Solder Resist Ink Market: Strategic Primer for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present this market primer to orient executives, M&A teams, and product leaders preparing for strategic moves in 2026. Our latest market study—anchored on a 2025 base year and spanning historical performance (2020–2025) with a forecast horizon to 2032—synthesizes commercial, regulatory, and technology dynamics that will shape competitive advantage in solder resist inks and masks. The narrative below surfaces high-impact implications and tactical levers without disclosing the detailed segment-level intelligence reserved for the full report.

Solder Resist Ink Market

Market Trajectory: A Clear Growth Arc

The solder resist ink market has moved from a mid-cycle recovery into a structurally expanding phase. On a macro scale, global revenue expanded from the low hundreds of millions (USD, million-unit reporting) in 2020 to a solid base year of 2025. Our forecast projects continued expansion through 2032, driven by sustainable product innovation, packaging complexity in electronics, and regulatory-driven reformulation demand. The modeled compound annual growth rate for the forecast window is 6.81%—a healthy pace that signals both steady demand and opportunities for margin-enhancing product differentiation.

Solder Resist Ink Market

Two headline takeaways for boards and strategy teams:

Solder Resist Ink Market

- Growth is predictable enough to underpin multi-year capacity and R&D investments—but nuanced enough that capital should be staged and tied to regulatory and end-market triggers.

- Market concentration is meaningfully elevated: the top tier incumbents control the lion’s share of revenues, creating both barriers to entry and opportunities for targeted disruption through specialized formulations or service models.

Why 2026 Is a Pivotal Year

2026 is the inflection point for several reasons. First, OEM and tier-one electronics manufacturers are accelerating substance-reduction rules and sustainability procurement clauses that impact formulation acceptance windows. Second, supply-chain volatility that began in the earlier part of the decade has normalized into recurring raw-material premium events—pushing buyers to prefer partners with vertically integrated supply security or validated multi-source chemistries. Third, advanced packaging and high-density PCBs continue to push technical specifications (resolution, thermal stability, adhesion), creating premium niches for high-performance resist chemistries.

For decision-makers, this translates into three practical actions in 2026:

- Prioritize qualification pathways with key customers around low-VOC, halogen-free, and low-bisphenol formulations—these are procurement gating items, not future nice-to-haves.

- Align capex and sourcing with volatility scenarios: validate alternative feedstocks, strategic stockpiles for critical monomers, and hedged supplier agreements.

- Differentiate through services—faster qualification, joint validation labs, and customer-focused troubleshooting are as defensible as proprietary chemistry in many accounts.

Competitive Landscape: Who Matters and How

The market’s competitive topology features a concentrated core of experienced specialty-chemicals and materials players, supplemented by regional formulators and nimble local suppliers. The top three players collectively account for a dominant share of revenue, with the top five extending that dominance—creating an environment where scale, formulation breadth, and customer trust deliver sustained advantage.

- Taiyo Ink Mfg. Co., Ltd. (Japan): Known for high-resolution formulations targeted at advanced PCB and packaging use-cases. Their R&D depth and legacy relationships in precision electronics create a durable moat for high-spec applications.

- Resonac Holdings Corporation (Japan): A major supplier of photosensitive films and inks for semiconductor packaging and substrates. Recent investments in next-gen packaging R&D signal intent to defend and expand share in premium segments.

- Tamura Corporation (Japan): Offers a broad portfolio of photoimageable resists and has a visible trade-show profile—an indicator of active commercial outreach and channel-strength preservation.

- San-Ei Kagaku Co., Ltd. (Japan): Specializes in specialty hole-plugging and substrate-specific chemistries for semiconductors—an example of vertical specialization that commands price premia.

- MacDermid Alpha Electronics Solutions (USA): A global supplier with deep PCB chemistry portfolios; plays the scale-and-service game to capture large OEM accounts.

- Eternal Materials Co., Ltd. (Taiwan), Kolon Industries (South Korea), Chang Chun Group (Taiwan), and Sumitomo Bakelite (Japan): These firms represent regional scale, dry-film expertise, and complementary resin platforms—important partners or acquisition targets depending on strategic intent.

- China-based specialists like Shenzhen Rongda and Jiangsu Kuangshun provide competitive cost structures and rapid product cycles—critical for volume-led offers in mainstream PCB production.

- Huntsman Corporation (USA): Supplies epoxy-based formulations that address thermal and reliability requirements for select segments.

Recent industry movements reinforce the competitive themes above. In 2026 several players amplified their market presence via trade shows and R&D commitments—Tamura showcased offerings at a major PV expo while Resonac launched a next-gen packaging R&D center in a strategic consortium. Eternal Materials increased visibility across coatings and plastics shows with low-VOC and durable resin messaging. These activities confirm the industry’s push along two axes: technology leadership and sustainability positioning.

Technology and Regulatory Dynamics — What Will Drive Winners

Three converging dynamics will determine winners in 2026 and beyond:

- Regulatory pressure and sustainability procurement: Stricter environmental rules are accelerating adoption of low-VOC, water-based, and bio-derived resists. Several European firms have moved to halogen-free, bio-based solutions and major OEMs are enforcing ppm-level restrictions on select bisphenol-type additives—an example of a procurement-led technology shift.

- Formulation complexity from advanced packaging: Requirements for higher resolution, thermal cycling resilience, and compatibility with novel surface finishes reward suppliers with R&D muscle and application engineering teams.

