Soccer Goalkeeper Gloves Market Regional Insights

Sports |

2026-02-26 06:12:46

This strategic briefing introduces PW Consulting’s comprehensive HFC Refrigerant Market study (base year 2025, forecast 2026–2032). It is written for executives, strategy teams, procurement leaders, and regulators who must make high-stakes decisions in 2026. The study synthesizes historical performance (2020–2025), forward projections under multiple regulatory scenarios and a granular competitive assessment to support decisions on sourcing, pricing, product portfolios, and M&A. The global market — measured in USD Billion — has expanded materially over the last five years and, under our central forecast, continues to grow through 2032 at a mid-single-digit CAGR (6.25%). This briefing demonstrates the study’s practical value while reserving detailed segment-level figures and worksheets for the full report.

HFC Refrigerant Market

Regulatory inflection point: 2026 brings binding operational rules that reframe compliance costs and product lifecycles. The U.S. EPA’s Subsection H leak-repair and management requirements became effective in January 2026, imposing inspection and repair obligations on larger HFC-containing systems and introducing GWP thresholds for heavier charge installations. Simultaneously, the AIM Act’s phasedown pathway continues to compress available allowances through the decade. Firms that anticipate timing and enforcement nuances will avoid costly remediation and stranded stock.

HFC Refrigerant Market

Price and supply volatility: Raw material inputs and spot-market dynamics have tightened supplier margins and shifted price formation. Chinese hydrofluoric acid costs rose sharply in 2025, and spot HFC prices remained firm into early 2026—conditions that have pushed several suppliers to implement steep, product-specific price actions during 2025–2026.

HFC Refrigerant Market

Strategic concentration: The market structure is highly concentrated, with incumbent producers capturing a large share of supply. This structural reality affects negotiations, access to transition technologies (low-GWP blends), and the speed at which alternative chemistries scale.

Decision urgency: Actions taken in 2026 — on inventory positioning, supplier contracts, product substitution strategies, and capital investments — will largely determine exposure to risk and opportunity through the rest of the decade.

PW Consulting’s central forecast charts a steady expansion from the 2025 base, reflecting continued demand in air conditioning, refrigeration and industrial applications combined with evolving product substitution dynamics. The model accounts for demand-side growth drivers (urbanization, cooling penetration, cold-chain expansion) and supply-side constraints (raw material cycles, regulatory allowances). Our scenario framework shows that, while base demand remains resilient, the rate of substitution to low-GWP alternatives and the timing of regulatory enforcement materially change vendor economics and market flows.

Two structural features deserve emphasis. First, concentration among leading producers amplifies the impact of individual supply or pricing decisions across the value chain; second, regulatory policy — both near-term operational rules and long-term phasedown targets — is the primary determinant of inventory and investment risk. In practice, these two forces interact: concentrated suppliers with differentiated low-GWP portfolios can disproportionately influence transition speed and costs.

Raw materials: HF feedstock volatility has direct and rapid pass-through into refrigerant pricing. In 2025 Chinese hydrofluoric acid prices rose appreciably, increasing production cost baselines for several manufacturers. Where producers lack hedging or alternative feedstock strategies, margin compression follows.

Spot and contractual markets: Spot HFC trading showed muted liquidity and sustained elevated prices in early 2026. Buyers reliant on spot procurement face two-sided risk: sudden price spikes and limited access during peak seasons. Conversely, long-term contracts that do not include robust indexation and force-majeure provisions can leave buyers exposed to cost shifts.

Regulatory compliance and stranded inventory: EPA and other jurisdictions are refining transition rules and, in some cases, extending compliance timelines for specific equipment categories. These policy moves can produce stranded high-GWP inventory risk for both producers and downstream OEMs — a key exposure we stress-test in our scenarios.

Logistics and export controls: Production allowances, export allowances and cross-border trade rules (including those tied to environmental compliance) mean that geographic diversification of supply is not a simple hedge; it requires active regulatory and customs management.

The market is dominated by a small set of players that combine manufacturing scale, proprietary blends, and channel reach. In the full study we model supplier cost stacks, blend portfolios and commercialization timelines; below are strategic snapshots of the leading firms and how recent developments shape their competitive angles.

Honeywell International Inc. — A leader with a broad low‑GWP portfolio and strong channel presence in HVACR. Recent commercial pricing actions have signaled willingness to use price as a lever to manage tight supply and incentivize migration to newer blends. Honeywell’s product positioning and supply discipline will remain a market-moving factor in 2026.

The Chemours Company — Strong brand recognition in fluorochemicals with active product campaigns around alternatives and retrofit solutions. Chemours’ investments in alternative refrigerants and its commercialization roadmap are central to buyers seeking transition pathways.

Arkema S.A. — European-based supplier with a growing presence in lower-GWP blends, augmented by strategic commercial arrangements that expand access to HFO-based options. These partnerships help Arkema accelerate its portfolio while navigating phasedown pressures.

Daikin Industries Ltd. — A major OEM and supplier whose product strategy tightly integrates refrigerant choices with equipment design, particularly for heat pumps and split AC systems. Daikin’s dual role as equipment maker and refrigerant supplier gives it a unique influence on adoption patterns.

Carrier Corporation and Trane Technologies plc — Both remain influential through equipment sales and integrated refrigerant servicing programs. Their choices about factory-charged chemistries and retrofit pathways materially affect aftermarket demand.

