Infrared Color Sorter Market Trends, Share and Future Outlook Forecast 2034

Other |

2026-05-26 12:45:58

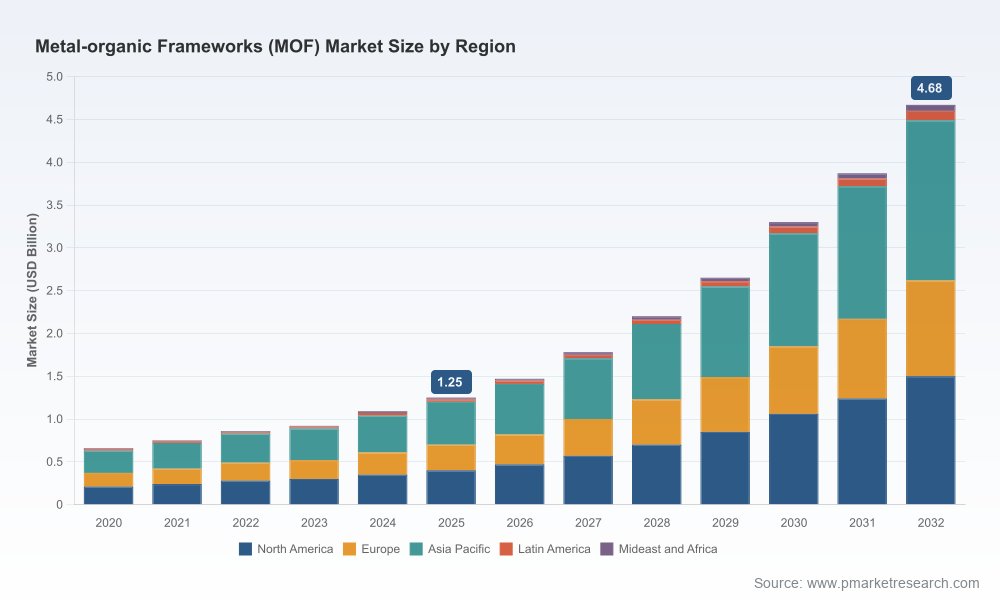

The metal-organic frameworks (MOF) sector has moved rapidly from academic curiosity to an industrially relevant materials market. Our proprietary market model—anchored on a 2025 base year with a historical window covering 2020–2025 and a forward-looking forecast to 2032—projects sustained, high‑teens to low‑twenties expansion. Specifically, the global MOF market is estimated at USD 1.25 Billion in 2025 and is forecast to reach USD 4.68 Billion by 2032, reflecting a compound annual growth rate (CAGR) of 20.6% over the 2026–2032 forecast period. This trajectory reflects concurrent advances in scalable synthesis, application validation (notably in carbon management and selective separations), and the gradual maturation of supply chains from laboratory to multi-ton production.

Metal-organic Frameworks (MOF) Market

Timing for commercialization: 2026 is the inflection year where several technology developers and incumbent chemical producers move from pilot or small‑scale production to commercial supply. That shift transforms MOFs from “emerging materials” to contractually viable inputs for industrial projects, changing procurement, long‑term contracting, and capital allocation decisions.

Metal-organic Frameworks (MOF) Market

Portfolio prioritization under uncertainty: With the market growing at >20% CAGR across the forecast window, firms must decide which MOF-enabled applications to prioritize (e.g., gas separations, carbon capture, catalysis, water harvesting). Strategic choice now will determine access to early commercial contracts, intellectual property positioning, and first‑mover supply advantages.

Metal-organic Frameworks (MOF) Market

Supply‑chain and scale-up risk management: The recent wave of commercial scale‑ups and kilogram‑to‑multi‑ton order fulfillments demonstrates both the opportunity and the operational risk associated with scaling MOF production. Firms must evaluate manufacturing partners, commit to appropriate offtake structures, and plan contingency capacity to avoid project bottlenecks.

Regulatory and ESG alignment: MOFs are tightly linked to decarbonization strategies (CO2 capture, biogas upgrading). Corporate and public procurement decisions in 2026 will be influenced by evolving carbon pricing, industrial emissions targets, and sustainability reporting. Early engagement with policymakers and standard‑setting bodies will be a competitive advantage.

Our full study is designed as an operational tool for executives, M&A teams, and product managers. The report moves beyond headline growth rates to provide the following practical outputs (previewed here at a high level to protect proprietary subsegment detail):

Market sizing and scenario modelling: Base case and stress scenarios calibrated to technology readiness, feedstock cost trajectories, and adoption curves for primary end uses. Readers will find deterministic and probabilistic demand paths to inform CAPEX timing and contract duration decisions.

Technology and cost roadmaps: Comparative analysis of production routes, economies of scale, and expected cost declines as suppliers move from kg‑scale to multi‑ton capacities. The roadmap identifies where process innovation is likely to unlock step‑changes in unit economics.

Customer and end‑use playbooks: Buyer personas, procurement windows, and pilot‑to‑scale conversion timelines for industrial customers in energy, chemical processing, and environmental services. The playbooks focus on commercial terms, qualification protocols, and trial metrics that win adoption.

