Footwear Market 2026: Strategic Imperatives from PW Consulting’s Latest Industry Readout

Executive snapshot

The global footwear market stands at a pivotal inflection point as companies enter 2026. After a five-year historical window of steady expansion, PW Consulting’s 2026-readiness analysis positions the industry on a trajectory from a 2025 aggregate market size of USD 483.0 Billion toward a mid‑range scenario of roughly USD 663.9 Billion by 2032 — reflecting a 2026–2032 compound annual growth rate of approximately 4.7%. That headline momentum masks profound structural shifts: rising policy friction, accelerated reshoring and automation, shifting consumer priorities around performance and sustainability, and a competitive field that blends global megabrands with specialized domestic manufacturers.

Footwear Market

Why this research matters for 2026 decision-making

- Policy and tariff volatility has moved from tail risk to operational baseline. Average U.S. footwear tariffs and targeted high-duty lines materially change landed-cost calculus, affecting sourcing, pricing, and inventory strategies.

- Sustainability and traceability are tightening from consumer preference into compliance: new EU ecodesign rules and required digital product passports are creating non‑optional upstream data obligations by 2027.

- Scale and specialization are co‑existing. The market’s competitive topology shows concentration at the top, but sizeable opportunity persists for targeted players that combine technical differentiation (performance, safety, orthopedics) with supply‑chain agility.

- Capital allocation in 2026 must be dual‑track: invest in near‑term resilience (nearshoring, contract manufacturing partnerships, tariff mitigation) and medium‑term value (product technical IP, sustainability compliance, software/data capabilities).

Market trajectory: what the macro numbers reveal — and what they conceal

The aggregate figures in our report make one point clear: demand for footwear as a category will expand on a mid-single digit cadence through the decade. That topology supports continued capital deployment across product innovation, distribution and manufacturing. Yet the headline CAGR masks diverging sub‑curves — premium performance and sustainable offerings capture outsized spending elasticity, while commoditized segments face margin pressure from tariff and input‑cost passthroughs. For strategic planners, the lesson is binary: don’t treat the market as a single, homogeneous growth engine. Investment choices should be segment‑aware, even when public summaries only present the topline.

Footwear Market

Competitive dynamics and where advantage is being built

The competitive set is best read as concentric rings. Global athletic and lifestyle leaders continue to invest in direct‑to‑consumer ecosystems, proprietary materials and platformized innovation. At the same time, a second tier of brands is consolidating technical niches (work, outdoor, military, orthopedic) that require different go‑to‑market and manufacturing models. Selected insights from the market scan:

Footwear Market

- Nike and adidas remain reflexive innovators: platform technology, brand ecosystems, and global distribution give them leverage on margin and scale, but they face the same supply‑chain rebalancing pressures as peers.

- Large comfort and value brands (Skechers, Crocs) are converting broad distribution into expanded lifestyle relevance; product simplicity lets them iterate quickly while balancing cost pressure.

- Outdoor, work and safety specialists (Timberland, Red Wing, Wolverine, Danner, Belleville) are consolidating supply resilience and certifications — a clear defensive response to tariffs and procurement cyclicality that benefits B2B and institutional buyers.

- Innovators and domestic champions (Made Plus, McRae Industries) exemplify a separate playbook: high‑margin specialty products built on performance or compliance (military Berry Amendment work), and growing alliances with machinery and automation providers.

- European comfort and premium brands (Clarks, ECCO, Geox, Rieker) leverage product engineering and premium positioning; their exposure to European sustainability standards forces early investments in traceability systems.

Recent industry moves that change the 2026 playbook

- Manufacturing and machinery alliances: the addition of tooling and automation suppliers into national manufacturing associations signals an acceleration of automation-enabled reshoring. Expect feasibility windows for domestic capacity to close in 2026 as know‑how and capital coalesce.

- Supply‑chain membership and capacity expansion announcements reflect a tactical response to tariff pressure and procurement decentralization. These moves reduce single‑node risk and shorten lead times for strategic assortments.

- Trade shows and exhibitions in 2026 showcased sustainable materials, sculptural design trends, and minimalist performance silhouettes — a real‑time barometer of buyer priorities for the coming product cycles.

Regulatory and trade dynamics — constraints that become levers

Policy is rapidly shifting from background noise to direct value driver. Average U.S. footwear tariffs and certain high‑duty lines impose a significant cost floor for import‑dependent models, and total duties paid at trade fences are now a multi‑billion‑dollar topic for the industry. In parallel, European ecodesign mandates introduce digital product passports and traceability obligations that will be enforced from 2027 — effectively turning material and process transparency into pre‑sale requirements for European distribution. For 2026 planners, the critical step is not merely compliance budgeting; it is embedding policy scenarios into product roadmaps and sourcing decisions so that regulation becomes a source of competitive differentiation rather than purely a cost center.

Operational playbook for 2026 — prioritized actions

- Recalibrate sourcing strategy: run dual scenarios quantifying near‑term tariff exposure versus nearshoring capex and unit economics. For critical product lines, cultivate a “two‑node” supply base to flex capacity quickly when duties or logistics spikes occur.

- Accelerate traceability and data foundations: implement the minimum viable Digital Product Passport compliance pathways now. Early adopters will reduce time‑to‑market friction in the EU and gain trust premiums with sustainability‑driven buyers.

