Baking and Cooking Paper Market Registering a CAGR of 8.1% Through 2036 | Growth in Bakery and Foodservice Industries Supports Expansion

Networking |

2026-06-27 05:46:25

PW Consulting’s new Industrial Energy Management System (IEMS) Market study is built for one purpose: to turn energy strategy from a compliance checkbox into a competitive advantage. As organizations confront tightening regulation, rising expectations for decarbonization, and increasingly volatile energy markets, the IEMS opportunity is shifting from pilot projects to enterprise-scale transformation. Our analysis synthesizes historical performance (2020–2025), a fully modelled forecast window (2026–2032), and actionable playbooks that will matter to CEOs, plant directors, and CFOs making investment decisions in 2026.

Industrial Energy Management System (IEMS) Market

Regulatory momentum is accelerating. New and updated mandates—from the EU’s Energy Efficiency Directive to U.S. federal and state-level policy changes—are raising the baseline requirements for industrial energy reporting, auditing, and continuous improvement. Standards such as ISO 50001 and national building and energy codes are turning voluntary best-practices into practical requisites for many industrial operators.

Industrial Energy Management System (IEMS) Market

Carbon economics and compliance are reshaping capital allocation. Paris-aligned commitments, carbon pricing trajectories, and associated incentives make IEMS investments not only an environmental imperative but a quantifiable route to improved margin resilience.

Industrial Energy Management System (IEMS) Market

Technology and grid dynamics create new value pools. Distributed resources, demand-side flexibility, and the maturation of AI-driven optimization change the value equation for multi-site operators. The ability to orchestrate energy across assets (site-level to portfolio-level) is now a determinative source of competitive differentiation.

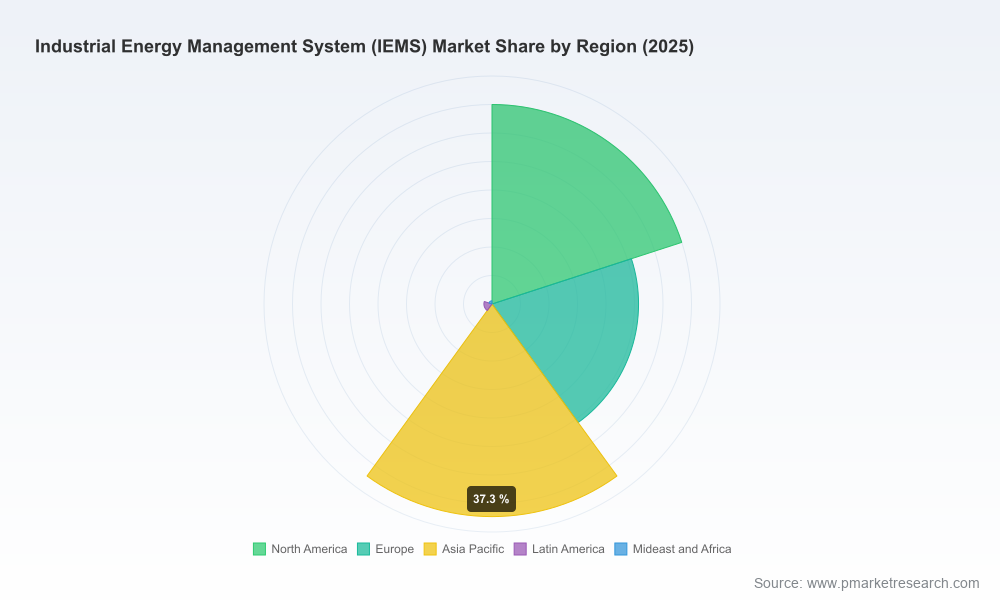

The IEMS market has moved from selective adoption to broad industrial relevance. Our historical model shows steady growth from 2020 through 2025, driven by a mix of regulatory compliance projects, retrofit programs, and greenfield automation initiatives. In monetary terms, the market reached an estimated USD 35.2 Billion in our base year of 2025. Looking forward, the study’s point forecast projects a compound annual growth rate (CAGR) of approximately 8.27% over the 2026–2032 period, taking the market materially higher by 2032.

At the same time, market structure reflects a balance between global incumbents and fast-moving niche players. Concentration metrics in the study indicate a market where leading vendors retain substantial share, but a meaningful portion of activity is won by innovative challengers offering specialized software, AI-driven optimization, or verticalized services. This dynamic creates room for both scale-focused and technology-focused strategies.

This study is deliberately operational. Rather than abstract frameworks, we deliver tools and guidance that enable decision-makers to act in 2026:

Executive decision briefs that translate market scenarios into recommended capital allocation and procurement timelines.

Site-level implementation playbooks: step-by-step audits, measurement protocols, KPIs to track, and a three-phase rollout template for multi-site deployments.

Vendor selection and contract templates, including negotiation checklists for software license structures, hardware warranties, data ownership, and service-level commitments.

TCO and ROI models calibrated to real-world energy tariffs, carbon costs, and operational savings profiles—designed to integrate into finance and asset teams’ existing capital planning processes.

Integration blueprints for IT/OT convergence that balance cybersecurity, latency, and data fidelity requirements for closed-loop energy optimization.

