger customer lock‑in.

- Electronics and energy systems: Electrification and higher-frequency electronics create sustained structural demand. Manufacturers of MLCCs and conductive pastes are particularly sensitive to particle-grade consistency and surface chemistry — areas where producers with proprietary atomization or post-treatment capabilities are gaining share.

- Production economics: Atomization routes that produce ultra‑fine powders are energy‑intensive. Energy cost volatility is therefore a first‑order margin risk; producers with lower energy exposure, on-site recycling, or more efficient process yields will have a durable advantage.

- Regulatory constraints and opportunity: Regulatory compliance (especially REACH-like nanoparticle controls) is a double-edged sword — it raises compliance costs and time-to-market for some suppliers, but it also erects quality and safety barriers that favor larger, well-capitalized players and certified facilities.

- Recent industry moves: Capacity expansions and targeted product launches in 2024–2025 indicate incumbents are focusing on high-purity, surface‑treated grades and MLCC-focused output. These tactical moves reflect a broader strategic pivot: prioritize higher-margin, specialized applications rather than competing on commodity price alone.

Competitive landscape — structure and implications

The industry shows a moderate concentration profile: the top three firms account for a meaningful share of market value, and the top five widen that footprint further. This structure creates a market where national champions and specialized technology leaders coexist with nimble regional specialists.

Ultra Fine Copper Powder Market

- Established Japanese players with proprietary atomization and wet-process capabilities are strong in electronics-grade high-purity powders and have strategic relationships with MLCC and electronic component manufacturers. Their strength is technical depth, process control, and long-term customer contracts.

- European and North American suppliers compete on specialized alloys, surface treatments and certification capabilities that appeal to high-reliability and additive manufacturing users.

- Chinese producers are scaling capacity and pushing into sub-micron grades, with expanding offerings targeted at high-volume applications and domestic OEMs — creating pricing and availability pressure in specific regional channels.

- Newer entrants and specialized firms (surface-treatment specialists, flake/flake-like morphologies, and AM-dedicated feedstock providers) are carving out niches where product differentiation and supply assurance matter more than scale.

Strategic takeaway: scale matters for compliance and capital intensity, but technology and customer intimacy create defensible pockets. Buyers and investors should evaluate both the capital base and the extent of product-engineering capability when scoring partners or targets.

Priority strategic moves for 2026

We recommend that decision-makers take three concurrent actions in 2026 to position for the next cycle of value creation:

- Secure differentiated supply and long-term offtake agreements. For OEMs and component-makers, moving beyond spot spot-market buys toward collaborative supply agreements reduces quality risk and supports co‑development of tailored powders (particle size, coating, purity).

- Invest in compliance and process efficiency. For producers, allocate a material portion of 2026 capex to emissions control, nanoparticle mitigation and energy-efficiency upgrades. This not only reduces regulatory exposure but improves unit costs under stressed energy scenarios.

- Pursue targeted vertical or adjacent moves. Manufacturers with materials science capabilities should evaluate playbooks into conductive inks, MLCC-paste formulations or additive-manufacturing feedstock. Conversely, downstream OEMs can consider minority investments in specialist powder producers to secure technology roadmaps and pricing predictability.

Scenario thinking and decision-support framework

Our scenario set in the full report isolates three plausible 2026–2028 pathways — a "consolidation & premiumization" scenario, a "broad supply build-out with price pressure" scenario, and a "regulatory-tightening shock" scenario. Each is modeled across demand, price and margin impacts, with trigger points and recommended tactical responses. Key decision-support tools included are:

- Heatmaps that rank application-by-technology attractiveness under different pricing regimes (note: detailed heatmap values are available only in the full study).

- Supplier stress-tests combining energy prices, regulatory capex and yield assumptions to reveal at-risk capacities and likely M&A flow.

- Transaction scorecards with threshold criteria (technology, certification status, customer contracts, geographic compliance readiness) tuned for buy-side screening in 2026.

What to watch in the near term

- Regulatory rulings around nanoparticle safety: expect rulings to create both compliance costs and market advantage for certified producers.

- Energy-price volatility: producers with hedges, captive renewables or efficiency projects will preserve margin advantage.

- Technology launches and surface-treatment innovations: those that reduce oxidation and improve dispersion in inks/pastes will unlock new premium segments.

- Consolidation signals: watch for strategic acquisitions of specialty producers by vertically integrated electronic-materials firms or private equity plays focused on roll-ups.

How PW Consulting’s full study helps your 2026 playbook

This preview is designed to orient strategy. The full Ultra Fine Copper Powder Market report is operational — it contains the granular scenario outputs, supplier scorecards, regional demand overlays and transaction-ready target shortlists that organizations need to execute in 2026. Use it to:

- Create a prioritized 24-month capex and compliance plan that aligns with demand scenarios and regulatory timelines.

- Negotiate supply agreements using modeled price and availability forecasts rather than spot quotes.

- Screen M&A targets with a bespoke scorecard that weights technology defensibility, customer contracts, and compliance readiness.

For executives preparing budgets, procurement roadmaps, or M&A pipelines in 2026, the strategic value of this research is immediate: it translates macro growth and risk inputs into transaction‑ready insights, prescriptive operational steps and defensible investment priorities — while keeping the granular segment tables and supplier-specific valuations in the locked, source-grade deliverable that accompanies the study.

To move from directional strategy to executable plans — including the full set of segmentation tables, regional demand drilldowns, supplier scorecards and scenario worksheets — access the complete PW Consulting Ultra Fine Copper Powder Market study and our bespoke advisory services.

For detailed analysis of this topic, please visit the official page:Ultra Fine Copper Powder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com