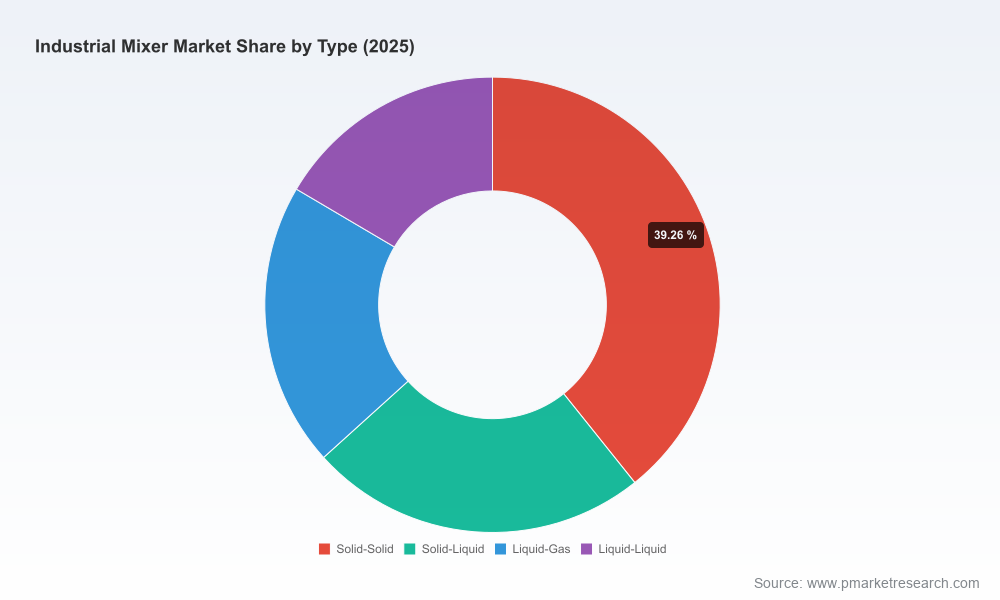

Industrial Mixer Market 2026: A Strategic Preview for Executive Decision-Making

Executive snapshot

As industrial end-users recalibrate capital plans entering 2026, the global industrial mixer market is on a clear expansion trajectory. Our base-year sizing (2025) identifies the market at approximately USD 215 million (revenue, Million USD unit), with a compounded annual growth rate (CAGR) of 6.98% projected across the 2026–2032 forecast window. Under the central-case forecast the market is expected to climb steadily through the decade, reflecting a recovery from early‑decade volatility and accelerating demand across industrial, construction and process manufacturing segments.

Industrial Mixer Market

These headline figures mask important structural nuances: the market remains commercially fragmented, with the top three vendors accounting for roughly a quarter of global revenue. Such fragmentation creates outsized opportunities for focused scale plays, regional specialists and vertically integrated suppliers that can combine product engineering with aftermarket services.

Industrial Mixer Market

Why this study matters for 2026 decisions

- Capex prioritization under shifting tax regimes: New 2025 legislation introduces material incentives for investments in domestically manufactured machinery, reshaping payback calculations for near‑term equipment purchases and localization investments.

- Supply‑chain and raw‑material risk: Stainless steel and specialty alloy price volatility directly reweights supplier selection, total landed cost and lead‑time risk; procurement teams must re-base sourcing and hedging assumptions now.

- Regulatory and compliance cost drivers: Equipment designed to meet national codes and certified control systems meaningfully reduces commissioning risk in regulated sectors (food, pharma, chemical), and can be a differentiator in procurement tenders.

- Service and aftermarket as margin lever: In a market with moderate concentration, technicians, spares and retrofit services drive recurring revenue and customer stickiness—often more predictable than new machine sales.

- Technology and performance premium: High‑shear, multi‑shaft and intensive mixing solutions command a premium where process yield improvements or throughput gains are quantifiable—an area ripe for pilot deployments and payback proof points.

What the PW Consulting report delivers (practical, operational content)

- An audited market sizing and multi‑scenario financial model covering 2020–2032 (base year 2025) with adjustable assumptions for CAGR, raw‑material inflation and regional demand shocks.

- Demand-driver mapping and a decision matrix tying mixer types to measurable process outcomes (yield, cycle time, energy intensity) for chemical, food & beverage, pharmaceutical and heavy construction users.

- Supplier risk and resilience heatmaps: lead‑time, raw‑material exposure, manufacturing footprint and tariff sensitivity.

- CapEx ROI calculators and TCO templates that embed tax incentives, accelerated depreciation and service revenue forecasts—ready for board‑level investment cases.

- Competitive benchmarking tools including capability scorecards, product‑feature matrices and aftermarket revenue profiles (designed for M&A screening and sourcing negotiations).

- Go‑to‑market playbooks for vendors: channel strategies, value‑added services, digital retrofits and pricing levers to accelerate share capture in target verticals.

- Regulatory compliance checklist and factory acceptance test (FAT) templates aligned to major codes and certification regimes.

