Powered Air Purifying Respirator (PAPR) Market — Strategic Preview for 2026 Decision-Makers

Executive summary

This preview distills the strategic value of PW Consulting’s forthcoming PAPR Market study and explains why 2026 is a pivotal planning year for procurement, product development, and M&A decisions across healthcare, industrial safety, and defense markets. Built on an evidence base spanning 2020–2025 and forward projections to 2032, the study synthesizes market sizing, competitive positioning, regulatory shifts, cost drivers, and practical playbooks that executives and procurement leaders will use to convert uncertainty into competitive advantage.

Powered Air Purifying Respirator (PAPR) Market

Market trajectory: growth with structure

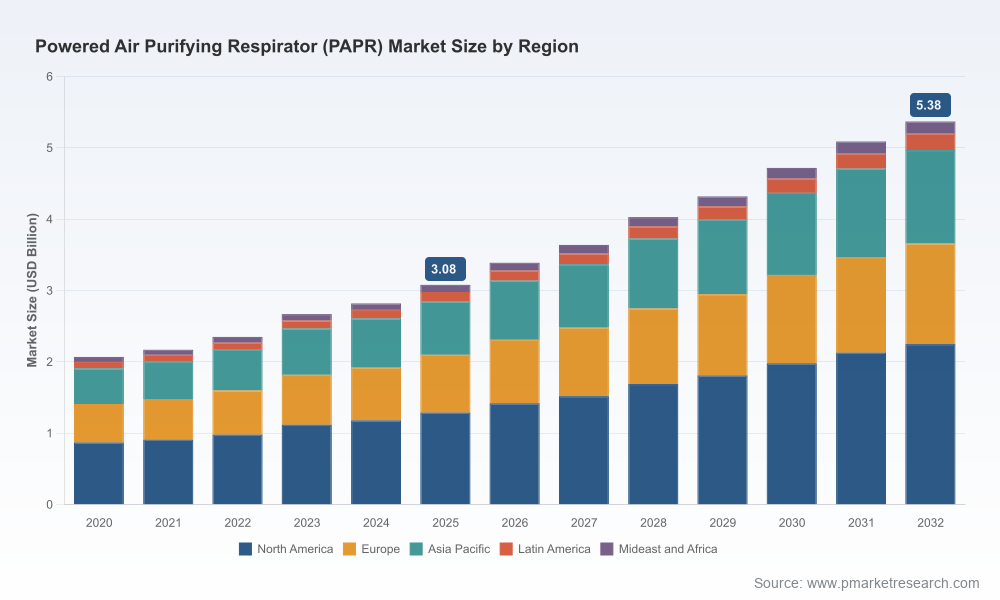

The global PAPR market has moved from early pandemic-driven demand into a structurally growing market characterized by steady commercial adoption and recurring consumable revenue. Our model shows total market value rising from USD 2.07 Billion in 2020 to USD 3.08 Billion in 2025, with a compound annual growth rate (CAGR) of 8.3% projected over the 2026–2032 forecast window. By 2032 the market is projected to be USD 5.38 Billion. This is not a narrative of transitory spikes; it represents an inflection toward normalization and durable expansion driven by regulatory recalibration, product refresh cycles, and creeping adoption in non-healthcare industrial segments.

Powered Air Purifying Respirator (PAPR) Market

What the headline numbers mean for corporate strategy

- Capital allocation: Growth at ~8.3% CAGR supports multi-year capital plans for manufacturing capacity and R&D, but timing matters—early entrants can lock in share via platform investments while late entrants face stronger incumbency.

- Revenue model evolution: Recurring revenue from filters, batteries and service contracts will increasingly dominate lifetime value. Procurement teams should model TCO across multi-year replacement and maintenance cycles rather than one-time equipment purchases.

- Concentration and competition: Market concentration is material—three leading firms control a majority share (CR3 ~54.5%) and the top five approach two‑thirds of the market (CR5 ~65.0%). This creates high barriers for scale-focused entrants but also creates white space for specialized offerings and regional partnerships.

Competitive landscape—incumbents, capability vectors, and near-term moves

The competitive set is a mix of global industrial safety majors and focused respirator specialists. Leading firms combine platform endurance, distribution depth, and regulatory track records; they are simultaneously modernizing product platforms and extending channel strategies.

Powered Air Purifying Respirator (PAPR) Market

- Dräger (Lübeck, Germany): Maintains a strong engineering posture through modular helmet/facepiece systems suitable for both industrial decontamination and clinical scenarios. R&D investments focus on integration and durability in multi-shift environments.

- MSA Safety (Pittsburgh, USA): Leverages distribution partnerships and complementary product portfolios to broaden access. Recent exclusive distribution agreements expand their welding and industrial PAPR offerings—an example of channel-enabled growth.

- Bullard (Cynthiana, USA): Product refresh cycles are accelerating; Gen-3 platform launches emphasize improved battery architectures and cleaner maintainability—features that directly reduce operational downtime and service cost.

- AirBoss Defense Group (Winnipeg, Canada): Competes on compactness and lightweight designs, positioning PAPR as a practical alternative for field operations and defense logistics where mobility and fast don/doff matter.

- 3M (St. Paul, USA): Continues to push into heavy industrial and hazardous-location applications, leveraging brand trust and integrated safety ecosystems to cross‑sell PAPRs into long-standing customer relationships.

