Leather Goods Market Growth and Future Trends

Other |

2026-05-11 11:45:49

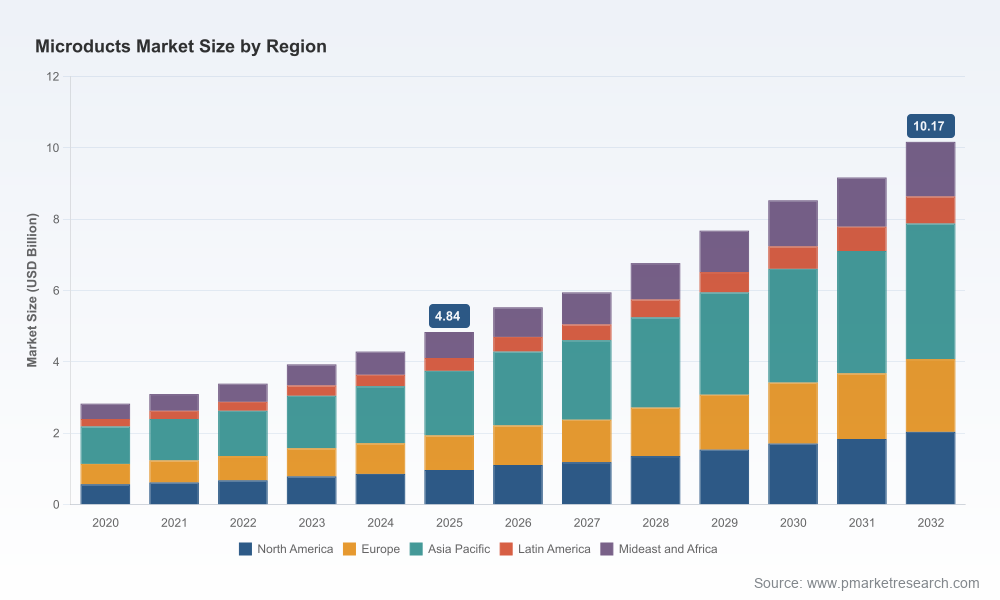

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present an executive preview of our Microducts Market study—designed to inform high‑stakes commercial choices in 2026. Anchored on a 2025 base year and a detailed 2026–2032 forecast horizon, the study quantifies a sector growing at a robust compound annual growth rate (CAGR) of 11.3% (USD, revenue unit: Billion). Our top‑line outlook shows the market expanding materially from the early 2020s into the next decade, highlighting both rapid adoption of fiber‑first network architectures and intensifying competition among suppliers.

Microducts Market

Capital allocation and project phasing: Operators planning FTTH, access modernizations, or data center buildouts need precise timing for microduct procurement to optimize capex and avoid penalty pricing during resin supply shocks or logistic surcharges.

Microducts Market

Supplier selection and contract design: With upstream HDPE feedstock volatility and variable certification requirements across jurisdictions, procurement teams must evaluate supplier resilience beyond price—manufacturing footprint, certification pedigree, and proven installation performance matter.

Microducts Market

Product and technology strategy: Vendors must choose where to compete—standard HDPE microducts, flame‑retardant indoor variants, multi‑microduct bundles, or integrated blown‑fiber systems—based on differentiated margins and adoption curves mapped in our forward scenarios.

M&A and alliance screening: The market exhibits mid‑to‑high fragmentation with meaningful share held by a limited set of global and regional players. Our playbook helps acquirers size target opportunity windows and forecast synergies under multiple regulatory and raw‑material scenarios.

Regulatory compliance and product spec evolution: New FOA and industry body guidance around blowability and diameter ranges, plus stricter indoor flame‑retardant mandates in developed markets, require rapid product updates and certification roadmaps.

PW Consulting’s Microducts Market study is structured as an operator’s and supplier’s toolkit rather than a purely academic analysis. Key deliverables include:

Top‑down and bottom‑up market sizing with scenario trajectories (base, upside, downside) across the 2026–2032 forecast window, stress‑tested for resin price shocks, logistics surcharges, and regulatory shifts.

Deployment economics models: downloadable CapEx/Opex templates to model trenching vs. microtrenching, direct burial vs. direct install tradeoffs, and the impact of blown‑fiber techniques on overall deployment velocity and lifetime cost.

Supplier scorecards and procurement playbooks covering factory footprint, production cadence, quality certifications (PPI, FOA), IP posture, and time‑to‑delivery risk assessments.

Go‑to‑market roadmaps for suppliers launching new microduct variants—pricing ladders, channel strategies, pilot deployment playbooks, and installation training modules that accelerate buyer acceptance.

Regulatory and standards tracker: country‑level compliance checklists, certification timelines, and recommended product formulations for flame‑retardant and indoor deployments.

M&A diligence pack: target filters, synergy levers, integration plan templates, and post‑deal value capture timelines calibrated to industry consolidation patterns.

