Aesthetic Cosmetic Lasers Market: Size, Share, and Future Growth

Other |

2026-06-01 13:51:32

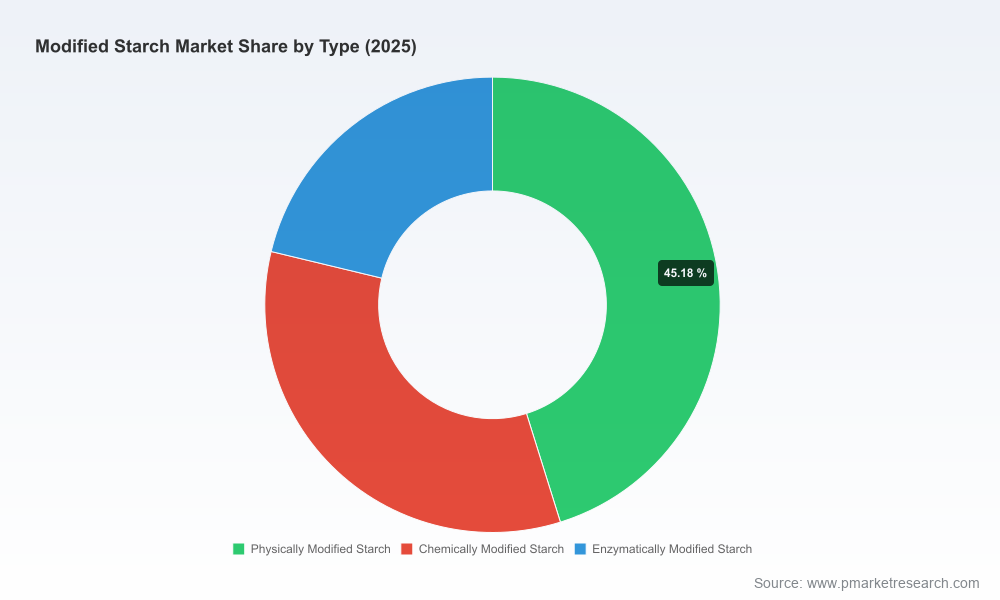

As companies finalize 2026 strategies, the modified starch market presents a classic test of operational resilience and product-led differentiation. Our PW Consulting Modified Starch Market study (base year 2025; historical window 2020–2025; forecast 2026–2032) highlights a steady expansion of the addressable market — rising from roughly USD 10.5 Billion in 2020 to USD 13.7 Billion in 2025 and projected to reach the mid‑teens by the end of the forecast horizon (compound annual growth of about 3.5%). That topline trajectory masks critical asymmetries across raw-material exposures, regulatory regimes, and routes to value capture that will determine winners in 2026 and beyond.

Modified Starch Market

Timing: 2026 is the first full year after several trade, tariff, and labeling changes that have materially altered cross‑border flows and product specifications—making near-term sourcing and pricing choices high‑stakes.

Modified Starch Market

Cost and pass-through: Rapid tapioca and starch feedstock movements in late‑2025 demand fresh procurement and hedging tactics to protect margins without eroding customer relationships.

Modified Starch Market

Product strategy: Clean‑label and enzymatic routes are moving from R&D conversation to commercial imperatives following regulatory guidance and customer preferences.

M&A and capacity: Moderate market concentration (cr3 ≈ 35%, cr5 ≈ 45%) suggests opportunity for targeted consolidation and bolt‑on acquisitions by specialty players and financial sponsors.

Demand drivers remain broad-based. Food & beverage reformulation, industrial adhesives, paper and packaging, and selected speciality applications continue to underpin growth. However, the pace and quality of demand vary by end‑use and by the label/convenience premium customers are willing to pay.

Raw‑material volatility is a near‑term operational risk. The period into early‑2026 saw a continuous price uptick and tightening supply for key feedstocks—tapioca in particular experienced meaningful upward pressure. Similarly, wide ranges in export pricing for potato starch in 2025 highlight supplier pricing dispersion. Procurement teams must retool to account for this elevated baseline.

Regulatory change is an activation lever. EU tariff code refinements and 2025 updates to FDA labeling guidance have increased demand for starches that avoid complex chemical declarations or E‑numbers—accelerating interest in “label‑friendly” chemistry and process routes.

Trade policy reshuffles trade flows. US tariff updates on modified starch imports in 2025 created immediate price effects and forced buyers to reconsider sourcing geographies and inventory strategies.

Bottom‑up capacity and shipment mapping across primary production sites and major converters.

Primary interviews with procurement leads, formulators, and trade intermediaries to validate pass‑through and substitution elasticities.

Price/volume scenarios reflecting feedstock shocks, tariff permutations, and regulatory adoption curves.