Supplier scorecards and due diligence templates: Operational, quality, regulatory and IP checks needed to underwrite supply agreements. We evaluate manufacturers on scale‑up history, reproducibility, and compatibility with standard industrial equipment.

M&A and partnership roadmaps: A strategic matrix of likely targets, partnership archetypes, and dilution vs. control tradeoffs for companies seeking to acquire capability quickly or secure privileged supply.

The MOF vendor landscape now combines specialty chemical incumbents, dedicated MOF startups, and niche materials suppliers. Market concentration metrics indicate a moderate level of aggregation among the leading players, but significant opportunity remains for new entrants that solve scale and cost challenges.

BASF SE (Ludwigshafen, Germany): As an incumbent chemical producer, BASF has translated laboratory MOF formulations into a multi‑ton production capability aimed at industrial CO2 capture. Their execution on industrial scale‑up makes them a strategic partner for large industrial customers seeking assured supply and integrated engineering solutions.

Promethean Particles Ltd (Nottingham, UK): A notable example of a founder‑led scale‑up that has converted patented continuous‑flow synthesis into commercial orders. Their recent large‑volume order fulfillment and leadership hires signal readiness to serve demanding, near‑term commercial applications.

framergy, Inc. (College Station, US) and NuMat Technologies (Evanston, US): These suppliers emphasize application‑tailored adsorbents and coordination polymer derivatives for gas purification and selective adsorption. Their strength is in custom product engineering and close collaboration with OEMs.

NovomoF AG, Mosaic Materials, Decarbontek, MOFapps, Strem Chemicals, ACSynam and others: This cohort ranges from specialized MOF commercializers to high‑purity powder suppliers for research and early industrial trials. Several recent product launches and scale‑up announcements reflect maturation of supply options available to industrial buyers.

Recent developments to monitor: multi‑ton commercial production achievements, kilogram‑scale product launches for low‑cost carbon capture, and landmark order fulfillments by multiple vendors. These events reduce technology delivery risk but also raise competitive pressure on pricing and contractual terms.

For buyers (industrial end users and OEMs): Secure multi‑stage procurement arrangements that include trial volumes, qualification gates, and flexible volume commitments. Favor suppliers with credible scale‑up evidence and transparent quality systems.

For investors and corporate development teams: Prioritize exposure to suppliers that demonstrate both process scalability and route‑to‑market traction with anchor customers. Distinguish between IP‑heavy technology plays and manufacturing/scale plays; both have different return profiles and exit pathways.

For technology licensors and licensors: Consider licensing structures that align incentives for capital investment—e.g., revenue‑sharing, minimum purchase commitments, or stepped pricing indexed to volume tiers—rather than simple one‑off fees.

For policy makers and project developers: Recognize MOFs as an enabling technology for decarbonization projects and incorporate supplier risk into project appraisal and grant design. Early procurement incentives can accelerate local supply development and clusters.

Scale‑up execution: Laboratory performance does not always translate to plant‑scale reliability. Expect a two‑to‑three year window of operational learning for first‑wave commercial plants.

Feedstock volatility and cost pass‑through: Raw chemical inputs and energy prices can materially alter unit economics; integration with existing chemical platforms will mitigate but not eliminate exposure.

Standards and certification: Lack of harmonized industrial standards for MOF performance and testing could slow buyer adoption—especially in regulated industries like pharmaceuticals and aviation.

Competitive pricing pressure: As scale increases and low‑cost MOF formulations enter the market, margins for component suppliers may compress quickly, favoring vertically integrated players.

Run fast, staged pilots: Contract pilot volumes with two suppliers—one incumbent and one pure‑play—to de‑risk supplier dependence and accelerate learning.

Secure optionality in offtake agreements: Negotiate options for volume expansion and clear technical acceptance criteria to prevent lock‑in to underperforming materials.

Pursue selective vertical integration: For large adopters of MOF‑enabled solutions, consider partial backward integration or long‑term strategic equity in manufacturing partners to stabilize supply and capture margin.

Invest in qualification pathways: For regulatory or high‑integrity applications, allocate resources to co‑develop test protocols and standards with suppliers and external labs.

Monitor consolidation signals: Use M&A as a lever to secure IP or capacity when valuations reflect early commercial traction rather than speculative promise.

This briefing outlines the contours of a market transitioning to commercial scale. The headline numbers—USD 1.25 Billion in 2025 growing at a 20.6% CAGR to an estimated USD 4.68 Billion by 2032—show a high‑growth opportunity, but the commercial and operational nuances that determine winners and losers live below the top line. Our full market study provides the granular segmentation, supplier scorecards, scenario models, and transaction checklists executives need to make confident 2026 decisions. Consider this a strategic trailer: sufficient to plan your next moves, but intentionally preserving the fine‑grained intelligence that will be critical when you’re ready to execute. Contact PW Consulting to access the complete analysis and tailored advisory support for your MOF strategy.

For detailed analysis of this topic, please visit the official page:Metal-organic Frameworks (MOF) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com