Risk matrices: material cost hedging strategies, inventory optimization, and contingency plans for transport surcharges and geopolitically driven feedstock constraints.

The microduct market comprises a mix of polymer specialists, cable system integrators, and niche innovators. Our competitive analysis profiles market leaders and emergent challengers—focusing on capability vectors decision‑makers care about: product range, blown‑fiber competence, certification and standards compliance, manufacturing scale, and channel reach.

Emtelle Holdings Ltd (UK): A strong innovator in blown‑fiber tubing and RDB microduct systems. Recent strategic partnerships broaden their hardened connectivity offerings—an important signal for network operators seeking integrated vendor solutions rather than point products.

Primo (Italy): Known for multi‑microduct systems and customization capability. Their flexibility is attractive to service providers deploying in complex urban or multi‑dwelling environments that require tailored bundles.

Hexatronic Group AB (Sweden): Focused on air‑blown cables and high‑performance microducts. Their product set targets high‑velocity deployments and operators prioritizing future‑proofed blown‑fiber systems.

Prysmian Group (Italy): As a large, integrated cable manufacturer, Prysmian leverages scale to offer multiway microduct systems and bundled offerings—important for large national or cross‑border programs requiring single‑vendor accountability.

Datwyler (Switzerland) & Egeplast (Germany): Producers emphasizing multilayer and fire‑retardant variants, addressing data‑center and indoor MDU demand where building codes and flame‑retardant specs are decisive.

Clearfield, Spur, Dura‑Line, Sanbor: Regional specialists and systems integrators delivering complementary hardware (cassettes, accessories) or targeting local public‑works contracts—key partners for last‑mile deployments.

Market concentration is meaningful but not monopolistic—our CR metrics indicate leading vendors control a significant share of the market while leaving room for regional champions and new entrants to capture niche opportunities through differentiation.

Capacity expansions (e.g., new factories inaugurated in 2025) suggest manufacturers are positioning for near‑term order wins; buyers should leverage forward offtake agreements to stabilize supply and negotiate pricing concessions tied to volume and timing.

Certifications and award recognitions de‑risk adoption for project owners; winning suppliers will combine certified product portfolios with proven installation methodologies to shorten procurement cycles.

Strategic partnerships between microduct specialists and connectivity systems firms are compressing solution cycles—operators benefit from bundled procurement but must guard against single‑vendor dependency through contract clause design.

Large-scale supply agreements between major fiber producers and network operators accelerate rollouts and can create localized capacity constraints; procurement teams should map these agreements when scheduling tenders to avoid delivery clashes.

Five structural factors will dominate decisions in 2026:

Raw material volatility: HDPE price swings materially affect margins. Recommended mitigations include multi‑tiered sourcing, multi‑year resin contracts, and product redesign to reduce material intensity where possible.

Standards and certifications: PPI and FOA requirements increasingly shape product acceptability. Early investment in certification shortens procurement cycles, especially for flame‑retardant indoor offerings.

Installation methods: Blown‑fiber systems accelerate network activation but require compatible microduct profiles and skilled installers. Operators should pilot blown systems on prioritized corridors before network‑wide rollouts.

Transport and logistics: Upstream freight and surcharge dynamics can erode landed cost advantage. Inventory buffers and near‑shoring production for key markets are defensive options.

Regulatory divergence: Building code tightening in developed markets pushes demand for certified flame‑retardant variants—suppliers lacking these SKUs risk exclusion from lucrative contracts.

Immediate (0–6 months): Update procurement specifications to reflect FOA and PPI guidance; run supplier resilience audits; secure conditional offtake contracts tied to resin‑price pass‑through clauses.

Near term (6–18 months): Execute pilots of blown‑fiber microduct systems in mixed urban/rural footprints; implement supplier scorecards and commence targeted supplier development programs.

Medium term (18–36 months): Lock in strategic capacity through partnerships or minority investments; diversify manufacturing footprint to mitigate logistics risk; roll out standardized installation training across contractors.

Strategic (36+ months): Pursue consolidation opportunities where technology assets or regional distribution provide clear synergies—use our M&A pack to model earn‑out structures and integration milestones.

This preview is intended to demonstrate the analytical depth and practical orientation of PW Consulting’s full Microducts Market study, and to outline the near‑term actions that should inform board and executive decision‑making in 2026. It surfaces the essential market trajectory, competitive dynamics, regulatory headwinds, and tactical mitigations—but intentionally omits granular regional and application‑level segmentation tables and proprietary unit‑economics that form the core of the paid study.

For procurement teams, investor diligence squads, and product‑strategy leaders preparing for accelerated fiber rollouts, the full report contains the detailed segment breakouts, downloadable financial models, and supplier scoring templates necessary to convert insight into executable plans. Contact PW Consulting or visit our Microducts Market report page to access the complete dataset and the operational tools that will underpin confident, timely decisions in 2026.

For detailed analysis of this topic, please visit the official page:Microducts Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com