- Supply-side instability: Tariffs and geopolitical tensions have translated into recurring raw-material price shocks. Suppliers that can vertically integrate, source diversely, or price more transparently will win share with risk-averse buyers.

Regulatory regimes (REACH and other jurisdictional updates) and large OEM substance specifications are non-negotiable design constraints. Suppliers must maintain compliance data packages, proactive reformulation roadmaps, and robust testing documentation to remain qualified on strategic accounts.

Report Scope & Practical Deliverables

Our full study is intentionally operational and executive-ready. It contains:

- Market sizing and modeled scenarios (historical 2020–2025, base year 2025, detailed forecasts 2026–2032 with sensitivity cases).

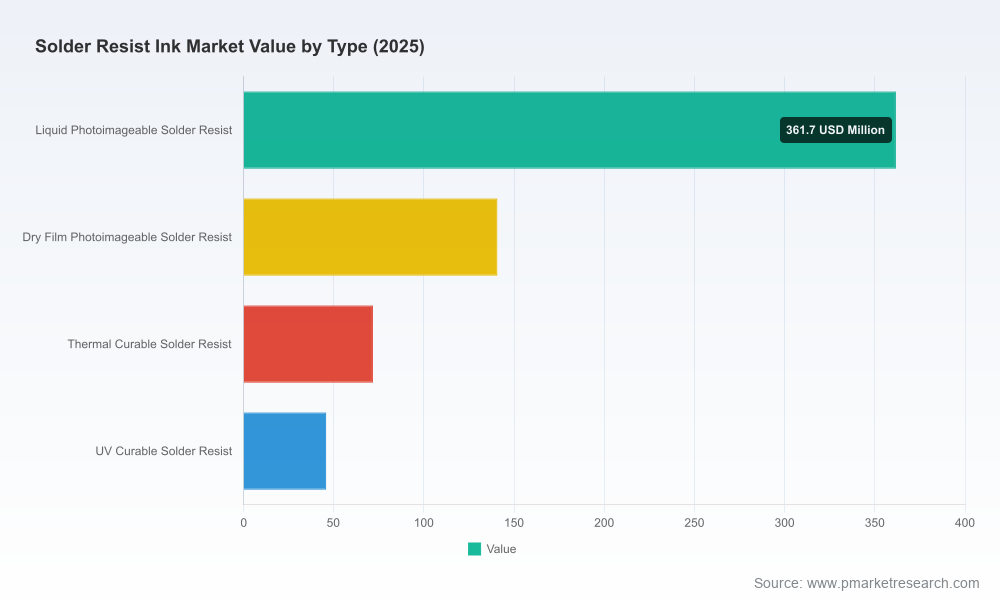

- Technology roadmaps and product-class profiles (photoimageable liquid and dry films, thermal and UV curable systems), mapped to end-market qualification requirements.

- Commercial playbooks for suppliers and OEMs: go-to-market options, M&A archetypes, and contract-structure recommendations tied to volatility scenarios.

- Customer qualification checklists and lab-validation timelines to accelerate adoption in tier-one OEMs.

- Competitive benchmarking and capability heatmaps for the major suppliers, with acquisition targets and strategic partnership matrices.

We deliberately withhold granular segment-level shares and region-specific percentages in this primer to preserve the strategic value of the full dataset. The detailed tables and proprietary splits—particularly the regional, type, and application breakdowns used to generate scenario analysis—are available in the subscription-grade report.

Risk Map — What Keeps the Market Vulnerable

- Regulatory shocks: Sudden tightening of substance limits can invalidate existing inventories and force costly reformulation and requalification cycles.

- Input-price and logistics spikes: Tariff changes and regional instability remain a persistent source of margin pressure.

- Customer qualification lag: Even superior formulations can take many quarters to convert into revenue due to long qualification cycles in semiconductor and automotive segments.

- Consolidation dynamics: With a concentrated top-tier, smaller players face margin compression or acquisition risks unless they own niche IP or exceptional cost positions.

Strategic Playbook: Recommendations for 2026

For executives planning 2026 actions, prioritize these levers:

- Fast-track regulatory-compliant formulations: Invest in low-VOC and low-bisphenol variants coupled with third-party certification—these unlock major customer lists.

- Customer co-development and risk-sharing: Offer joint validation programs and performance guarantees to shorten qualification timelines and capture higher ASPs.

- Supply resilience: Execute supplier diversification, strategic stockpiles, and selective vertical integration for critical monomers.

- M&A and partnership discipline: Target acquisitions that add unique formulation IP, application engineering teams, or regional production footholds rather than volume-only plays.

Next Steps — Where to Access the Full Intelligence

This primer demonstrates the strategic value of the 2026 edition of PW Consulting’s Solder Resist Ink Market study: clear market sizing, a robust growth outlook, and a set of actionable commercial and technical prescriptions to inform capital allocation, product strategy, and M&A. For full access to the proprietary segment splits, regional matrices, and candidate lists for acquisition or partnership, request the complete report and the accompanying scenario model. PW Consulting will provide a brief, client-only walkthrough to align the findings with your organization’s decision calendar.

Contact PW Consulting to schedule a tailored briefing and to obtain the complete dataset, which includes the revenue model (USD, Million unit basis), concentration analytics, and qualified supplier heatmaps that underpin the recommendations above.

For detailed analysis of this topic, please visit the official page:Solder Resist Ink Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com