Plastic Pallets Market — Strategic Preview for 2026 Decision‑Makers

As organizations calibrate supply chains for resilience, sustainability, and cost discipline in 2026, plastic pallets have moved from a niche replacement for wood to a strategic asset class. This preview from PW Consulting synthesizes the directional intelligence and decision frameworks you need now — exposing the macro trajectory, competitive fault lines, regulatory inflection points, and high‑impact actions — while reserving the granular region/application matrices and price curves for the full report.

Plastic Pallets Market

Why this research matters for 2026

- Market momentum: The global plastic pallets market has demonstrated consistent expansion through the 2020–2025 period and is projected to continue growing across our 2026–2032 forecast horizon at a compound annual growth rate (CAGR) of 6.68% (USD Million basis). Understanding that growth path is essential for capital allocation, contract design, and product strategy in 2026.

- Operational leverage: Decisions on ownership vs. pooling, pallet specification, recycling content, and warehouse protection strategies now materially affect total landed cost, working capital, and insurance exposure.

- Regulatory & risk timing: Recent code updates and standards are already changing facility design and operating cost expectations. Firms that act early gain a first‑mover advantage in cost containment and customer assurance.

Market trajectory: the macro picture

Across the historical window (2020–2025) the market expanded from a modest baseline to a materially larger industry footprint. By the 2025 base year our consolidated market estimate sits in the mid‑thousands of USD Million; under the central forecast the industry is set to approach the high‑thousands by 2032, reflecting the sustained 6.68% CAGR. That macro expansion masks important structural dynamics: growing demand from hygiene‑sensitive verticals, an accelerated shift toward recycled‑content resins, and the rising commercial prominence of pallet pooling and service models.

Plastic Pallets Market

For executives, this combination of steady market growth and structural change means 2026 is a high‑leverage year for strategic moves — invest selectively in capacity or partnerships, redeploy legacy wood‑pallet assets, or double down on service offerings that convert product into recurring revenue.

Plastic Pallets Market

Key structural dynamics to watch

- Hygiene and traceability as primary demand drivers: Food, beverage, and pharmaceutical supply chains are increasing specification stringency. Hygienic, rotomolded, and easy‑clean designs command premium positioning and open routes to longer contract tenors with brand owners.

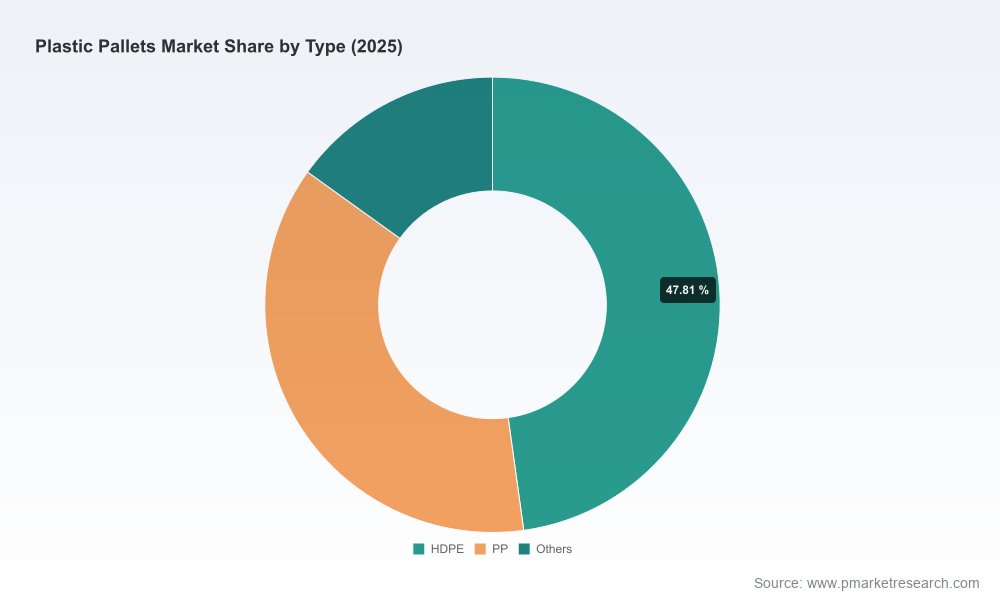

- Recycled content and circularity: HDPE and PP remain the dominant feedstocks. Leading suppliers are offering products with significant recycled composition; some commercial offerings now exceed 30% recycled HDPE. This creates both differentiation and sourcing complexity — resin quality, certification, and supply stability matter.

- Service model bifurcation: The market is bifurcating between pure manufacturers and integrated service players that offer pooling, reverse logistics, and asset lifecycle management. Pooling operators can capture higher lifetime value but require scale and operational discipline.

- Regulatory risk crystallizing into operational cost: Fire protection guidance has evolved to explicitly address plastic pallets; recent updates (e.g., NFPA 13 guidance and NFSA advisories) raise warehouse commodity classifications when plastic pallets are used, especially when reinforced. The knock‑on effects include sprinkler design requirements, higher insurance premiums, and possible limits on allowable storage arrangements.

Competitive landscape — how to read the field

The market displays moderate concentration: our market concentration metrics indicate the top three firms account for a material but not dominant share (CR3 ~35%), and the top five approach a higher but still non‑monopolistic share (CR5 ~45%). That structure produces a competitive environment where platform economics benefit those who can combine product, logistics, and digital services, while specialised manufacturers can sustain margins through technical differentiation.

