Unlocking Drug Discovery Potential Through Advanced High Throughput Screening Solutions

Health |

2026-06-10 18:27:29

The lithium‑sulfur (Li‑S) battery market is transitioning from laboratory promise to commercial reality. Between 2020 and the 2025 base year, total industry revenues have moved from the low tens of millions of USD to a materially larger market position, and our forecast projects a continuation of that rapid expansion — reaching a multiple of the 2025 base by 2032 at a compound annual growth rate of 25.7%. For executives making allocation, partnership and M&A decisions in 2026, this report synthesizes the operational levers, regulatory constraints, and competitive vectors that determine who wins the next phase of Li‑S commercialization.

Lithium-Sulfur Battery Market

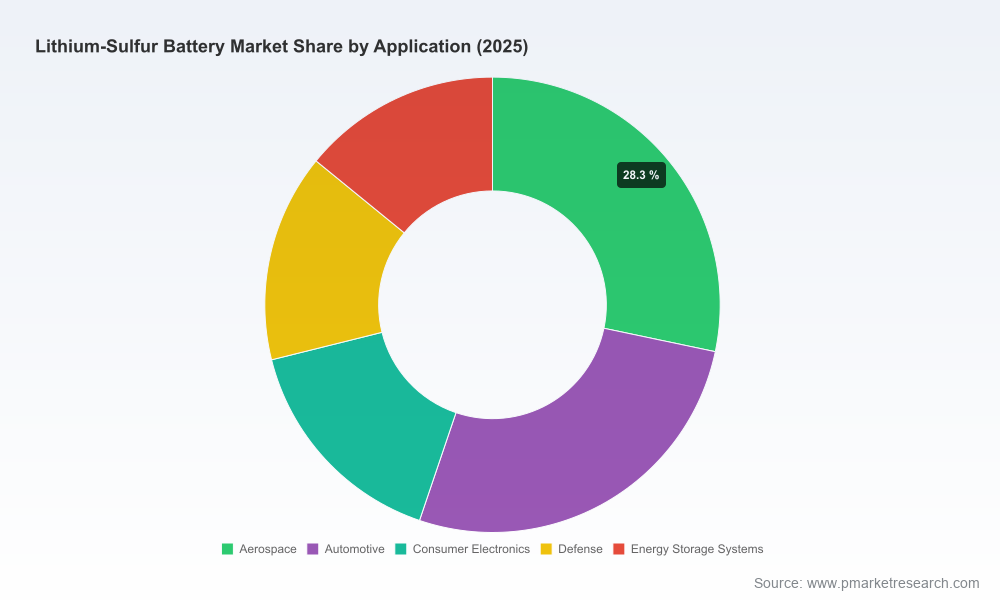

Fast, capital‑intensive scale‑up: With a projected market that grows from USD 53.0 Million (base year 2025) to USD 262.8 Million by 2032 at a ~25.7% CAGR, ramp timing and plant economics will decide margins. Delays of 12–24 months in cell qualification or supply‑chain integration can materially erode first‑mover returns.

Lithium-Sulfur Battery Market

Supply‑chain localization is strategic, not just tactical: Recent movements (e.g., U.S. initiatives to maintain investment tax credits for hybrid storage through 2035 and high‑visibility industrial policy in Europe) favor vertically integrated manufacturers or buyers that can demonstrate regional sourcing and low carbon footprints.

Lithium-Sulfur Battery Market

Technology selection drives go‑to‑market segmentation: Variants of Li‑S chemistries and cell formats (pouch, cylindrical, foil‑based anodes, nano-encapsulated sulfur cathodes, etc.) are at different maturity stages. Choosing a technology partner is as consequential as plant location.

Executive market map and scenario engine: Base case and downside/upside scenarios for 2026–2032 that integrate technology learning curves, capital intensity, and regulatory shifts.

Unit‑cost and BOM build‑ups: Detailed manufacturing cost models for representative cell formats, with sensitivity to anode protection solutions, cathode architectures and electrolyte formulations.

Supply‑chain heat map and procurement playbook: Supplier tiers, critical raw material availability (including sulfur and lithium‑metal), tariff and trade considerations, and mitigation strategies for single‑point failures.

Regulatory and incentive impact assessment: EU carbon‑footprint declaration requirements, U.S. investment tax credit implications, and long‑duration storage policy drivers that materially affect LCOE and procurement choices.

Commercial diligence package: Go‑to‑market templates, customer segmentation, channel economics, and a prioritized list of target OEMs and system integrators for pilots and scale contracts.

M&A and partnership screening: A curated model for evaluating technology acquisitions, equity investments and joint ventures — with playbooks for structuring earn‑outs tied to technical milestones.

Appendix of primary research: Interview synopses, plant visit notes, and supplier questionnaires used to validate assumptions.

Regulatory tailwinds and reporting obligations: As of February 2026, new EU battery regulation requires carbon footprint declarations for industrial rechargeable batteries above specified capacity thresholds. For producers and buyers active in European supply chains, embedded emissions will be a procurement filter — and will influence sourcing, process electrification and recycling strategies.

Investment incentives persistence: The U.S. policy environment has kept Section 48E‑style investment tax credits available through 2035 for hybrid battery energy storage, sustaining a landscape in which capital deployment decisions hinge on tax equity availability and project timelines.

Raw‑material economics favor sulfur‑based chemistries: Sulfur cathode active material costs reported in technical industry presentations run at a fraction of lithium‑ion equivalents (approximately one‑third on a per‑kWh materials basis), a structural advantage for Li‑S in applications where gravimetric energy and cost per kWh are primary drivers.

