The Rise of Industrial Automation Control Systems Market Demand Surges

Other |

2026-05-05 09:23:14

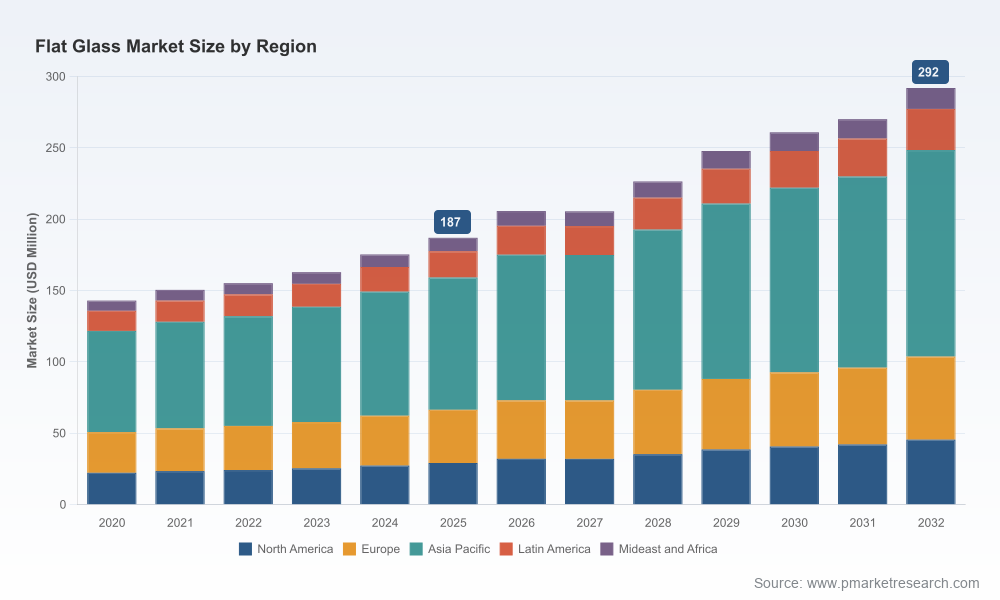

The global flat glass market is on a sustained expansion path. From a baseline measured across 2020–2025, the market rose steadily and reached a 2025 level that establishes a new planning horizon for 2026. Our forecast period (2026–2032) models a compound annual growth rate of 6.5%, with the market trajectory projecting continued recovery and product-driven expansion through 2032. For executives planning capital allocation, product roadmaps, or supply‑chain reconfiguration in 2026, this implies a market environment that rewards timely investment in high‑value product lines, decarbonized production capacity, and tighter integration with growing end-use ecosystems such as energy and high-performance construction.

Flat Glass Market

Timing capital deployment: With the market already demonstrably larger in 2025 than five years earlier and forecasted to grow meaningfully through the late 2020s, 2026 is a pivotal year to either accelerate greenfield projects or optimize existing lines for higher‑margin, low‑carbon products.

Flat Glass Market

Risk-adjusted supply strategies: Input volatility — from specialized low‑iron silica sands to soda ash and natural gas exposure — has become a recurring pressure point. Procurement strategies that combine spot‑market agility with strategic contracts will materially change margin profiles in 2026.

Flat Glass Market

Standards and certification as market gates: New and updated standards (including building and safety specifications) raise the bar for entrants and influence product mix decisions; early compliance translates to earlier access to premium building projects and multi‑pane IGU applications.

Robust market sizing and scenario modeling: Transparent methodology with baseline, upside and downside scenarios covering 2026–2032 so executives can stress‑test investments under multiple macro and energy price paths.

Actionable competitive playbooks: Vendor profiles, capability heatmaps, capacity maps and go‑to‑market vectors to inform partnerships, M&A target screening, or defensive investments.

CapEx and retrofit prioritization matrix: ROI calculations comparing new float lines, tempering upgrades, and low‑carbon technology retrofits, including payback sensitivities tied to energy costs and carbon pricing assumptions.

Supply‑chain risk dashboard: Supplier concentration, critical raw‑material exposures, logistics bottlenecks, and suggested mitigation tactics (indexing, forwards, co‑investment in raw‑material hubs).

Product and application playbooks: Profitability ladders and commercialization timelines for insulating, low‑e, ultra‑thin and solar‑grade glass solutions, with recommended product roadmaps by customer cohort.

Commercial negotiation templates: Procurement and offtake contract structures adapted to glass industry norms and energy volatility, including pragmatic clauses for price pass‑throughs and service level guarantees.

Executive briefings and investor decks: Ready‑to‑use, C-suite‑focused slide kits to accelerate board approvals or investor conversations in 2026.