Iofina Chemical — Active in production under export allowances, especially where EPA quotas and export dynamics create niche opportunities; may play a role for buyers seeking alternative sources.

Linde plc — An industrial gas and refrigerant supplier with broad distribution networks; its logistics capabilities matter in a tight market where time-to-delivery can determine project viability.

Selected recent events — including a major portfolio expansion commercial arrangement between Arkema and Honeywell and a steep price increase on select products announced by one leading supplier in 2025 — illustrate how corporate strategies and supply-cycle stress can accelerate substitution or tighten availability. Meanwhile, the EPA’s post‑2025 regulatory milestones add a compliance overlay that all firms must manage.

The published study is designed as an operational toolkit as much as a market map. Key deliverables include:

A transparent market-sizing methodology with base-year reconciliation and an extensible demand model for 2026–2032 that you can reweight to test bespoke scenarios.

Regulatory scenario analysis that quantifies impacts under alternative EPA enforcement and allowance pathways, including stress cases for accelerated phasedown or extended compliance timelines.

Price and cost models: input cost drivers, feedstock sensitivity testing (including hydrofluoric acid shocks), and supplier pass-through behavior matrices.

Supply-chain stress-tests and contingency playbooks: inventory optimization templates, supplier diversification checklists, and contractual clauses to mitigate price and delivery risk.

Supplier scorecards and strategic positioning maps for leading producers (product breadth, low‑GWP readiness, commercial behavior, logistics strength, and regulatory risk).

M&A and partnership playbooks: valuation heuristics, carve-out opportunities in downstream servicing, and integration risks tied to regulatory inventory.

Executive dashboards and a packaged Excel model that link strategic choices (e.g., cutoff dates for R‑410A, retrofit windows) to P&L and balance-sheet outcomes through 2032.

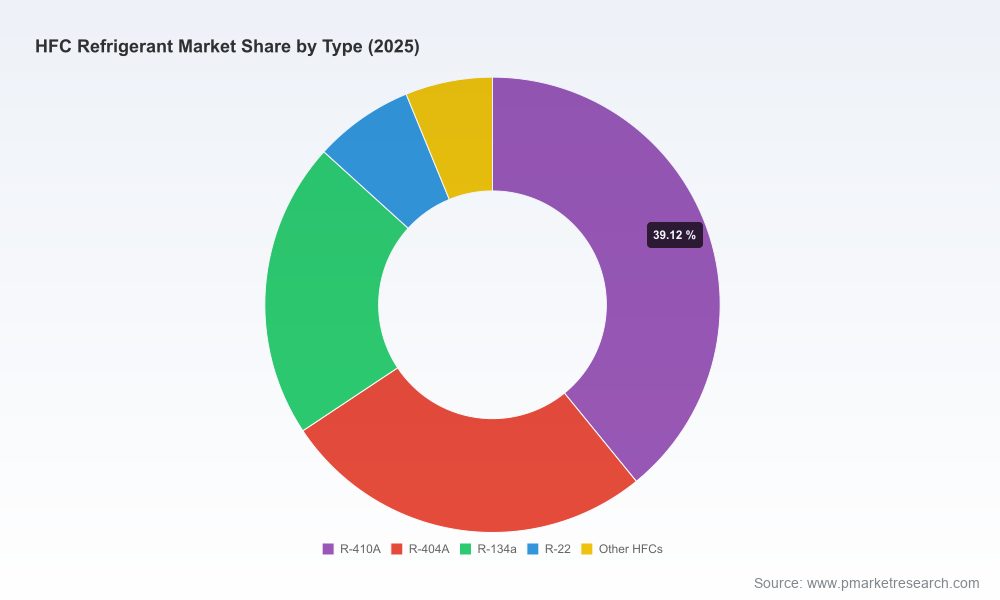

Note: to preserve competitive confidentiality in this briefing we summarize competitive dynamics and regulatory drivers but do not disclose detailed regional or application-level splits. Those segmented datasets, along with downloadable models and supplier-level unit metrics, are included in the full report and its supporting files.

Right-size inventory using scenario-driven thresholds: adopt a dual-queue approach that separates transition-critical inventory from tactical stock to minimize stranded asset risk.

Lock in flexible supply agreements with indexation and capacity options: prioritize contracts that include escalation clauses tied to feedstock indices and optionality for low‑GWP blends.

Fast-track retrofit and low-GWP adoption where lifecycle economics and regulatory timing align: OEMs and large end-users should identify retrofit windows to capture first-mover advantages on servicing and certification.

Engage regulators proactively: contribute operational data and impact assessments to influence phasedown implementation and enforcement timelines, especially for equipment categories with long service lives.

Prepare for strategic M&A or partnership plays: target capabilities that accelerate access to low‑GWP chemistries, distributed fill networks, and compliance-management technologies.

2026 is not a routine planning year for the HFC refrigerant ecosystem; it is a transition year in which regulatory enforcement, supply-chain tightness, and supplier strategy converge to determine who captures value through the next investment cycle. PW Consulting’s HFC Refrigerant Market study provides the data, scenario tools, and operational playbooks to convert uncertainty into defensible choices. This briefing is intentionally selective: it frames the strategic imperatives while preserving the detailed segment-level intelligence for subscribers. For the full dataset, supplier scorecards, scenario workbooks and step‑by‑step implementation guidance, please consult the PW Consulting HFC Refrigerant Market report and model package.

For detailed analysis of this topic, please visit the official page:HFC Refrigerant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com