Vitamin E Market 2026: Strategic Signals for Executive Decision-Making

As companies shape strategies for 2026 and beyond, the Vitamin E market is presenting a mix of resilient demand growth, supply-side stressors, and strategic inflection points. PW Consulting’s latest Vitamin E Market study (base year 2025, forecast period 2026–2032) synthesizes historical performance, supply-chain diagnostics, supplier benchmarking, and scenario-driven forecasts to convert data into executable choices. In short: the market is neither a low-risk commodity nor a niche innovation play — it is a mid-sized, globally traded ingredient market with definable winners and clear tactical moves for manufacturers, ingredient buyers, and investors.

Vitamin E Market

Market trajectory at a glance

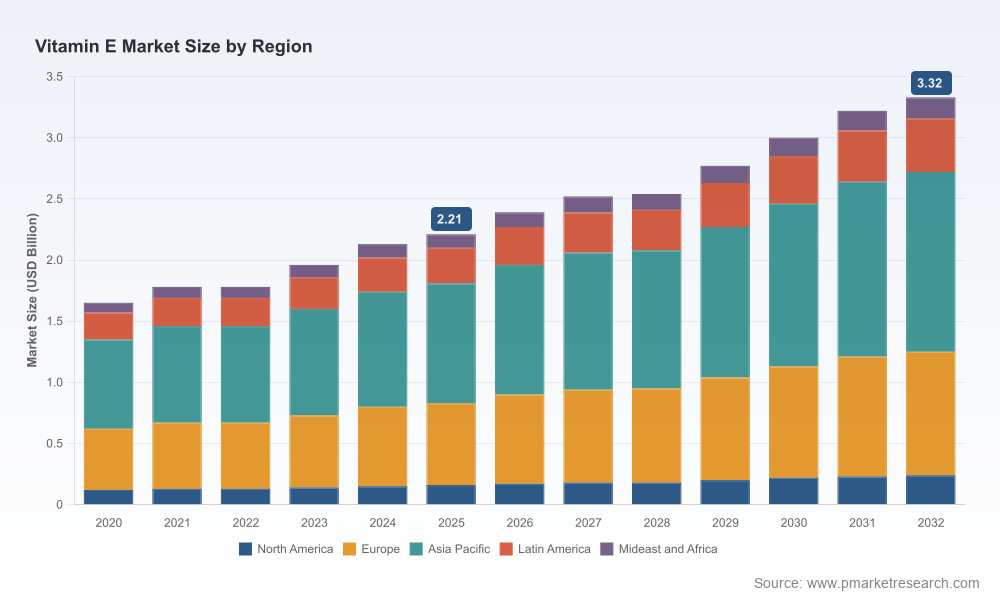

The Vitamin E market expanded from an estimated USD 1.65 Billion in 2020 to USD 2.21 Billion in 2025, reflecting steady end-market adoption across dietary supplements, functional foods, and related applications. Our modeling projects continued expansion through 2032, with the market reaching roughly USD 3.32 Billion and an aggregate compound annual growth rate of about 5.3% over the forecast window. This growth profile signals predictable baseline demand combined with episodic price and supply volatility — a mix that rewards firms with disciplined procurement, product differentiation, and supply visibility.

Vitamin E Market

Why this report matters for decisions in 2026

- Timing of investments: 2026 is a pivotal year to decide on capacity expansions, long-term off-take agreements, or backward integration. The forecast horizon shows attractive upside for premium, traceable natural sources, but success depends on securing feedstock and managing cost swings.

- Procurement strategy: With supply tightness reported from multiple origins in early 2026, procurement teams must move from transactional buying to portfolio-based sourcing that blends spot, forward, and strategic supplier relationships.

- Product portfolio prioritization: Companies must assign capital where margin and defensibility intersect — premium natural formulations with traceability and clean-label credentials versus lower-cost synthetic options for volume applications.

- Regulatory & labeling readiness: Evolving labeling norms and milligram-based declarations require reformulation and packaging alignment; companies that preempt label-driven reformulation will avoid costly commercial disruptions.

What’s inside the PW Consulting study (practical and operational)

This report is built for decision-makers who need actions, not just charts. Key deliverables include:

Vitamin E Market

- Proprietary demand model (2020–2032) calibrated to end-use trends and macroeconomic scenarios, enabling scenario-based volume and value forecasts.

- Supply-side heat maps and capacity tracker highlighting geopolitically sensitive feedstocks, milling bottlenecks, and expansion timelines for major producers.

- Price and margin sensitivity matrices that quantify the impact of feedstock swings, freight disruptions, and currency moves on COGS and gross margin under multiple procurement mixes.

- Supplier capability benchmarking (technology, quality certifications, traceability, sustainability credentials, and lead-time reliability) with anonymized scoring for rapid vendor shortlisting.

- Commercial playbooks for manufacturers and ingredient buyers — including negotiation templates, contract clauses for forced majeure and quality offsets, and best practices for collaborative forecasting.

- M&A and partnership heatmap identifying targets and strategic fits across upstream feedstock, midstream processing, and downstream branded ingredient players.

