Les Meilleures Plages pour un Casino en Ligne de Qualité

Other |

2026-06-19 12:18:26

As the global healthcare supply chain continues to recalibrate after pandemic-era shocks, crude heparin has re-emerged as a critical strategic input for pharmaceutical manufacturers, contract producers and healthcare systems. Our PW Consulting study—anchored on a 2025 base year and a detailed historical review (2020–2025) with a forward-looking forecast through 2032—quantifies a market that expanded meaningfully over the past half-decade and is expected to sustain mid-single-digit to high-single-digit growth through 2032. The compound annual growth rate (CAGR) over the 2026–2032 forecast window is 7.47%, and the study models the market trajectory under multiple scenarios to stress-test sourcing, pricing and regulatory pathways.

Crude Heparin Market

Procurement and raw-material risk: crude heparin is a primary upstream input for anticoagulant APIs and low-molecular-weight heparins (LMWHs). Volatility in upstream supply or regulatory friction can cascade through margins and production schedules for downstream drugmakers. For executive teams planning 2026 budgets and capital allocation, proactive reconfiguration of sourcing strategies will likely yield outsized risk mitigation benefits.

Crude Heparin Market

Regulatory compliance as a strategic lever: regulatory requirements tightened materially at the end of 2025 concerning import documentation, species-origin traceability and lot-level contaminant testing. These controls elevate the cost and time-to-qualification of suppliers and create a competitive advantage for firms with validated, auditable supply chains.

Crude Heparin Market

Consolidation and partnership opportunities: the market concentration metrics indicate a fragmented supply base—no small number of players yet dominate decisively—creating fertile ground for strategic alliances, vertical integration or targeted M&A to secure dependable feedstock and capture margin uplift.

Our modelling shows the global crude heparin market increased steadily from the early 2020s into 2025 and is projected to continue rising through 2032. The base-year analysis (2025) and the forecast horizon reflect supply-side constraints, demand dynamics from cardiovascular and surgical anticoagulant use cases, and the influence of raw-material sourcing patterns. At a 7.47% CAGR for 2026–2032, the market profile supports capital investment cases for capacity expansion, selective integration of upstream processes, and long-term offtake contracts—provided firms can navigate regulatory and biosecurity headwinds.

Biosecurity and raw-material concentration: porcine intestinal mucosa remains the predominant raw material worldwide due to extraction yields and established processing pathways. This technical reality means that outbreaks affecting swine populations create outsized supply risk; recent reports have highlighted disease-driven disruptions in key producing regions, stressing availability and elevating the premium for traceable, disease-free supply chains.

Regulatory tightening and lot-level scrutiny: regulators—led by recent revisions in importation rules—now require more granular analytical data, species-origin records and contaminant testing for each shipment of crude heparin. These higher compliance thresholds increase the time and financial cost of qualifying new suppliers and raise the barrier to entry for some prospective entrants, but they also reward firms that have demonstrable traceability and robust quality systems.

Quality risk: persistent vigilance against known adulterants (for example, oversulfated chondroitin sulfate) and ruminant-derived contaminants remains an active regulatory condition and a commercial differentiator. Buyers will increasingly prioritize suppliers that can demonstrate both analytical rigor and independent third-party verification.

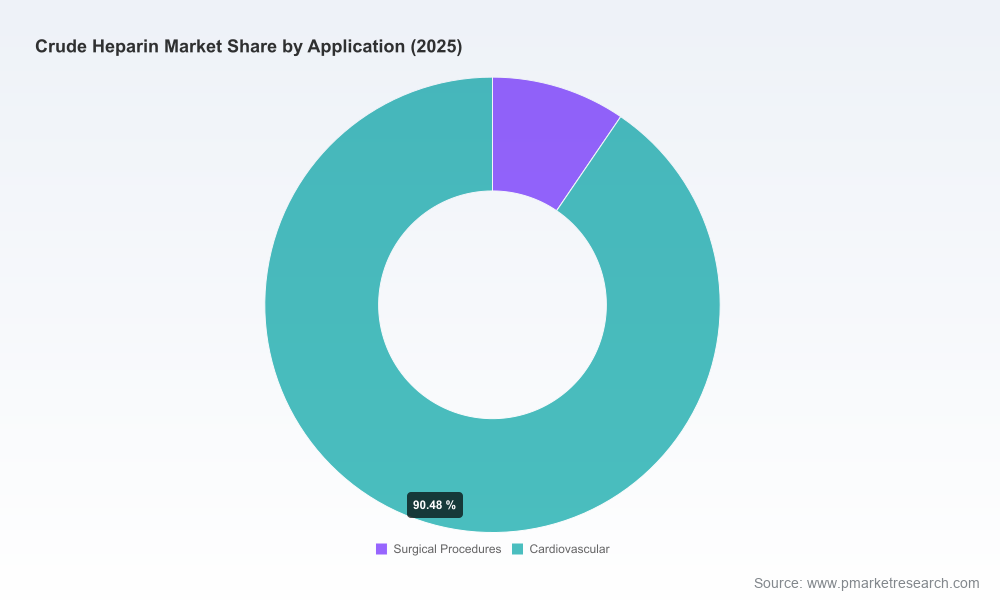

Downstream demand resilience: demand drivers include established cardiovascular indications and perioperative anticoagulation needs. While clinical practice evolves, the fundamentals of anticoagulant therapy ensure base demand. However, incremental demand is sensitive to pricing, supply stability and substitution dynamics.

