Acoustic Panel Market 2026 Preview: Strategic Insights for Decision‑Makers

Executive snapshot

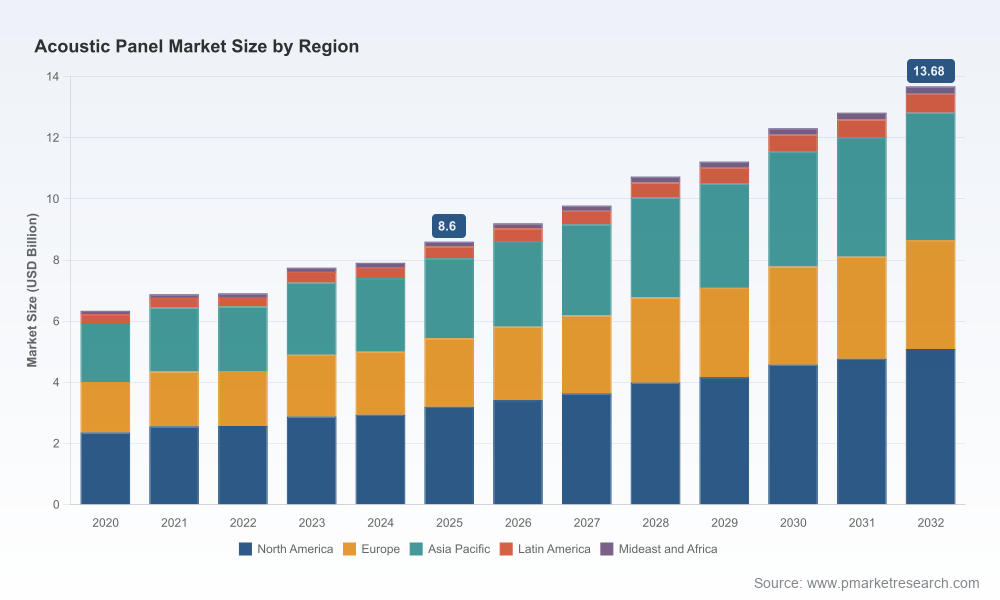

As PW Consulting’s senior strategy adviser and chief industry analyst, I present a strategic preview of our comprehensive Acoustic Panel Market research. Built on a 2025 base year and a five‑year historical window (2020–2025), the study projects the market through 2032. At an expected compound annual growth rate (CAGR) of 6.7% for the 2026–2032 forecast horizon, the industry evolves from an estimated USD 8.6 Billion in 2025 toward roughly USD 13.7 Billion by 2032. This trajectory — and the forces shaping it — will be decisive for corporate capital allocation, product roadmaps, procurement strategies, and merger & acquisition (M&A) plays in 2026.

Acoustic Panel Market

Why this research matters for 2026 decision cycles

- Timing of strategic moves: With demand momentum accelerating into the late 2020s, 2026 is a hinge year for committing to capacity, supply agreements, and vertical integration. Decisions made this year will lock in cost structures and market reach for the next six to eight years.

- Regulatory and sustainability inflection: End‑user and building‑code requirements are tightening around low‑emitting materials and product transparency. Early compliance and differentiated sustainability claims can translate directly into specification wins with major architects and owners.

- Fragmentation creates opportunity: The market remains structurally fragmented; concentration among the top three and top five players is modest. That fragmentation lowers barriers for focused, well‑executed entrants or roll‑up strategies.

- Technology and material evolution: New binders, recycled feedstocks and acoustical constructions are changing cost curves and product positioning — which will affect margins and distribution models.

Market trajectory and what the numbers tell us (high level)

The market’s historical expansion from roughly USD 6.3 Billion in 2020 to USD 8.6 Billion in 2025 demonstrates steady recovery and structural demand for acoustic solutions across built environments. Our forecast shows continued momentum into 2026 and beyond, reaching approximately USD 9.2 Billion in 2026 and approaching USD 13.7 Billion by 2032. This pace — underpinned by a 6.7% CAGR across the forecast period — reflects a mix of retrofit activity, new commercial and institutional construction, and an increasing share of specification driven by acoustic, aesthetic, and sustainability requirements.

Acoustic Panel Market

Key structural dynamics shaping supply and demand

- Specification-led demand: Architects, acoustic consultants and corporate real‑estate teams are prioritizing measurable acoustic performance and material health certifications. Products that combine verifiable acoustic metrics with low‑emission profiles are winning larger project scopes.

- Material substitution and sourcing pressure: Polyesters (including recycled PET), mineral fiber, wood‑based constructs and advanced fiberglass products each compete on acoustic performance, cost, circularity credentials and fire performance. Volatility in recycled feedstock availability and energy costs can compress margins or create arbitrage across material classes.

- Regulatory tailwinds: Standards and test certifications for VOCs and material disclosure are becoming procurement gatekeepers. Compliance with recognized standards is rapidly shifting from “nice to have” to “must have” in major tenders.

- Channel and specification complexity: The purchase path is multifaceted — from direct supplier to fabricator relationships to distribution networks serving repeat commercial buyers — demanding tailored commercial models.