Regulatory and operating dynamics that will drive 2026 decisions

- Regulatory recalibration: Two regulatory signals are reshaping demand profiles. In 2025, a proposed OSHA update removed certain medical clearance requirements for users of filtering facepiece respirators and loose-fitting PAPRs—this reduces administrative friction for industrial adoption. In April 2026, the FDA issued draft guidance proposing enforcement discretion for NIOSH-approved PAPRs intended for healthcare use; this is intended to reduce premarket burdens during public health situations. Both developments lower the entry friction for broader deployment but increase the importance of compliance documentation and post-market surveillance.

- Product safety and quality vigilance: Recent FDA references to a device recall linked to assembly defects underscore that product reliability and supplier traceability remain critical. Procurement and quality teams must demand robust manufacturing controls, lot-level traceability, and clear corrective‑action plans.

- Cost drivers and supply chain exposures: Battery chemistry (lithium-ion, NiMH) and filter media are the primary material cost centers. Labor for maintenance and fit-testing continues to drive total cost of ownership in hospital and industrial settings. Mitigating strategies—multi-year supplier contracts, diversified battery sourcing, and plans for in-house or outsourced maintenance—should be prioritized.

Operational impact by buyer type (summary view)

Different buyer cohorts face distinct imperatives:

- Hospitals and health systems: Must balance infection control protocols with capital constraints. The removal of some clearance requirements lowers adoption hurdles, but clinical procurement still demands interoperability with existing PPE programs, consumable logistics, and staff training.

- Manufacturing and construction: Operational continuity and worker comfort dominate. Companies will favor platforms with long battery life, simple maintenance, and minimal training overhead to reduce downtime and safety incidents.

- Specialized sectors (oil & gas, defense): These buyers prioritize hazardous-location approvals, intrinsic safety, and ruggedization. Certification pathways and field-service support become decision levers.

What PW Consulting’s full report delivers (actionable and field‑tested)

Our full study is explicitly designed to be operationally implementable for 2026 initiatives. The published report includes:

- Market sizing and validated growth scenarios through 2032, with sensitivity analyses that reflect alternative regulatory and supply chain outcomes.

- Commercial and procurement playbooks—template RFP language, contract terms to mitigate obsolescence risk, and maintenance-vs-replace decision matrices built for hospital and industrial buyers.

- Competitive heat maps and vendor scorecards that juxtapose technology features, service coverage, and channel strength (note: detailed segment revenue breakdowns and region/type/application-level tables are reserved for the full report to protect the integrity of the competitive analysis).

- CapEx and TCO models with input controls for battery cost volatility, filter consumption rates, and labor assumptions—ready to be customized to your operational parameters.

- Regulatory playbook and surveillance templates that operational teams can use to track rulemaking, recalls, and certification requirements in real time.

- M&A and partnership advisory: target screens, valuation heuristics, and integration risks for firms seeking inorganic scale or capability extension into adjacent respiratory protection categories.

Strategic recommendations for 2026 planning

- Adopt a two-track procurement stance: secure incumbent supply for continuity while piloting innovative, lightweight platforms in targeted workstreams. This hedges operational risk while creating options for scale migration.

- Shift from CAPEX-only thinking to a service-enabled model: evaluate vendor offerings on lifecycle service, consumable logistics, and data-enabled maintenance forecasting. Where feasible, negotiate outcome-based SLAs tied to uptime and filter delivery metrics.

- Insist on verifiable traceability and quality controls: require manufacturing lot traceability, third-party test data, and supplier corrective action plans as bid prerequisites—especially given recent recalls and FDA scrutiny.

- Model regulatory scenarios: run sensitivity analyses that incorporate both accelerated permissive policies (easing clinical adoption) and tightening recall/regulatory review scenarios. Use these to stress-test inventory and stockpiling decisions.

- Pursue selective partnerships: for manufacturers, channel expansions and OEM partnerships (distribution or co-branded systems) are high-leverage plays to expand addressable markets without proportionate capex.

- Prepare integration playbooks for battery and filter supply: longer-term supply agreements or vertical moves into filter production can materially reduce input cost volatility and improve margin predictability.

Why this preview — and why now

We purposefully present a strategic, model-driven preview that establishes trends and competitive dynamics while reserving detailed slice-and-dice data (for example, revenue by region, device type, and application at granular levels) for subscribers of the full PW Consulting report. This “preview” approach is deliberate: it provides enough strategic insight to inform boardroom debates and procurement policies, while directing practitioners to the primary report for the empirical inputs required to execute procurement, investment, or M&A actions with confidence.

Next steps for executives

- Use the topline growth projections and concentration metrics provided here to brief finance, procurement, and safety leads on 2026 budget posture and risk appetite.

- Contact PW Consulting for the full report to obtain vendor scorecards, customizable TCO models, procurement templates, and the granular regional/type/application matrices that support contract-level decisions.

- Book a strategic workshop with our team to convert the report’s insights into a 90‑day executable roadmap (supplier selection, pilot programs, and regulatory monitoring cadence).

For C-suite and procurement teams preparing capital, sourcing, or product strategy decisions in 2026, the PAPR market represents both an operational necessity and a business opportunity. The window to set durable advantages—through platform selection, supplier structuring, and regulatory preparedness—is now. PW Consulting’s full PAPR Market study provides the empirical backbone and practical tools required to act decisively; consider this preview your invitation to a deeper, execution-oriented dialogue.

For detailed analysis of this topic, please visit the official page:Powered Air Purifying Respirator (PAPR) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com