Europe Footwear Sole Materials market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-20 11:41:35

As PW Consulting’s newest industry brief on LTCC (Low‑Temperature Co‑Fired Ceramic) ceramic substrates, this introduction synthesizes the market dynamics that matter most to executives making resource, partnership, and product decisions in 2026. Our base‑year assessment places the global LTCC substrates market at USD 1,458.2 Million in 2025, and our model projects a steady expansion at a 6.3% CAGR through the forecast horizon. By 2032 the market approaches a USD‑scale milestone, reflecting durable end‑market demand for higher layer counts, tighter RF performance, and embedded functionality. This article highlights strategic implications, competitive signals, and the practical utility of the full PW Consulting study — while intentionally reserving detailed segment tables and the proprietary model that underpin our findings to the full report.

LTCC Ceramic Substrates Market

2026 is the year when strategy execution meets industrial inflection. For manufacturers and system OEMs, product roadmaps initiated in 2023–2025 are entering mass qualification and capacity ramp phases. For component suppliers and investors, the differentiation between firms that capture high‑value, high‑reliability programs (e.g., automotive radar, 5G RF modules, AI accelerator I/Os) versus those competing on commodity pricing is becoming stark. Our LTCC market study translates macro growth into operational decisions: where to locate capacity expansions, which material systems to prioritize, and how to structure commercial agreements to protect margin as volume scales.

LTCC Ceramic Substrates Market

Since 2020 the LTCC market has demonstrated resilient compound growth underpinned by multiple, partly convergent drivers: the proliferation of 5G infrastructure and higher‑frequency mobile front ends; accelerating electrification and advanced driver assistance systems (ADAS) in vehicles; demand for thermally robust, miniaturized interposers in AI and heterogeneous compute packages; and continued growth in industrial and medical applications requiring high‑reliability multilayer ceramic stacks. These technology trends drive not only unit growth but also an increase in average selling price and complexity per unit as design wins shift toward higher layer counts, embedded passives, and integrated sensors.

LTCC Ceramic Substrates Market

Supply‑side signals matter too. Our tracking of industry developments shows leading producers expanding capacity and launching next‑generation products: for example, Murata announced capacity expansion and new high‑frequency substrate introductions during 2024–2025 to support automotive and telecom ramps, while Kyocera commercialized a multilayer core substrate targeting advanced AI semiconductor packages in early 2026. These moves validate the thesis that premium LTCC content is migrating toward high‑rigidity, thermally engineered, and high‑density solutions.

Importantly, material‑chain and regulatory noise that often confounds strategic planning is muted for LTCC as of early 2026. Alumina feedstock prices and supply availability have been stable, and no new export controls or targeted tariffs on key LTCC precursors were introduced across major economies during 2025–2026. Standard industry certifications (ISO 9001, AEC‑Q200 for automotive) remain baseline requirements. In short, demand, not sudden upstream shocks, is the dominant near‑term driver.

The LTCC supplier landscape is moderately concentrated: the top three firms collectively account for roughly two‑thirds of the market, and the top five capture approximately three‑quarters. This degree of concentration creates distinct strategic consequences: premium price capture for differentiated offerings; high barriers for scale entrants; and intensified competition in mid‑tier commodity segments.

Competitive differentiation is increasingly defined by depth in three capability vectors: material science (dielectric and thermal properties), multilayer process expertise (yield and layer count), and integration services (embedded passives, sensors, and turnkey module assembly). Firms that combine two or more of these vectors command structural pricing advantages and stronger program longevity.

The full report is designed to be a working tool for commercial, operational, and investment teams. Key actionable contents include:

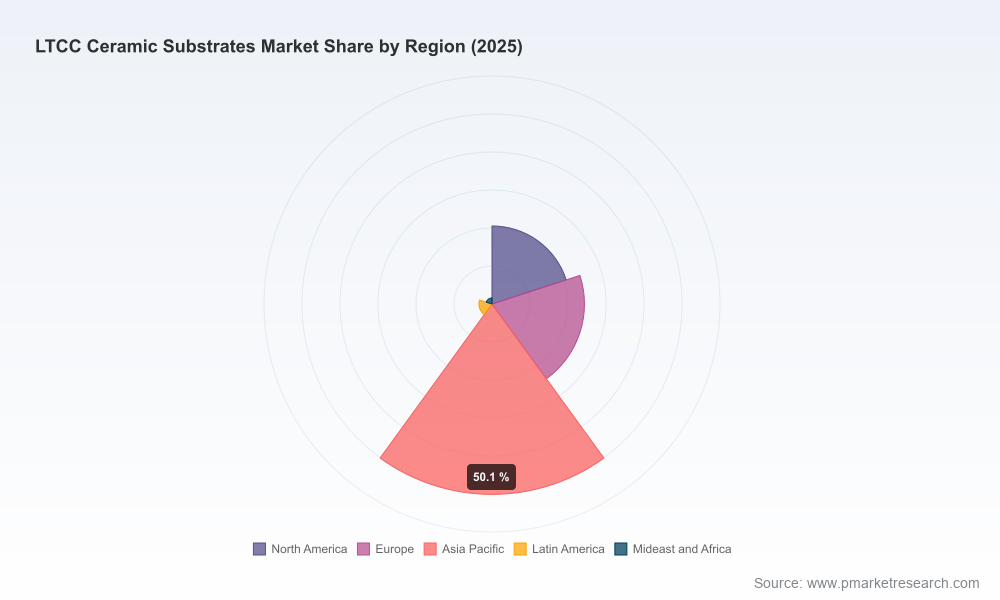

To preserve the tactical advantage of our clients and maintain data integrity, the public summary intentionally omits the granular regional and application splits embedded in the model — these are available only in the full report and interactive dashboards.

The following recommendations translate our analysis into prioritized actions for different stakeholders:

Executives should treat the PW Consulting study as a playbook, not a summary. Use the model to run three scenarios: base‑case demand expansion (our central 6.3% CAGR), a high‑adoption case driven by accelerated automotive and AI uptake, and a constrained case where program delays compress near‑term volumes. For each scenario, map cash‑flow implications of capacity builds, run sensitivity analyses on yield improvement timelines, and stress test supplier concentration impact using the provided CR3/CR5 benchmarking.

Finally, the right tactical moves are often timing dependent. Capacity investments announced in 2025–2026 will be judged by qualification wins secured in this cycle; procurement negotiations concluded this year will determine margin flow through 2027–2028. The market’s shape in 2026 rewards clarity of focus: narrow technical differentiation combined with contractual protections against volume‑and‑yield risk.

PW Consulting’s full LTCC report contains the granular segmentation, supplier share matrix, and interactive financial model necessary to operationalize these recommendations. If you are preparing capital allocation, supplier strategy, or M&A due diligence this year, the full report and our bespoke advisory services provide the data, scenario models, and negotiation playbooks you will need to convert insight into advantage.

For detailed analysis of this topic, please visit the official page:LTCC Ceramic Substrates Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com