What Is Driving Demand in Chemical Dust Suppressants Market for Industrial Safety?

Networking |

2026-04-27 11:26:37

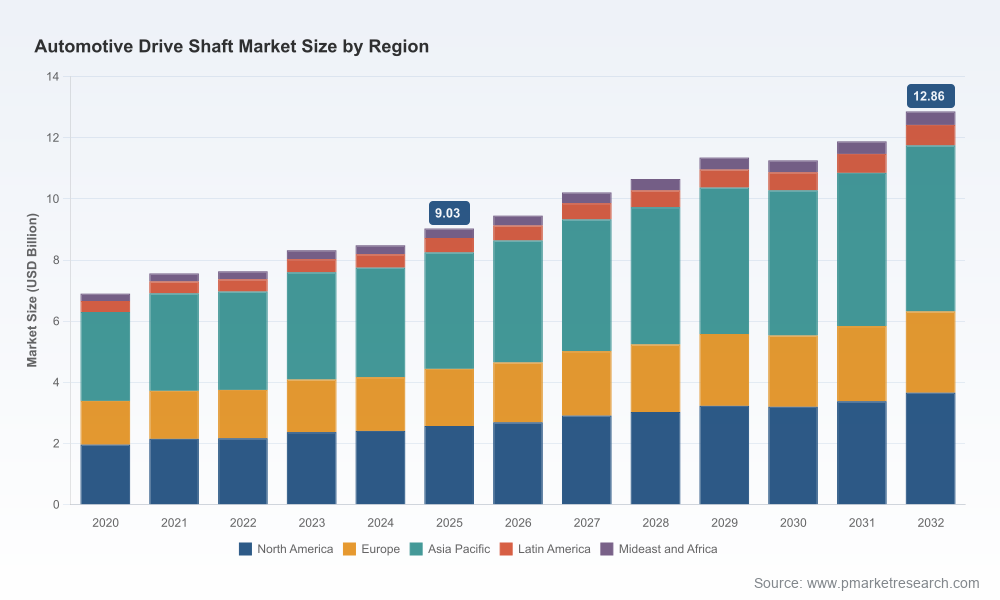

As OEMs and suppliers enter a decisive inflection point for drivetrain architecture, the global automotive drive shaft market presents a clear yet nuanced growth opportunity. Our PW Consulting analysis uses 2025 as the base year and tracks historical performance from 2020–2025, projecting the market through 2032. The market expanded from roughly USD 6.9 billion in 2020 to about USD 9.03 billion in 2025, and current forecasts anticipate continued expansion to a projected market size north of USD 12 billion by 2032, implying a mid-single-digit compound annual growth rate (CAGR) over the forecast period. These headline dynamics reflect a market shaped by propulsion transition, new-material adoption, and persistent cost pressures — forces that will directly influence capital allocation, product roadmaps, and M&A activity in 2026.

Automotive Drive Shaft Market

Portfolio prioritization: Product teams must decide which driveline architectures to accelerate (telescopic, hollow, hybrid-compatible) and which to mothball. The next 18 months are critical: supplier selection and first-mover product launches will determine content wins on next-generation vehicle platforms.

Automotive Drive Shaft Market

Materials strategy and cost resilience: While composites and lightweight aluminum are being specified more frequently by EV programs to meet efficiency targets, steel remains the backbone of production due to its strength and supply-chain maturity. Coupled with documented raw-material price volatility (which can add material cost variance in the low double-digit range annually), buyers and suppliers must embed materials flexibility and hedging into procurement and design cycles.

Automotive Drive Shaft Market

Supply-chain footprint and industrial economics: The market structure remains relatively fragmented (three- to five-player concentration metrics indicate room for consolidation and niche leadership). For corporate development teams, this fragmentation creates both acquisition opportunities and risks as larger OEM-aligned suppliers jockey for system-level dominance.

Technology compatibility and certification: With propulsion-agnostic driveline systems emerging, R&D and validation calendars must be synchronized with OEM platform timelines. Certification and reliability testing regimes for high-angle CVs, telescopic joints, and e-propulsion interface components will be gating factors for 2026 program awards.

Proven market-sizing and growth model with base-year calibration and scenario runs through 2032, supporting conservative, base, and accelerated demand paths.

Demand-driver mapping linking vehicle electrification rates, regional production footprints, and vehicle mix shifts to drive-shaft content trajectories.

Cost-to-serve and component-level cost modeling that isolates material, processing, and logistics levers — enabling 5–10% cost-to-complete planning for supplier negotiations.

Technology roadmaps and time-to-certification estimates for hollow shafts, telescopic variants, high-angle CV joints, and composite-reinforced designs.