- Targeted automation investment: prioritize cells that compress labor intensity and increase mix flexibility (stitching, sole attachment, last‑handling). Machinery partnerships are becoming a pragmatic route to scale domestic capacity without prohibitive headcount expansion.

- SKU rationalization and assortment science: double down on demand‑driven assortment optimization to reduce inventory drag while protecting high‑margin, high‑elasticity items with rapid replenishment pathways.

- Strategic M&A and alliance playbooks: prioritize acquisitions that add technical IP (materials, midsoles), domestic manufacturing footprints, or traceability technology — not merely revenue scale.

What PW Consulting’s full report delivers — the practical toolkit

Our full Footwear Market study goes beyond headline forecasting to provide operationally actionable intelligence tailored to executive decision cycles in 2026. Highlights include:

- Proprietary topline model and scenario suite: baseline, tariff‑stress and accelerated‑sustainability pathways through 2032, with sensitivity levers for input costs, channel shifts and policy shocks.

- Competitor deep dives and capability maps: go‑to‑market strategies, manufacturing footprints, R&D investments and partnership profiles for the leading global and specialist players.

- Supply‑chain heatmaps and supplier scorecards: visibility on nearshore/onshore capacity, critical machinery suppliers, and digital traceability readiness.

- Investment playbooks: prioritized capex roadmaps for automation, traceability, and sustainability programs, with break‑even horizons under multiple demand scenarios.

- M&A screening models and valuation ranges: targeted lists of strategic acquisitions and partnerships that unlock manufacturing resilience or technical differentiation for 2026 buyers.

- Commercial playbooks: channel strategies, pricing levers, and DTC‑vs‑wholesale decision matrices aligned to the observed consumer shifts in outdoor and lifestyle spending.

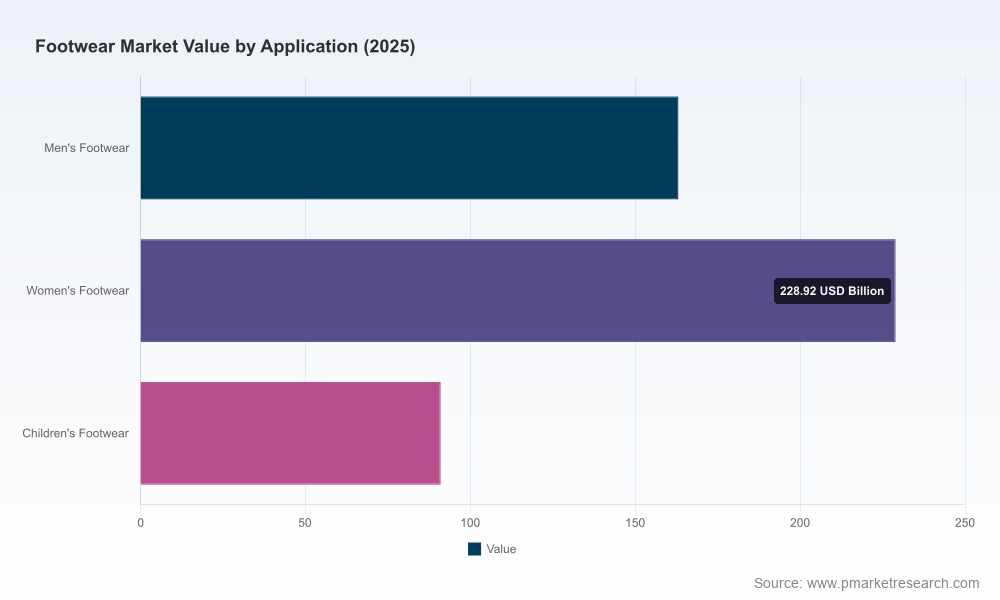

Note: our public summary intentionally omits the granular regional and application splits that are essential to precise buy/have/sell decisions. Those detailed matrices, unit economics and regional demand ladders are included exclusively in the full report and dataset.

How to convert insight into 90‑day wins

- Run a tariff‑sensitivity sprint: produce a prioritized SKU list where nearshoring or premiumization yields immediate margin protection.

- Start a Digital Product Passport pilot for a single product family destined for EU channels — validate data flows, supplier cooperation and customer labeling in 60–90 days.

- Engage one automation partner for a rapid feasibility study to convert an existing offshore line into a hybrid nearshore cell; use trade‑show supplier introductions to accelerate procurement timing.

- Launch a small M&A diligence on an adjacently located technical manufacturer or materials supplier that provides immediate onshore capacity or IP.

Closing perspective: positioning for asymmetric advantage in 2026

As the market transitions from global arbitrage to a more fragmented and policy‑sensitive regime, the companies that will outperform are those that treat 2026 as a year of architectural decisions rather than tactical fixes. That means embedding compliance and traceability into product design, prioritizing investments that shift the supply‑cost curve (automation, nearshoring partnerships), and harvesting brand premium through technical differentiation and sustainability authenticity.

PW Consulting’s full Footwear Market report provides the granular segmentation, datasets and playbooks required to convert these strategic imperatives into executable programs. For executives prioritizing resource allocation and M&A through 2026, the full intelligence package is the difference between reacting to policy and turning it into competitive advantage. Visit our report page to access the complete datasets, scenario models and bespoke consulting offers that are designed to operationalize the opportunities outlined here.

For detailed analysis of this topic, please visit the official page:Footwear Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com