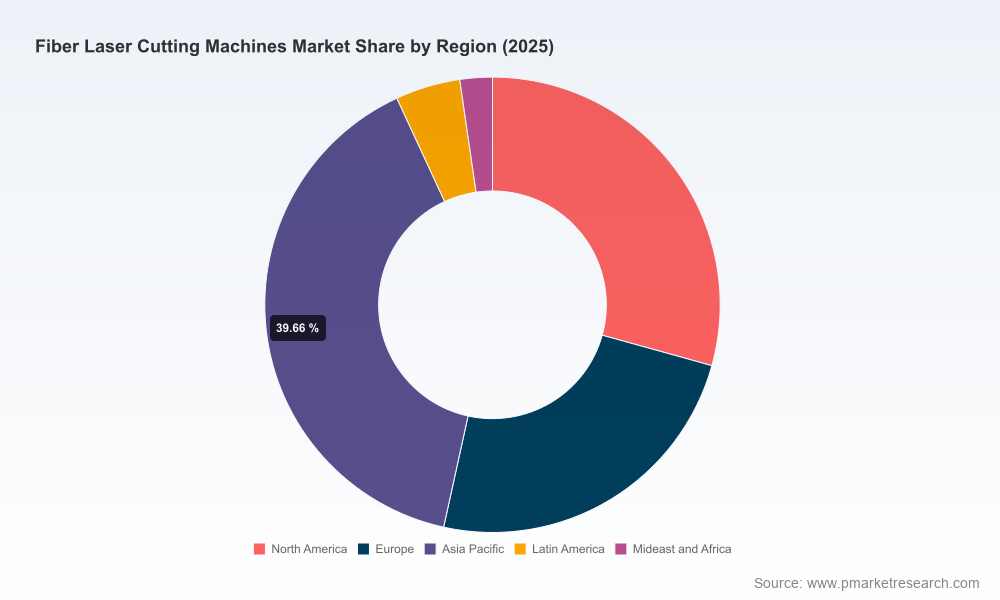

Fiber Laser Cutting Machines Market: Strategic Outlook for 2026 Decision-Makers

As PW Consulting’s Lead Industry Analyst, I present a concise strategic primer on the fiber laser cutting machines market to inform executive decisions entering 2026. Our latest market model uses 2025 as the base year and projects through 2032. At a compound annual growth rate (CAGR) of 5.3% the global market expands steadily in our forecasts — rising from an observed market size of USD 1.74 Million in 2025 to USD 2.51 Million by 2032 — a trajectory that materially affects capital allocation, product roadmaps, supply‑chain choices, and M&A timing across OEMs, job shops, and industrial end‑users.

Fiber Laser Cutting Machines Market

Why this research matters for 2026 strategy

- CapEx timing and replacement cycles: The market’s mid‑single digit CAGR signals an environment where measured capacity additions often outperform aggressive expansion. Firms that align procurement windows with technology upgrades (e.g., higher‑power single‑mode sources, integrated automation) can secure cost and productivity advantages while avoiding excess inventory.

- Product differentiation vs. commoditization: Increasingly, buyers evaluate systems on automation, energy consumption, and lifecycle cost rather than upfront price alone. The report helps prioritize product investments that produce durable differentiation in throughput, uptime, and integration capabilities.

- Supply‑chain resilience and critical materials: The fiber gain medium (rare‑earth, ytterbium‑doped fiber) and high‑precision optics are strategic bottlenecks. Our analysis traces supplier concentration, lead‑time sensitivity, and mitigation strategies critical for 2026 sourcing plans.

- Regulatory and safety compliance as a competitive filter: With OSHA, ISO, CE and FDA/CDRH requirements shaping procurement thresholds, companies that pre‑certify and package compliance as part of the offering shorten sales cycles and reduce purchase hesitancy.

What the full report contains (practical, actionable deliverables)

The published study is designed to be operational from day one. Highlights include:

Fiber Laser Cutting Machines Market

- Proven market sizing and forecasting model (historical 2020–2025; forecast 2026–2032) with transparent assumptions and sensitivity levers for energy costs, labor rates, and automation adoption.

- End‑user economics: total cost of ownership (TCO) calculators, payback models for retrofit vs full replacement, and material‑specific productivity benchmarks.

- Technology and product matrix: laser source architectures, beam quality tradeoffs, integration options for 2D/3D/bevel cutting, and automation packages with ROI estimates.

- Supply‑chain mapping: component tiering, single‑sourcing risk heatmaps, and recommended procurement strategies (dual‑sourcing, strategic inventory buffers, and supplier development playbooks).

- Regulatory and safety checklist: actionable steps to ensure compliance in major export markets and how certification can be used as a go‑to‑market lever.

- Competitive intelligence dossiers: structured profiles of market leaders and challengers with product roadmaps, capability gaps, and M&A watchpoints.