Cross‑checking against macro consumption trends in key end‑use verticals and historical growth over 2020–2025 to establish a 2026 baseline and 2026–2032 trajectories.

Granular revenue build by region, product type and application with sensitivity ranges — essential for channel segmentation and investment prioritization (note: detailed splits are reserved for the full report).

Company scorecards and a competitive positioning matrix with capability maps, margin proxies, and accessibility to specialty grades.

Supply‑chain risk heatmaps, including feedstock exposure, single‑source dependencies, and logistics chokepoints by corridor.

Raw‑material price‑pass‑through models and recommended contract structures (fixed, indexed, hybrid) under three stress scenarios.

Regulatory and tariff playbook summarizing HS code updates, labeling implications, and compliance costs per geography.

10 industry playbooks (CPG, paper, adhesives, textiles, pharma, animal feed) with targeted product and commercial tactics for 2026.

M&A target shortlist and valuation framework focused on specialty producers, regional champions, and technology owners.

The market exhibits a hybrid structure: several global leaders with broad portfolios and scale, alongside a broad base of regional and specialty producers. That mix creates space for both price competition in commodity grades and premium capture in differentiated, label‑friendly, or application‑specific solutions.

Cargill — an innovation‑led platform. Cargill’s recent rollouts (e.g., dent‑corn modified starch variants and pectin replacement solutions) underscore its R&D to commercialization pipeline. Buyers should view Cargill as a strategic partner for product reformulation and scale supply, but also expect a premium for specialty blended solutions.

Ingredion — food‑market mastery. Ingredion’s depth in food‑grade modified starches and industrial grades makes it a go‑to for formulators seeking texturizing and stabilization expertise linked to consumer perceptions. Their capabilities favor customers prioritizing clean‑label transitions.

Roquette — breadth of feedstock and variants. Roquette’s multi‑source approach (corn, wheat, potato, tapioca, pea) and extensive variant library mean rapid prototyping and cross‑application reuse — an advantage when supply shifts force rapid substitution.

Tate & Lyle — specialty and clean label focus. Tate & Lyle’s positioning on clean‑label and functional derivatives aligns closely with CPG customers targeting ingredient transparency.

Regional specialists (Premier Starch, Angel Starch, Jay Dinesh, Vinayak, SMS, Grain Processing, Global Bio‑Chem, AEBE, SPAC) — cost and niche innovation. These players provide lower‑cost or highly tailored solutions, particularly in Asia and emerging markets. SMS’s recent trade show launches and awards highlight the rising commercial quality of tapioca‑based specialty starches.

Lock in upstream optionality. Negotiate hybrid contracts with key tapioca and potato suppliers (blend floor/ceiling pricing) and build shorter, high‑frequency contracts with alternative suppliers to manage supply shocks.

Prioritize “label‑friendly” reformulations now. With FDA labeling shifts and EU regulatory refinements, first movers can claim shelf‑space and margin premiums; delay increases reformulation cost and time pressure.

Differentiate via application engineering. Invest modestly in co‑development teams focused on high‑margin verticals (specialty sauces, paper adhesives, pharma excipients) where unique functional performance outvalues raw cost.

Use M&A tactically. Target small specialty producers and regional feedstock integrators to acquire product portfolios, secure capacity, or obtain route‑to‑market in constrained geographies.

Revise price governance. Establish transparent pass‑through clauses tied to monitored feedstock indices and embed automatic review triggers tied to tariff or regulatory changes.

Accelerate traceability and sustainability narratives. Sustainability is increasingly a procurement filter—buyers will pay for traceable, lower‑impact starches sourced under verifiable stewardship.

Valuation premiums are clustering around: (1) clean‑label and enzymatic modification IP, (2) specialty tapioca supply chains with export capability, and (3) formulatory expertise for high‑value applications. Financial sponsors should anticipate modest scale benefits from roll‑ups but must price in integration risks tied to feedstock concentration and regulatory variability.

Customized scenario models that quantify margin impact under alternative feedstock price and tariff outcomes.

Due diligence packs for M&A targets with supplier maps, technical capability audits, and integration playbooks.

Commercial playbooks for formulators and CPGs to capture label‑premium pricing without sacrificing shelf stability.

Procurement transformation programs including indexed contract templates and a supplier diversification roadmap.

Our report is a practical instrument for 2026 decision‑makers: it equips procurement leaders, product managers, and corporate strategists with the scenario tools, supplier intelligence, and route‑to‑value playbooks needed to convert a modest market CAGR (~3.5% through 2032) into differentiated growth. For detailed regional, product and application splits, company market shares, and the full set of operational templates, access the complete PW Consulting Modified Starch Market study and accompanying toolkits.

For detailed analysis of this topic, please visit the official page:Modified Starch Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com