What our full report delivers (practical, decision‑ready content)

This study is designed to be actionable for executives, strategy teams, product leaders and corporate development professionals. Highlights of the deliverables include:

Acoustic Panel Market

- Robust market sizing and a transparent forecasting methodology using 2025 as the base year, with historic analysis (2020–2025) and forward scenarios to 2032.

- Scenario analysis that stress‑tests volumes and pricing under alternative macroeconomic, raw‑material and regulatory assumptions.

- Go‑to‑market playbooks tailored to manufacturers, distributors and material suppliers — including channel economics, tender strategies and specification tactics.

- Supplier and value‑chain maps that identify strategic pinch points for feedstocks, manufacturing capacity and finishing services.

- Commercial diligence modules for M&A and investment teams: synergy estimates, integration risks, and high‑level valuation levers for targets.

- Regulatory and sustainability impact analysis, including implications of low‑emission certifications and material disclosure frameworks on procurement and pricing.

- Practical KPIs and an implementation checklist for procurement, R&D and product marketing teams to translate insights into 12–18 month actions.

To preserve competitive value, granular segment splits and project‑level contract data are omitted here — these are available within the full report and accompanying data workbook for subscribers and clients.

Competitive landscape — what to watch in 2026

The market combines established industrial players with specialized niche providers. Overall concentration is relatively low, with the largest three firms accounting for a modest share of total revenue and the top five still holding limited dominance — an environment that favors focused innovation and selective consolidation.

- Large incumbent manufacturers: Established companies with broad portfolios and distribution networks continue to set performance and compliance benchmarks. Expect continued investment in mineral fiber, wood‑wool offerings, and scalable ceiling portfolios tailored for large projects.

- Specialists and differentiation leaders: Firms that emphasize sustainability credentials, novel binders or design‑forward aesthetics are carving higher‑margin niches. Their proximity to architects and designers can shift specification outcomes in targeted accounts.

- Notable company examples: Leading suppliers include manufacturers known for premium acoustical products and modular solutions; firms offering mineral fiber ceiling and wall panels with high acoustic ratings and climate performance; producers of PET‑based panels with carbon or recycled claims; and specialist industrial noise solutions for harsh environments. Recent industry activity illustrates these dynamics: several suppliers have launched new low‑emission or recycled‑content products and certifications that materially affect specification choices.

Recent developments that matter for procurement and product strategy

- Product introductions with validated low‑emission performance and Red List–free claims are shifting specification thresholds. Early movers that can demonstrate compliance with established indoor‑air and material transparency standards enjoy a pricing premium on major tenders.

- Manufacturers are increasingly publicizing recycled feedstocks and carbon‑neutral product claims. These claims accelerate buyer preference among sustainability‑focused owners and design teams.

- Innovation in binders and manufacturing processes — including formaldehyde‑free adhesives and natural binder technologies — is reducing health exposure risk and unlocking new product positioning for healthcare, education and corporate interiors.

Strategic playbook for 2026

For senior leaders planning for 2026, our recommendations are practical and prioritized:

- Audit specifications and certifications now: Map your product lines against the certifications expected by target customers and invest in the minimum viable certification set required to win projects in your priority segments.

- Lock in feedstock and capacity flexibility: Negotiate blended procurement contracts for recycled polyester and mineral inputs, and evaluate toll‑manufacturing or contract finishing to manage cyclical demand swings without heavy capital outlay.

- Pursue targeted M&A or partnership for capability gaps: Acquire or partner to add differentiated acoustic performance, low‑emission binders, or design aesthetics — bolt‑on deals can be more accretive than greenfield expansion in 2026 market conditions.

- Refine go‑to‑market by buyer persona: Build separate value propositions for specifiers (architects and consultants), end‑users (owners and facility managers) and distributors. Demonstrable performance data and case studies accelerate specification conversion.

- Price for specification value, not commodity: Establish price tiers tied to measurable acoustic metrics, environmental credentials and lead‑time guarantees to avoid margin erosion.

How to use this report in your 2026 planning cycle

Use the research as a decision toolkit: inform capital budgets, prioritize R&D and certification spend, prepare integration planning for M&A targets, and align commercial incentives with specifier behavior. For procurement organizations, the scenario analyses provide actionable hedging strategies for feedstock risk and capacity utilization. For product and brand leaders, the product benchmarking and case studies show how to translate technical advantages into specification wins.

Conclusion — the strategic inflection is now

The acoustic panel industry presents a classic combination of structural growth, shifting material science, and rising regulatory and buyer expectations. With the market poised to expand meaningfully from its 2025 baseline under a 6.7% CAGR through 2032, 2026 is a pivotal year to set strategic positions that capture the higher‑value opportunities. Our full PW Consulting study delivers the granular, transaction‑grade analysis and implementation roadmaps that leaders and investors need to act with conviction. For access to the detailed segment analytics, regional and application splits, and full company profiles and financial benchmarks, please obtain the complete report and datasets from PW Consulting.

For detailed analysis of this topic, please visit the official page:Acoustic Panel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com