Long‑duration storage targets: Public programs targeting sub‑5 cents/kWh levelized costs for long‑duration storage by 2030 create a market pull for technologies — like Li‑S — that can combine higher gravimetric energy with lower raw‑material cost bases, provided cycle life and system integration challenges are resolved.

The market concentration metrics indicate a moderately fragmented early market: the top three players account for just over a third of industry revenue, while the top five approach mid‑forties. This places a premium on first‑mover scale and proprietary IP for those seeking to establish durable positions.

Lyten Inc. (San Jose, CA) — World leader in using proprietary 3D graphene and U.S.‑sourced cells for high‑energy applications. 2025–2026 milestones include domestic production starts for battery‑grade lithium‑metal foil, major equity raises, product launches targeted at defense and drone markets, and strategic acquisitions to close recycling and capacity gaps. Lyten exemplifies vertical integration and defense‑led commercialization.

Zeta Energy LLC (Houston, TX) — Developer of sulfurized‑carbon cathodes and 3D metallic lithium anodes targeting EV energy density without cobalt/nickel. Strategic OEM collaborations (including a recent joint development agreement with an automotive OEM) indicate a go‑to‑market path via vehicle manufacturers rather than pure play cell sales.

Solidion Technology, Inc. (Dallas, TX) — Focused on ultra‑high gravimetric energy cells for transport and aerospace. Their work highlights the trade‑off set between energy density and cycle life that buyers must evaluate against application requirements.

Gelion Technologies (Sydney, Australia) — Offers cathode materials designed for compatibility with existing lithium‑ion manufacturing infrastructure, reducing near‑term capex and transition risk for stationary storage customers.

theion GmbH (Berlin, Germany) — Targets ultra‑fast charging and aviation markets (eVTOL) with polymer‑host anode architectures and ambitious energy density targets — a good example of specialization towards high‑value niches.

PolyPlus Battery Company (San Diego, CA) — Proprietary protected lithium‑metal anodes and advanced electrolytes; their technical approach is a reminder that anode protection and electrolyte stability are gating items for commercial Li‑S viability.

Sion Power Corporation (Tucson, AZ) — Pursuing high‑energy Licerion® platforms for EV and aerospace markets, highlighting the commercial pathway via high‑value early adopters.

Bettergy Corp., Giner Inc., CIC energiGUNE — These players represent a mix of manufacturing scale efforts, DOE‑funded R&D and European pilot capabilities — collectively, they underscore the ecosystem dimension beyond pure‑play cell makers (equipment, testing, pilot lines).

Lyten commenced domestic production of battery‑grade lithium‑metal foil and has subsequently announced major equity raises and acquisition plans to secure recycling and European capacity. These moves signal a deliberate push to control both upstream materials and downstream closed‑loop value chains.

Cross‑industry partnerships (for example, automotive OEMs partnering with Li‑S developers) are emerging as a preferred commercialization route, allowing cell developers to de‑risk by co‑developing cells to vehicle specifications rather than attempting broad market sell‑through.

Public policy milestones — from EU carbon declarations to U.S. tax credits for storage — are influencing siting, capital structure and customer contracting strategies for 2026 plant builds.

Cycle life and warranty exposure: Li‑S cell chemistries can offer compelling gravimetric energy, but cycle stability under real duty cycles is the gating technical risk. Warranty frameworks and performance guarantees must be explicitly modeled into contracts.

Scale‑up complexity: Moving from prototype to multi‑MW lines requires process control investments and supply‑chain fidelity for lithium‑metal and protected anodes; failure to secure parts or feedstock can create multi‑quarter delivery slippages.

Recycling and end‑of‑life: Early evidence suggests integration of recycling pathways — particularly for lithium‑metal anodes — will be both a regulatory expectation and a margin lever for producers that can reclaim valuable components.

Market concentration dynamics: With CR3 at ~34.2% and CR5 at ~45.8%, the mid‑market remains contestable; strategic investments and alliances in 2026 can materially change ranking over a short horizon.

Run parallel qualification pathways: Start at least two pilot programs with different technology partners (one targeting rapid integration using existing Li‑ion infrastructure, one targeting maximum gravimetric energy) to hedge technology and time‑to‑market risk.

Secure upstream optionality: Negotiate options or small equity stakes with lithium‑metal foil and sulfur feedstock suppliers to ensure tariff‑free, localized supply and preferential access.

Model regulatory exposure: Incorporate EU carbon‑footprint reporting and U.S. tax credit timelines into capex project IRRs and customer bid models now — these variables move procurement behavior.

Prepare M&A playbooks: Determine thresholds for bolt‑on acquisitions versus JV partnerships tied to technical progress milestones; structure earn‑outs and IP milestones to align incentives.

This briefing intentionally highlights macro sizing (USD 16.9m in 2020 → USD 53.0m in 2025 → USD 262.8m by 2032, CAGR ~25.7%) and the strategic drivers executives must act on in 2026. The full PW Consulting Lithium‑Sulfur Battery Market report contains the granular regional and application splits, supplier‑level cost models, downloadable financial models, and the proprietary segmentation tables referenced throughout this summary. To evaluate specific investment cases, pilot budgets, or M&A targets you will need those datasets and our scenario spreadsheets.

If your 2026 capital allocation or partnership roadmap depends on winning a position in the Li‑S value chain, our complete report and the accompanying financial models are designed as decision‑ready assets. PW Consulting’s cross‑functional team can also run a tailored 60–day commercial due diligence and pilot selection process to compress development timelines and de‑risk first commercial deployments.

For detailed analysis of this topic, please visit the official page:Lithium-Sulfur Battery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com