The crude heparin ecosystem comprises upstream extractors, API manufacturers, and large pharmaceutical consumers. Key internationally active firms illustrate the strategic options available to market participants.

Integrated producers with global reach: Established European and North American players have invested in multi-site production footprints and brand-level quality reputations. Their advantages include long-standing regulatory relationships, diversified commercial channels and the ability to supply pharmaceutical-grade starting material at scale.

Regional champions from China: Several multinational Chinese biochemical groups occupy substantial positions across the value chain, from crude extraction through API manufacture. Their scale and integrated industrial chains enable cost-competitive supply, but their exportability is influenced by domestic biosecurity events and evolving international standards.

Downstream pharmaceutical buyers: Large drug manufacturers that rely on crude heparin for LMWH production represent a concentrated demand base for certain supply lines. These firms mitigate upstream risk through diversified sourcing and supplier qualification programs and, in some cases, maintain strategic partnerships or offtake agreements to secure supply.

Recent corporate developments underscore how companies are positioning within this landscape. Major producers have maintained high visibility at industry fora, signalled plans to optimize profitable growth streams, and achieved index inclusions that improve access to capital. Firms have also highlighted continued focus on API and LMWH production lines—evidence that both upstream supply and downstream conversion capacity remain attractive operational bets.

Importation rules now require detailed species-origin documentation and shipment-level contaminant analytics. Corporates should assume longer supplier qualification timelines and higher compliance costs when budgeting for 2026 supplier diversification or new geographic sourcing.

Biosecurity episodes in major supplying regions have periodic potential to create acute shortages. Scenario planning should therefore include supply disruption triggers, lead-time elongation assumptions, and inventory-depth requirements to maintain uninterrupted production.

Trade policy and inspection regimes may add friction at ports and border crossings. Firms that pre-emptively align to the most stringent expected standards will face fewer downstream surprises and will be better positioned competitively.

Reconfigure supplier portfolios: Move from transactional sourcing to stratified supplier relationships—qualify primary suppliers with demonstrable traceability, identify regional second sources with validated contingency capacity, and create rapid-qualification playbooks for emergency onboarding.

Invest in traceability and analytics: Upgrading inbound quality analytics and supplier auditing programs reduces recall risk and shortens time-to-release. Consider co-investment models with key suppliers to underwrite enhanced testing capacity that benefits both sides.

Evaluate vertical integration selectively: For firms with sizable downstream exposure or strategic need for assured supply, targeted upstream investments or long-term offtake agreements can deliver insulation from price and availability shocks. Financial modelling should weigh capital intensity against probability and expected duration of supply disruptions.

Develop hedging and inventory strategies: Holding strategic buffer inventory, implementing supply options contracts, and integrating supply-disruption triggers into production planning can blunt the impact of short-term shocks. The optimal policy will depend on cost of carry, shelf-life considerations and regulatory constraints on stockpiling.

Pursue M&A and partnerships tactically: The fragmented concentration profile suggests opportunities to pursue bolt-on acquisitions, strategic joint ventures, or manufacturing alliances that can consolidate sourcing and expand control of quality-critical upstream processes.

Market sizing and scenario-based forecasts (base year 2025; detailed historical series through 2020–2025; forward projections to 2032), with sensitivity analyses calibrated to supply shocks, regulatory tightening and demand elasticity.

Supply-chain maps and supplier scorecards that evaluate traceability, audit readiness, capacity flexibility, and compliance posture—designed to support supplier selection and contingency planning.

Regulatory heatmaps and a compliance playbook outlining approval timelines, documentation requirements and recommended quality-control protocols to expedite qualification under recent rules.

Competitive benchmarking of incumbent players (profiles, strategic positioning, recent developments), plus a transaction pipeline and valuation sensitivities for potential acquisitions or strategic partnerships.

Commercial and procurement playbooks: model contract language, recommended acceptance testing regimes, inventory optimization tools, and scoring matrices for offtake and co-investment decisions.

Risk matrix and mitigation options, including quantified scenario outcomes for production shortfalls, price spikes and regulatory non-compliance events—constructed to be directly actionable in 2026 planning cycles.

For executives planning 2026 strategy, crude heparin is no longer an operational afterthought: it is a strategic lever. The market’s mid-to-high single-digit growth trajectory over the next multi-year cycle, combined with tightening regulatory requirements and episodic biosecurity risks, converges to make proactive sourcing, quality assurance and selective vertical positioning high-return priorities. PW Consulting’s full study provides the granular tools—supplier scorecards, scenario models, contract templates and regulatory playbooks—needed to convert insight into defensible decisions. This introductory analysis highlights the strategic imperatives; the comprehensive report contains the operational detail required to execute them.

PW Consulting is prepared to brief executive teams, procurement committees and boards on tailored implications for your business, including bespoke stress tests and an implementation roadmap calibrated to your exposure profile. Access to the complete dataset and supplier-level intelligence is available through our report portal; clients seeking an expedited executive workshop for 2026 planning should contact our advisory desk to schedule a deep-dive.

For detailed analysis of this topic, please visit the official page:Crude Heparin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com