Core players and strategic postures to monitor:

- CHEP (Australia) — a global leader in reusable pallet pooling and supply solutions. CHEP’s scale and pooling capabilities make it the benchmark for service‑centric models and contract design for multinational shippers (https://www.chep.com/).

- Rehrig Pacific Company (USA) — durable, nestable and rackable product designs focused on supply‑chain efficiency and sustainability; competitive where compatibility with existing material handling is critical (https://www.rehrigpacific.com/).

- ORBIS Corporation (USA) — specializes in reusable, rackable and stackable designs for industrial and retail logistics, competing on design flexibility and aftermarket services (https://www.orbiscorporation.com/).

- CABKA Group (Germany) — emphasis on recycled‑material products and eco variants; relevant for buyers with aggressive sustainability targets (https://cabka.com/).

- Schoeller Allibert (Netherlands) — global provider of hygienic, durable and reusable pallets, with strong retail and foodservice footprints (https://www.schoellerallibert.com/).

- Regional and niche manufacturers — including Millwood Inc., Polymer Solutions International (PSI), Elkhart Plastics, Lile Group, and Vantage Plastics — supply differentiated technologies (recycled blends, rotomolding, thermoforming) and custom solutions that serve technical or regulatory niches.

Implication: scale and service integration deliver pricing power in enterprise contracts, while technical differentiation (material science, hygiene, recyclability) secures premium positions in regulated verticals. Expect continued M&A activity where service players acquire manufacturers to control cost and where manufacturers secure recycling assets to assure feedstock.

Regulatory inflection — immediate and medium‑term impacts

- Fire protection standards: The most consequential recent development is updated guidance on how plastic pallets affect commodity classification in high‑piled storage and the explicit inclusion of plastic pallet design in sprinkler calculation standards. Practically, this can move facilities into higher sprinkler and racking specification bands, increasing retrofit costs and insurance loads.

- Phytosanitary and cross‑border friction: Plastic pallets remain exempt from ISPM‑15 treatment requirements applicable to wood pallets — a persistent trade facilitation advantage that supports substitution, especially in cross‑border cold‑chain and consumer goods flows.

- Product safety and claims: Growing buyer scrutiny on recycled content claims will push suppliers toward third‑party verification and chain‑of‑custody documentation as a table‑stakes requirement.

Supply‑chain levers and raw material risk

HDPE and PP dominate the feedstock mix. Resin price volatility and availability are the leading cost uncertainty for manufacturers. Strategic mitigants include:

- Vertical integration into recycling streams or long‑term offtake with recyclers to stabilise cost and secure certified recycled resin.

- Design for material efficiency — thinner ribs, cellular cores, and hybrid constructions that preserve strength while reducing resin use.

- Service models (pooling and take‑back) that internalise return flows and reduce reliance on virgin resin.

Actionable recommendations for 2026

- Prioritise hygiene‑sensitive and traceability use cases: If you serve food, pharma, or premium retail, accelerate procurement of hygienic pallet designs and insist on cleanliness and traceability KPIs in contracts.

- Reassess ownership economics vs. pooling: Run a life‑cycle TCO with scenarios that incorporate higher sprinkler/insurance costs driven by recent standards; pooling may shift capex to opex and reduce network complexity.

- Lock resin risk management: Secure multi‑year recycled‑resin offtake agreements or invest in recycling capacity if your volume justifies vertical integration.

- Embed regulatory scenarios in capital plans: For any warehouse expansion or retrofit in 2026, include sprinkler redesign and potential racking reclassification in baseline capex models.

- Invest in digital services: RFID, IoT, and analytics turn pallets from a commodity into a service platform; this can improve utilization, reduce losses, and create new revenue streams.

- Pursue selective M&A: Targets include local manufacturers with technical competencies, recycling assets that secure feedstock, and regional pooling operators that can be integrated into a global service footprint.

- Differentiate on verified sustainability: Commit to certified recycled content percentages and transparency in chain‑of‑custody to capture procurement mandates from large brand owners.

What the full PW Consulting report provides (operational detail)

The full study goes beyond this strategic preview. It delivers:

- Granular demand models by region and application (with scenarios), and a near‑term outlook tuned to 2026 procurement cycles.

- Comprehensive supplier scorecards and competitive benchmarking, including technology roadmaps, capacity maps, and business model diagnostics.

- Price and cost curves, resin‑sensitivity analyses, and an interactive CapEx/Opex model you can adapt to your volumes and facility footprint.

- Actionable go‑to‑market playbooks for manufacturers, poolers, and 3PLs — including contract templates, KPI frameworks, and pilot implementation roadmaps.

- M&A screen and valuation guidance calibrated to the sector’s current concentration (CR3 ≈ 35%, CR5 ≈ 45%) and growth trajectory.

- Regulatory impact assessment down to sprinkler-design implications and insurance cost scenarios — with mitigation options and cost estimates.

Final synthesis — how to use this intelligence in 2026

2026 is the inflection year where strategic positioning in the plastic pallet market translates into measurable commercial advantage. The combination of steady market expansion (6.68% CAGR), regulatory tightening on warehouse protection, and escalating buyer demands for hygiene and sustainability creates a landscape in which execution quality — not just product availability — determines margin and market share. Use this preview to align your board‑level priorities, then consult the full report to operationalize investments, select partners, and stress‑test scenarios against detailed datasets and supplier diagnostics.

For the full datasets, interactive models, and proprietary supplier scorecards referenced here, access the PW Consulting Plastic Pallets Market report. The full intelligence package is designed to convert this strategic preview into executable plans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Plastic Pallets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com