- Board‑ready scenario briefs for three stress environments: tariff shock, raw‑material spike and accelerated on‑shore procurement due to tax policy change.

Market dynamics and strategic implications

Three dynamics will define competitive outcomes in 2026. First, fiscal policy is actively reshaping sourcing decisions. Incentives that favor domestically produced equipment compress payback periods on local manufacturing investments and give a clear near‑term advantage to vendors with onshore production or U.S.‑aligned supply chains.

Industrial Mixer Market

Second, raw‑material cost swings—particularly stainless steel and alloy inputs—continue to flow directly to bill‑of‑materials and lead‑times. Companies that have invested in long‑lead inventory strategies, alternative grade qualification, or supplier partnerships will preserve gross margins. INDCO’s public commentary on raw‑material exposure highlights this operational reality: procurement and engineering teams must collaborate to validate alternative specifications without compromising process outcomes.

Third, customer purchasing behavior is bifurcating. Buyers seeking lowest total cost are increasingly valuing lifecycle services, digital monitoring and retrofitability over a simple purchase price. Equipment makers that can bundle IoT‑enabled monitoring, preventative maintenance contracts and rapid spare parts will capture higher lifetime value per installation.

Competitive landscape — profiles and strategic takeaways

- Charles Ross & Son Company (Hauppauge, NY) — Well established in ribbon blenders, planetary and high‑shear mixers, Ross emphasizes U.S.‑built systems and compliance‑level control packages. Their recent thought leadership on manufacturing localization and tax incentives underscores a strategic push to capture projects accelerated by 2025 incentives. For buyers prioritizing regulatory compliance and shortened procurement risk, Ross’s UL‑rated control systems and domestic engineering support are differentiators. (See: https://www.mixers.com/)

- INDCO (Hauppauge, NY) — Positions itself on fast lead times and domestic raw‑material sourcing. INDCO’s operational narrative centers on de‑risking supply chains for chemical, paint and food processors; procurement teams often shortlist them when lead‑time certainty is a gating requirement. (See: https://www.indco.com/)

- Dynamix Agitators (United States) — Specializes in custom, large‑scale batch mixers and agitators for heavy industries. Their engineering DNA suits applications where bespoke configurations and heavy‑duty materials are required; Dynamix is a logical partner when performance envelopes exceed standard catalog offerings. (See: https://dynamixinc.com/)

- CO‑NELE Mixer (China) — Strong in intensive and planetary mixers for concrete, refractory and high‑performance materials. CO‑NELE’s prominent trade‑show presence signals an aggressive export posture into construction and industrial segments, where price‑performance and scale are decisive. Their recent showcase at a major concrete exhibition reinforces outreach into European and international markets. (See: https://www.conelemixer.com/)

Tactically, vendors with domestic manufacturing, engineering customization capabilities and bundled aftermarket services are best positioned to convert the near‑term demand impulse created by tax incentives and shortened supplier lead times. For buyers, the vendor selection lens must widen beyond purchase price to include lifecycle economics, certification compliance and spare‑parts availability within your region.

Actionable plays for executives in 2026

- Recalculate capex under the new tax framework: run accelerated depreciation and Section 179 scenarios to quantify the true near‑term payback for localized purchases.

- Implement a supplier‑resilience scorecard: include lead‑time variability, material‑cost pass‑through clauses and dual‑sourcing readiness for critical alloy inputs.

- Prioritize pilot projects that demonstrate process improvements (yield, cycle time) with clear business cases—use these to justify premium investment in high‑shear or multi‑shaft technologies.

- Convert service contracts into growth engines: create tiered preventive maintenance packages and digital monitoring subscriptions to stabilize revenue and reduce churn.

- Consider targeted M&A or minority investments to secure capacity in key geographies or access specialized product lines that are difficult to replicate organically.

- Embed scenario planning into procurement rounds—model tariff, raw‑material and currency shocks against supplier proposals to avoid surprises in 12–18 month budgets.

Why PW Consulting’s report is indispensable for 2026

This report is designed as a working toolkit for operators, procurement leaders and corporate strategists facing fast‑moving fiscal and supply‑chain shifts. Beyond headline market sizing, it delivers executable artifacts: adjustable financial models, negotiation playbooks, technical acceptance templates and a decision matrix that connects mixer technology to measurable production outcomes.

We intentionally refrain from publishing the detailed segmentation and proprietary vendor-level datapoints in this preview. Those granular analytics—including split‑level forecasts, application‑specific unit economics and the full competitive scoring model—are available in the full report and interactive dashboards on our website. That deeper layer is purpose‑built to support capital allocation memos, procurement RFIs and M&A diligence in 2026.

Next steps

- Download the full Industrial Mixer Market report to access the scenario models, vendor scorecards and the complete segmentation detail necessary for board‑level decisions.

- Engage PW Consulting for a tailored executive workshop where we run your company’s capital plans through our tax‑incentive and supplier‑risk scenarios—delivering a prioritized investment roadmap you can present to the board within 30 days.

For detailed analysis of this topic, please visit the official page:Industrial Mixer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com