The flat glass sector demonstrates a mix of global integrators, regional champions and specialty technology suppliers. Market concentration metrics indicate that the top three firms capture a meaningful share but not a dominant majority, and the top five likewise leave room for agile regional players and focused specialists. This structure creates opportunities for strategic partnerships, bolt‑on acquisitions and niche differentiation.

Legacy global manufacturers (e.g., Saint‑Gobain, AGC, NSG): These incumbents leverage scale, diversified end‑markets and R&D investments. Their strategic moves focus on low‑carbon float technology, insulating glass systems and high‑value processed glass. For 2026, anticipate continued investment in carbon reduction and differentiated coatings as gatekeepers to large architectural projects.

Coated and high‑performance specialists (e.g., Guardian, SCHOTT, Central Glass): Emphasis here is on engineered coatings, high‑transmission variants and specialty thin glass. These players are advantaged where performance pays — premium façade contracts, specialty industrial uses, and advanced optoelectronics.

Regionally dominant producers (e.g., Şişecam, Vitro, Xinyi, Fuyao, CSG, Taiwan Glass): Regional manufacturing density, proximity to construction booms, and integrated supply chains make these firms agile partners for local OEMs and distributors. Their 2026 strategies will likely focus on capturing retrofit demand and expanding processing capacity for value‑added products.

Specialty fabricators and glass processors (e.g., Cardinal, Pittsburgh Glass Works): These companies are critical nodes in the value chain, bringing fabrication, finishing and aftermarket services. For buyers, partnering with fabricators for co‑development shortens time‑to‑market for complex IGUs and automotive glazing solutions.

Decarbonization as a commercial differentiator: Low‑carbon production lines and product carbon footprint declarations are moving from compliance nicety to procurement prerequisite. Several manufacturers now publish embodied carbon metrics for their lines; buyers increasingly price and select suppliers based on those disclosures.

Raw‑material tightness and price signaling: The emergence of specialized low‑iron silica sand pricing and continuing soda‑ash and energy cost volatility materially affect ultra‑thin and solar‑grade economics. In 2026, upstream sourcing strategies and co‑investment in raw‑material security will be decisive competitive advantages.

Standards and safety constraints: Recent updates to dimensional and optical standards, and the ongoing limitations posed by safety glazing certifications for very thin glass in multi‑pane units, shape product timing and certification roadmaps. Meeting these standards early de‑risks sales cycles into large construction and automotive clients.

Application convergence: Solar modules, high‑performance façades and advanced automotive glazing are converging requirements around optical clarity, low iron content and robust coatings. Cross‑industry partnerships (glass makers with module makers, façade engineers and OEMs) present outsized upside in 2026.

Recalibrate product portfolios: Prioritize low‑carbon and high‑value coated products for new capacity and retrofits. Deprioritize commodity lines with thin margins unless they provide strategic market access.

Secure raw‑material supply with layered contracts: Use a mix of long‑term agreements, indexed buyouts and strategic inventory hubs to protect against silica and soda‑ash swings while preserving cash flow flexibility.

Pursue targeted M&A and partnerships: Look for bolt‑ons that add coatings capability, specialty fabrication or proximity to growing construction markets. The current concentration profile favors strategic consolidation at the regional level.

Invest in certification and standards leadership: Engage with standards bodies and invest in testing/certification early to remove technical barriers and accelerate procurement approvals with large specifiers.

Hedge energy exposure and explore alternative fuels: Given the sensitivity of glass manufacturing to natural gas and electricity prices, invest in energy efficiency, fuel switching and on‑site renewables where economically viable.

Industry forums and trade shows scheduled throughout 2026 are high‑value windows for competitor scouting, technology sourcing and customer engagement. Events in North America, Europe and the Middle East aggregate manufacturers, fabricators and suppliers and are ideal venues for validating assumptions, launching pilots, and negotiating supply arrangements.

Our approach bridges rigorous quantitative forecasting (transparent models built on 2020–2025 history and 2026 starting conditions) with hands‑on commercial tools that executives can execute immediately. The deliverable is not just a market map but an operational playbook: slide decks for boards, Excel models for finance teams, procurement templates for supply teams, and a prioritized investment scoreboard for strategy groups.

This article intentionally highlights the strategic contours and operational levers without publishing the detailed, segment‑level forecasts, regional allocations and price-by-product matrices that discipline 2026 decisions. Those granular datasets — including the detailed segment breakdowns, scenario tables and supplier scorecards — are available in the full PW Consulting Flat Glass Market report. For teams preparing board materials, investment memos or procurement strategies for 2026, the full report contains the precise inputs and templates you will need to convert insights into executable plans.

For detailed analysis of this topic, please visit the official page:Flat Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com