Case studies and quantified outcome summaries from representative manufacturing, process, and energy-intensive sites—showing typical pathways to payback, non-energy benefits, and operational risks.

A scenario-based forward model with sensitivity testing across key variables (energy price volatility, carbon cost trajectories, regulatory stringency), enabling risk-adjusted prioritization of projects.

The IEMS vendor field is diverse, ranging from global automation conglomerates to software-first challengers. Our competitive analysis profiles each major player on capability, scale, go-to-market approach, and typical client fit:

ABB Ltd — A major automation and power management provider whose IEMS offerings integrate advanced energy monitoring and optimization into broad industrial automation portfolios; well-suited to heavy industry rollouts that need end-to-end hardware and control solutions.

Eaton Corporation PLC — Strong in power management and electrical systems, Eaton couples hardware depth with growing software and analytics capabilities for industrial energy optimization.

Emerson Electric Company — A control- and process-automation incumbent recently strengthened operational posture with a new global headquarters; excels where process optimization and energy management converge.

EnerNOC / Enel X — Focused on demand response and energy services, the company is a strategic partner for firms that need market-facing flexibility and monetization of load-side resources.

Rockwell Automation — Delivers industrial automation software with embedded energy monitoring, particularly compelling for manufacturers seeking tight integration of production and energy KPIs.

Cisco Systems — While not a traditional energy vendor, Cisco’s networking and IoT platforms are critical enablers for scalable IEMS deployments that demand robust, secure data infrastructure.

General Electric — Brings systems-level industrial expertise and portfolio-scale solutions that appeal to process industries with complex asset fleets.

Honeywell International — Combines building and industrial automation with strong services capabilities for facility-level energy management and retrofits.

Schneider Electric — Offers a comprehensive energy management and automation stack, including edge-to-cloud architectures that are often selected for cross-site standardization programs.

Siemens AG — A leader in digital industries and industrial IoT, Siemens’ IEMS platforms emphasize integration, lifecycle services, and plant-level process optimization.

Yokogawa, Azbil, Mitsubishi Electric — Regionally strong incumbents with deep domain expertise in measurement, control, and process automation; attractive partners for manufacturing and process plants requiring proven reliability.

IEM (Industrial Electric Manufacturing) and specialized system integrators — Provide tailored power distribution and energy management systems where bespoke engineering is required.

explitia, Tibo Energy, Prescient Technologies, MRI Software — Represent a new wave of software-first or AI-centric vendors delivering real-time energy optimization, portfolio analytics, and horizontal SaaS platforms; these challengers are rapidly winning greenfield projects and retrofit proofs-of-value.

The competitive picture is dynamic. Recent developments—Emerson’s relocation of global HQ (2026), Tibo Energy’s funding round to scale AI-driven grid and site-level optimization (2025), and Azbil’s strategic relocation strengthening automation capabilities (2025)—underscore continued investment and positioning by both incumbents and challengers. These moves reflect an industry shifting from product sale to platform and services-led engagement models.

What is the organization’s target level of energy transparency and over what timeline? (Site-only, regional roll-up, or portfolio orchestration?)

How should IT/OT responsibilities be allocated to manage data governance, cybersecurity, and upgrade cycles?

Which procurement model best matches risk tolerance and capital constraints: CAPEX-heavy integrated systems, SaaS-first software with managed services, or hybrid operating leases?

Where should pilots be deployed to maximize learning while minimizing disruption? (Identification of “teachable” sites is covered in our rollout playbook.)

How will the organization capture grid-facing value (demand response, ancillary services) while ensuring production continuity?

What governance and KPIs will ensure continuous improvement post-deployment?

Should M&A or partnerships be used to fill capability gaps—e.g., AI analytics, domain-specific control expertise, or global service scale?

The report strikes a careful balance: it delivers the analytical muscle leaders need to justify and execute investments, while preserving proprietary detail that is best accessed through our full dataset and client engagement channels. You will receive:

Proprietary, scenario-based financial models that translate market forecasts into site-level investment cases.

Vendor scorecards and negotiation playbooks that are directly usable in RFP processes.

Implementation roadmaps and risk matrices tailored to plant types and regulatory environments.

Action-oriented recommendations on sourcing, financing, and scaling IEMS across industrial portfolios.

For readers who need the granular segmentation tables, region- and application-level forecasts, or our full vendor benchmarking matrix, the report’s companion data pack and client workshops unlock those layers. This article serves as a strategic trailer: it reveals the trends, the tools, and the choices you must make in 2026, while preserving the full, actionable datasets for direct engagement.

Book a ninety-minute executive briefing with PW Consulting to translate the study’s insights into a prioritized 12–24 month roadmap for your organization.

Run a focused pilot using our site selection criteria and implementation playbook to create an early proof-of-value that informs enterprise rollout decisions.

Use our vendor negotiation templates and TCO model to accelerate procurement cycles and protect margin outcomes.

Industrial energy management will be a defining operational capability in the mid-2020s. PW Consulting’s IEMS Market study equips leaders with the forecasts, frameworks, and field-proven playbooks necessary to turn compliance and cost-control into strategic advantage. For the complete dataset, vendor matrices, and bespoke advisory services, please visit our report page or contact our IEMS practice for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Industrial Energy Management System (IEMS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com