- Scenario and stress testing: how market outcomes shift under alternative energy price, automation adoption, and macroeconomic scenarios — model files are included for client customization.

Market dynamics that will determine winners and losers

- Energy efficiency mandates: National and corporate decarbonization targets are accelerating replacements of older CO2 and Nd:YAG systems with solid‑state fiber lasers. The energy and maintenance savings are key inputs to procurement decisions, and our models quantify paybacks across typical factory duty cycles.

- Automation and labor pressures: Persistent shortages in skilled fabrication labor are increasing demand for turnkey high‑throughput cells that combine fiber sources with robotic handling and advanced nesting. Buyers now value solutions that reduce manual set‑up and parts handling time.

- Component scarcity and technical concentration: The ytterbium‑doped fiber and precision optics form the technical core. We map supplier concentration and show how single‑mode high‑power breakthroughs change competitive dynamics and aftermarket economics.

- Regulation and safety: Compliance is non‑negotiable. Class 4 laser safety features, automated beam shutters, and certified enclosures are mandatory design considerations for new systems destined for regulated markets.

- Market concentration: The industry displays moderate concentration: the top three and top five suppliers account for meaningful shares of global shipment value — an important context for pricing power, channel strategy, and M&A rationale.

Competitive landscape — tactical takeaways

Our competitive analysis synthesizes product strengths, go‑to‑market models, and recent strategic moves. Selected observations:

Fiber Laser Cutting Machines Market

- IPG Photonics (Marlborough, MA): A world leader in fiber laser sources, IPG’s integrated systems and high‑power single‑mode innovations set the technical pace. Their recent recognition for an 8 kW compact single‑mode source underscores continued differentiation at high power and beam quality.

- TRUMPF (Ditzingen, Germany): Strong in industrial 2D systems and automation platforms, TRUMPF’s TruFiber line and new high‑productivity launches position it well for OEM customers with high‑volume, high‑automation requirements.

- Bystronic (Balgach, Switzerland): Known for systems integration, Bystronic’s modular machines and recent strategic acquisition moves expand its product scope and aftermarket capabilities.

- Coherent (Santa Clara, CA) and related players: With new industrial fiber platforms and strategic divestitures/acquisitions in play, the supplier landscape is dynamic — buyers should expect product convergence but also pockets of focused innovation.

- Regional and niche manufacturers (multiple HQs): Several companies specialize in vertical use cases (heavy‑duty cutting, engraving, large bed machines) and can be attractive acquisition or distribution partners for scaling into specific end markets.

Recent product launches and M&A through 2025–H1 2026 — including several high‑power platform introductions and a strategic acquisition expanding fiber capabilities — illustrate why incumbents and challengers alike are investing in both technology and route‑to‑market enhancements. These developments materially impact component demand, service networks, and aftermarket revenues.

Decision frameworks and recommended next steps for 2026

We translate market insights into practical actions across five stakeholder archetypes:

- OEMs: Prioritize modular architectures that permit field upgrades to higher‑power sources and integrated automation. Lock strategic supply agreements for fiber gain media and optics. Use our TCO models to redesign warranty and service packages that monetize uptime.

- Fabricators and job shops: Run the included payback and scenario tools before replacing legacy equipment. Target investments that reduce labor touchpoints and energy intensity to maximize mid‑cycle returns.

- Component suppliers: Invest selectively in capacity for critical fiber and optics and offer certification and traceability as premium features to OEMs seeking supply security.

- Private equity and strategics: Use the market concentration profile and company dossiers to identify consolidation targets with strong aftermarket potential or niche vertical dominance.

- Public policy and compliance teams: Integrate the safety and certification checklist into procurement policies to accelerate adoption and avoid post‑purchase retrofits that reduce ROI.

Why PW Consulting’s analysis is unique — the trailer principle in action

This briefing demonstrates the analytical depth you can expect from the full study: a rigorously sourced market model, proprietary TCO and scenario tools, granular competitive dossiers, and executable playbooks for procurement, product management, and M&A. Intentionally, this primer does not disclose the full granular regional and application splits or every line‑item financial table — those details are included in the report’s interactive dashboards and downloadable model workbooks, which clients can use to run bespoke scenarios for their business.

For decision‑makers preparing capital plans and go‑to‑market strategies in 2026, the most valuable contributions in the full report are: calibrated investment timing driven by our 2026–2032 scenario sets; supplier risk mitigation measures tied to critical materials; and a competitor action map that converts observed product launches and acquisitions into a 24‑month playbook.

Next step

To translate these insights into an executable 2026 plan, PW Consulting offers briefing packages that include a tailored workshop, access to the underlying model files, and a 90‑day implementation roadmap specific to your role in the value chain. Access to the full dataset, regional and application segmentation, and benchmarking matrices is available on the report landing page — consult the full report to unlock the granular intelligence required for decisive action.

For detailed analysis of this topic, please visit the official page:Fiber Laser Cutting Machines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com