Competitive playbooks for incumbent and challenger suppliers, including capability heatmaps, likely move sequences, and M&A candidate shortlists consistent with consolidation economics.

Practical implementation tools: supplier selection scorecards, risk-heatmap templates, and a 12–18 month tactical rollout plan aligned to procurement cycles.

The competitive topology is a mix of global system suppliers and specialized driveline component manufacturers. Key strategic behaviors are already visible among leading players:

GKN Automotive (Coventry, UK) continues to position itself as a propulsion-agnostic systems provider, emphasizing sideshafts, CV joints, and propeller shafts that can be integrated across ICE, hybrid and EV platforms. Their emphasis on system modularity reduces OEM integration friction and creates a durable relevance regardless of powertrain mix.

Nexteer Automotive (Auburn Hills, MI) is pursuing premium driveline technologies, with recent product introductions targeted at EVs and performance packaging. Their telescopic and high-angle CV competencies place them well for luxury and performance segments where NVH and dynamic response command price premiums.

Dana Incorporated (Maumee, OH) has been translating wins in integrated drivetrain solutions into momentum on electrified programs. Their combined systems approach — from axles to e-propulsion modules — positions them to win higher content-per-vehicle and to offer OEMs cleaner integration pathways.

American Axle & Manufacturing / Dauch Corporation (Detroit) continues to leverage deep metal-forming and driveline manufacture for global OEMs. Recent corporate combinations aim at consolidating technology stacks and scale advantages to maintain competitiveness in tender processes.

Hyundai WIA (Seoul) and Neapco (Quakertown) represent different strategic postures: one leveraging OEM group alignment and vertical scope; the other focusing on OEM and aftermarket breadth. Both remain active in productization and aftermarket penetration strategies.

Recent developments signal two tightening trends: incumbents are expanding EV-capable portfolios, and strategic combinations are being pursued to pool technology assets and scale production. Examples include a multi-product EV driveline platform launch and corporate combinations aimed at integrating driveline technologies into broader mobility systems. For clients, this pattern means accelerated timelines for competitive response and an increased value on IP and system-level integration capabilities.

Regulatory push and OEM specifications are catalyzing wider use of aluminum and carbon-fiber composites on EV programs to meet efficiency and emissions objectives. These choices influence not just unit cost but tooling, joining methods, and life-cycle repairability.

Despite composite interest, steel still dominates for many applications because of its mechanical properties and existing manufacturing scale. A pragmatic materials strategy for 2026 is one of graded substitution — selectively deploying composites where weight-to-cost payback is clear and retaining steel where durability or cost certainty is paramount.

Raw material price swings remain a salient operational risk. Historical industry analysis shows that annual cost volatility for key materials can reach low- to mid-double-digit percentages, which rapidly erodes margin for suppliers operating on fixed long-term OEM contracts. Active hedging, multi-sourcing, and pass-through mechanisms are now core procurement imperatives.

90-day: Run a portfolio heat-map to identify which driveline products are strategically core, which are competitive differentiators, and which should be licensed or divested. Align R&D spend to the top two prioritized product families.

6–12 months: Execute cost-to-serve audits for top OEM customers; implement material-flex design guidelines to allow dual-sourcing between steel and aluminum/composite suppliers.

6–12 months: Launch a limited pilot for hollow-shaft or telescopic-shaft lightweight variants with one lead OEM program to establish a certification baseline and capture first-mover learning.

12–18 months: Establish M&A screening criteria targeting technology-rich niche players in regions where scale or localization is a procurement advantage; prioritize targets that close capability gaps (e.g., CV joint NVH, telescopic reliability, e-propulsion interfaces).

Ongoing: Institutionalize raw-material hedging and supplier scorecards that incorporate volatility metrics, lead times, and secondary-sourcing exposure.

18–36 months: Invest in digital-twin and fleet-telemetry pilots to quantify real-world failure modes and service-life economics — an advantage for aftermarket and warranty-cost reduction strategies.

For executives making resource-allocation and M&A choices in 2026, the right blend of market context, cost analytics, and competitor intelligence is non-negotiable. Our research provides that blend: calibrated market sizing from 2020–2025 with forward scenarios to 2032, a pragmatic assessment of materials and regulatory headwinds, and a tactical playbook that translates insights into executable moves. The analysis intentionally demonstrates rigor while reserving detailed proprietary splits and client-ready models to the full report — a design choice that ensures decision-makers receive both strategic clarity and actionable next steps. To deploy these insights directly into your 2026 planning cycle, PW Consulting’s full report and bespoke advisory services provide the proprietary segmentation, supplier scorecards, and deal-sourcing lists required for confident execution.

For detailed analysis of this topic, please visit the official page:Automotive Drive Shaft Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com