- Regulatory and labeling roadmap, with compliance checklists and product transition timelines to meet milligram-based Nutrition and Supplement Facts requirements.

- Risk register and stress tests — from agricultural seasonality to supplier closures — with recommended mitigation actions and insurance/hedging strategies.

Competitive landscape: Who matters and why

The Vitamin E value chain is competitively diverse. Market concentration remains relatively low-to-moderate, reflecting many regional processors alongside a handful of global ingredient suppliers. Our report analyzes the strategic positioning of leading participants and how their capabilities map to near-term market opportunities:

- Archer Daniels Midland (ADM) — Strong in natural-sourced vitamin E and mixed tocopherols, ADM’s scale and portfolio offer advantages in supply continuity and formula-level support for clean-label claims. Their integrated offering supports food and nutraceutical customers that prioritize efficacy and compliance.

- BASF SE — Known for high-purity formats and microencapsulation technology, BASF is positioned to serve formulators needing consistent performance in functional foods and supplements. Backwards-integrated production supports reliability in measured-volume contracts.

- dsm-firmenich (formerly DSM) — A Western supplier of natural, non-GMO vitamin E with premium traceability and patented processes. Their regulatory support and high-concentration offerings make them a partner of choice for branded nutraceuticals and pharma-grade formulations.

- Zhejiang Medicine — A large-scale Chinese producer with both synthetic and natural capability. Their ongoing capacity expansions influence global supply balances and form an important counterweight to Western suppliers, particularly for volume-driven markets.

- PMC Isochem — With specialized offerings such as TPGS, they occupy an important niche where solubilization and pharmaceutical excipient functionality meets regulatory-grade manufacturing.

- Cargill & Wilmar — Major processors emphasizing sustainable sourcing and feedstock control; their upstream position in vegetable oils provides risk-management advantages, especially where raw-material volatility drives costs.

- Merck KGaA, Eisai, American River Nutrition — These firms fill differentiated roles across pharmaceutical-grade supply, branded consumer offerings, and specialized nutraceutical supply chains.

Recent market developments underscore two themes we stress in the report. First, supply tightness — as noted by dsm-firmenich in March 2026 — has tightened availability from both Chinese and non-Chinese origins. Second, procurement innovation is accelerating: new e-commerce and digital procurement platforms (e.g., Prinova’s US platform launch in early 2026) are lowering search friction for buyers, but they do not replace the strategic value of vetted long-term supplier relationships.

Dynamics to monitor in 2026

- Feedstock and cost volatility: Seasonality and geopolitical shifts affecting vegetable oil prices create recurring production-cost shocks. Firms with integrated feedstock strategies or long-term contracts will enjoy margin stability.

- Regulatory pressure: Labeling rules (notably milligram-based declarations required in key markets) and evolving claims frameworks force product-reformulation decisions and can generate one-time transition costs.

- Premiumization vs. commoditization: Demand is bifurcating — premium natural, traceable vitamin E is commanding value in clean-label and clinical-positioned products, while commoditized synthetic options remain relevant for price-sensitive volume markets such as certain feed and bulk food uses.

- Technology and formulation innovation: Microencapsulation, beadlet technologies, and excipient-driven solubility solutions (e.g., TPGS) are altering application economics and shelf stability — critical for product developers.

- Sustainability and traceability: Buyers increasingly require chain-of-custody assurances and deforestation-free sourcing, which affects supplier selection and can justify price premiums.

Strategic playbook for 2026 — five executive moves

- Shift procurement to a portfolio model: Reduce spot exposure by layering strategic supplier agreements, indexed volume contracts, and selected spot purchases tied to a hedging policy.

- Prioritize traceable natural sources where margin allows: For consumer-facing brands, certification and non-GMO origins enable premium pricing and limit reputational risk.

- Invest in product-format innovation: Allocate R&D to microencapsulation and solubility technologies that reduce dose, improve stability, or enable novel matrices — these create differentiation and protect against price competition.

- Design supply contingency plans: Build mapped alternative sources, maintain buffer inventories for critical SKUs, and run periodic supplier stress tests to validate continuity plans.

- Use M&A and partnerships selectively: Identify upstream feedstock players and technology specialists as acquisition or JV targets to secure raw materials and proprietary formulation advantages.

Next steps and how to use this study

For executives and functional leaders preparing 2026 budgets and strategic decks, this report functions as both a decision-support toolkit and an operational manual. Use it to stress-test your procurement model, justify capex or M&A moves, and to operationalize labeling and compliance transitions. The report deliberately provides deep supplier benchmarking and scenario outputs while reserving core segmented tables and supplier-level numeric details for the full study — a deliberate design to protect the value of primary research and to invite collaborative engagements.

To unlock the full intelligence set — detailed segmentation matrices, supplier scorecards, contract templates, and our raw-model access — visit PW Consulting’s Vitamin E Market page or contact our advisory team. Our analysts can also run a tailored sprint to translate these insights into a 90-day execution plan for your company.

For detailed analysis of this topic, please visit the official page:Vitamin E Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com