3D Printing Software Market Trends Shaping the Industry Through 2034

Other |

2026-05-12 11:28:55

As the toilet tank fittings market moves beyond 2025 into a period of sustained expansion, 2026 is shaping up as a pivotal year for capital allocation, product strategy, and supply‑chain redesign. Our latest PW Consulting market study — anchored on a 2025 base year and a 2026–2032 forecast horizon — shows a sector that has expanded steadily from the early 2020s and is projected to continue growing at a mid‑single‑digit annualized rate (CAGR ~7.5% over the forecast). Aggregate market value has moved from a multi‑billion‑dollar baseline in 2020 to a substantially larger industry total by 2025, with forecast scenarios indicating near‑term resilience and medium‑term upside as efficiencies, regulatory pressure, and retrofit cycles intersect.

Toilet Tank Fittings Market

Transition momentum: After a period of recovery and stabilization, 2026 is the first year where several structural forces — regulation, materials cost dynamics, and product innovation — converge to materially change product roadmaps and channel economics.

Toilet Tank Fittings Market

Investment timing: Firms that commit to targeted investments in low‑flow, retrofit‑friendly technologies, or that secure resilient polymer supply arrangements in 2026, will capture disproportionate share as purchasers accelerate upgrades.

Toilet Tank Fittings Market

M&A and consolidation window: Market concentration metrics indicate a moderately consolidated landscape (CR3 ≈ 55%; CR5 ≈ 70%), suggesting room for both bolt‑on acquisitions among regional leaders and disruptive entrants that can scale quickly via distribution partnerships.

Our modeling uses five years of historical performance through 2025 and a seven‑year forecast to 2032. That longitudinal view surfaces three durable themes: steady demand growth reflated by renovation cycles; regulatory tightening around water consumption and product performance; and cost volatility in polymer and energy inputs. These drivers combine to produce the 7.5% CAGR we report for the forecast window — a rate that is meaningful for strategic planning without implying a near‑term boom that would distort capital allocation.

Regulatory pressure and product compliance: Water efficiency standards (for example, regulatory frameworks that mandate maximum flush volumes and incentivize high‑performance low‑flow fittings) are no longer hypothetical. Companies must bake compliance into product design and certification roadmaps or face access barriers to key markets. This changes the R&D prioritization ladder: certification engineering and test labs move from cost centers to strategic assets.

Raw material and input cost volatility: Recent supplier actions and public disclosures show upstream price adjustments tied to plastics and energy. These cost movements are compressing gross margins for commodity products while widening returns for firms able to substitute materials, re‑engineer parts counts, or pass value through via premium performance claims.

Channel and retrofit demand: Residential retrofit cycles and commercial refurbishment programs are creating predictable replacement flows. Firms with retrofit‑friendly SKUs and simplified installation kits can accelerate attachment rates and reduce customer friction.

Portfolio re‑engineering: Prioritize modular designs that enable upgrades (e.g., conversion kits for older tanks), reduce bill‑of‑materials complexity, and improve manufacturability. Product modularity lowers SKU proliferation and shortens time‑to‑market for compliant variants.

Pricing and margin management: With input costs showing periodic upticks, adopt a segmented pricing strategy that differentiates core commodity items from performance‑differentiated SKUs tied to water savings and ease of install. Consider indexed supplier contracts and selective pass‑through clauses in distributor agreements.

Go‑to‑market motion: Strengthen relationships with plumbing wholesalers and national retail chains by offering training, installation support, and co‑branded consumer education on water savings — mechanisms that lift conversion and support premium positioning.

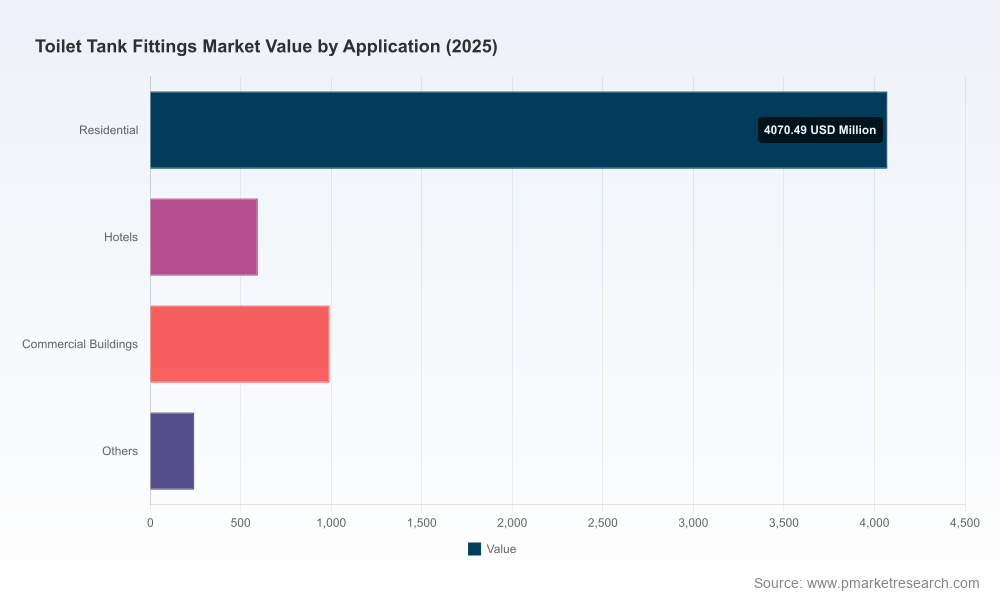

Our research deep dives into the principal segmentation lenses used by industry participants: product type (e.g., fill mechanisms, flush mechanisms, accessory components), application (residential, hospitality, commercial, and other end uses), and geography (regional demand profiles, regulatory intensity, and distribution structures). The public primer intentionally avoids publishing the granular split tables here — these are preserved in the full study to protect the proprietary demand model and to drive decision‑grade insight accessibly.

The competitive map is characterized by a mix of established specialized manufacturers and integrated system providers. Leaders combine broad distribution networks with scale in procurement and manufacturing; challengers focus on channel intimacy, installation simplicity, or product differentiation.

Fluidmaster — Strategic positioning: Known for universal fill valves and repair kits, Fluidmaster’s strengths are channel penetration in retail and mass‑DIY segments and a well‑recognized serviceable SKU set. For incumbents and investors, Fluidmaster represents a model of margin resilience driven by aftermarket attachment and strong brand recall in replacement parts.

Korky — Strategic positioning: With U.S. manufacturing heritage and concentration in repair kits and components, Korky’s pathway to growth is via premiumization (durability claims, U.S.‑made positioning) and selective channel expansion. Private‑label partnerships and OEM retrofit programs are high‑impact levers.

Danco — Strategic positioning: Danco’s universal‑fit approach and broad component range make it a go‑to supplier for installers. Firms evaluating partnership or consolidation should measure Danco’s cross‑channel capabilities and aftermarket loyalty as primary considerations.

Geberit — Strategic positioning: As a system provider with concealed tank systems and integrated flushing mechanisms, Geberit competes more at the specification and project level. Recent developments include a product catalog refresh (released late 2025/announced early 2026) and a measured price adjustment on select polymer products in mid‑2026 to offset energy and plastics cost pressure. These moves underline Geberit’s ability to influence supplier pricing and signal the importance of integrated systems in commercial and high‑end residential segments.

Regulatory enforcement timelines and certification throughput — delays or accelerated approvals materially change addressable demand.

Polymer feedstock and energy price trends — even modest sustained increases compress margins on commodity fittings and make differentiation via materials or process innovation more valuable.

Distribution consolidation or exclusive contracts — a wave of consolidation among wholesale distributors would alter access economics for mid‑tier brands.

Adoption of retrofit‑first policies by institutional purchasers and utilities — demand spikes for compliant, easy‑install kits can shift growth from new‑build segments to aftermarket channels.

We designed the full market study as an execution playbook for commercial leaders and investors. Highlights include:

Proprietary demand model with scenario runs and sensitivity to price, regulatory tightening, and retrofit adoption curves.

Supply‑chain maps with supplier risk scoring, near‑term input cost exposure, and mitigation playbooks.

Go‑to‑market frameworks for tiered distribution (retail vs. wholesale vs. specification channels) and a commercialization checklist for launching certified low‑flow SKUs.

Vendor benchmark dossiers and comparative capability matrices for the leading players, including product portfolios, channel strategies, and recent corporate actions.

Actionable M&A and partnership roadmaps: target criteria, valuation drivers, and integration templates for bolt‑on acquisitions aimed at scaling installation services or retrofits.

Regulatory impact modelling (national and sub‑national scenarios) that maps compliance costs and market access timelines to product P&L outcomes.

Implementation playbooks and a 90‑, 180‑, and 360‑day decision checklist for 2026.

Conduct a rapid compliance audit: Map your SKU portfolio against enacted and pending water‑efficiency standards; prioritize certification for high‑volume SKUs.

Lock supply levers: Negotiate flexible polymer sourcing clauses and explore secondary suppliers or material substitutions to reduce single‑supplier exposure.

Accelerate retrofit offerings: Pilot low‑installation‑time kits in two high‑volume channels and measure conversion economics before broader rollout.

Validate M&A targets: Use the report’s target scoring to shortlist acquisitions that add distribution density or installation capability, then run quick‑win integration plans.

For CEOs, product chiefs, and private equity sponsors contemplating moves this year, the critical value of the PW Consulting study is decision‑grade clarity: a validated market trajectory (7.5% CAGR in the forecast window), a calibrated view of concentration and competitive dynamics (CR3 ≈ 55%; CR5 ≈ 70%), and a set of executable playbooks that translate regulatory and cost noise into investment priorities. The public primer you are reading establishes the context and the judgments; the complete report contains the proprietary segmentation matrices, price and volume tables, and company scorecards that operational teams will use to build budgets, structure deals, and launch products in 2026.

Access the full dataset and the operational annex to unlock detailed regional and segment forecasts, SKU‑level pricing scenarios, and the competitive playbook that underpins our 2026 recommendations.

For detailed analysis of this topic, please visit the official page:Toilet Tank Fittings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com